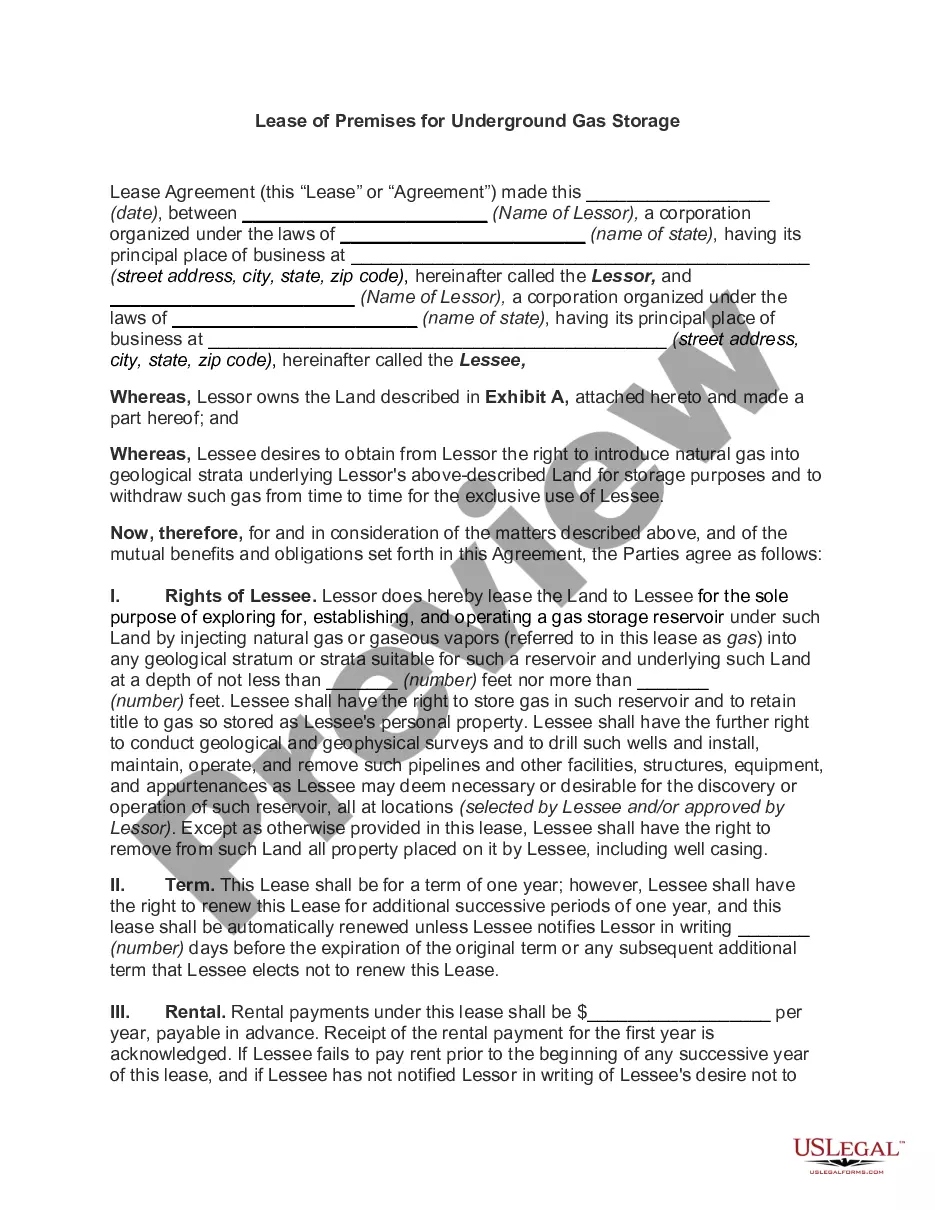

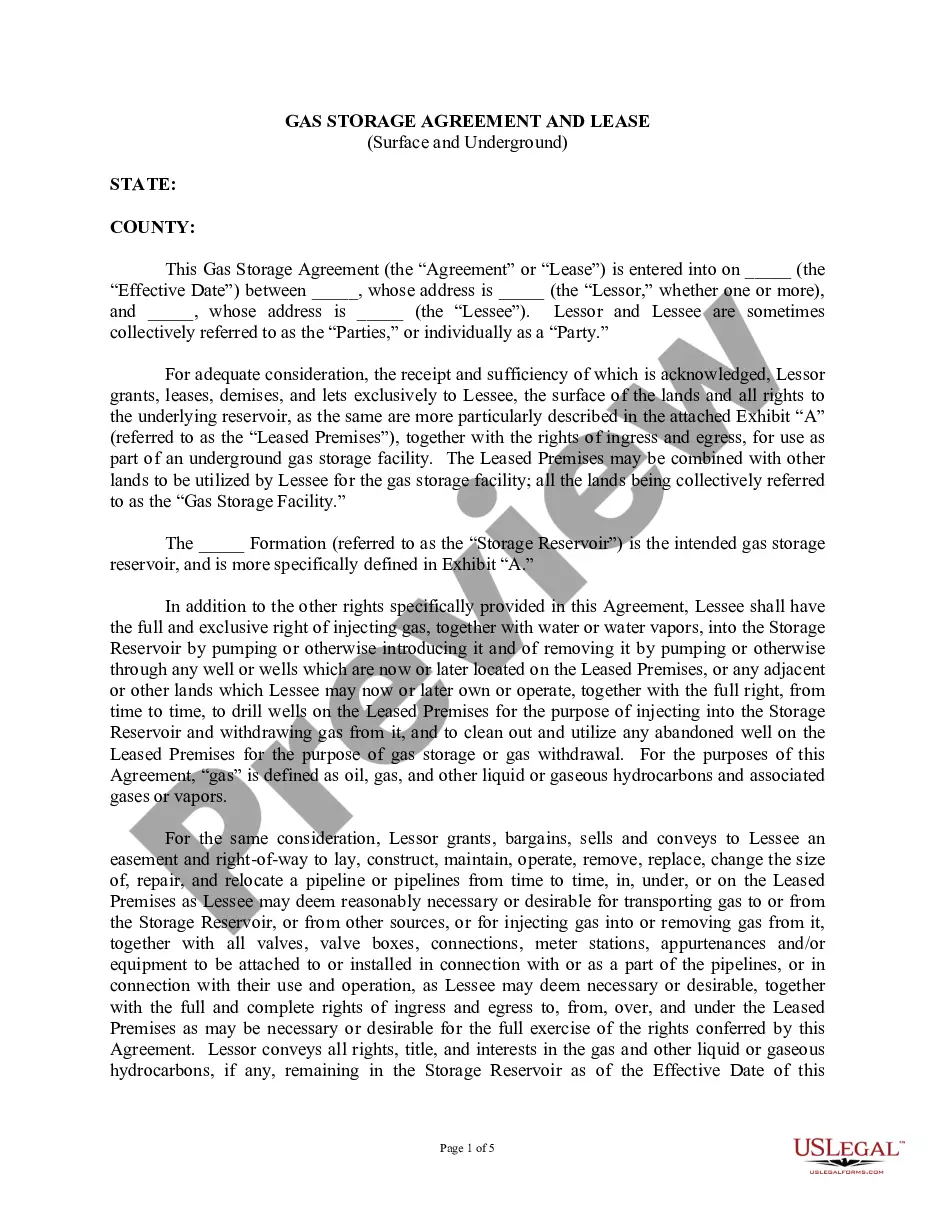

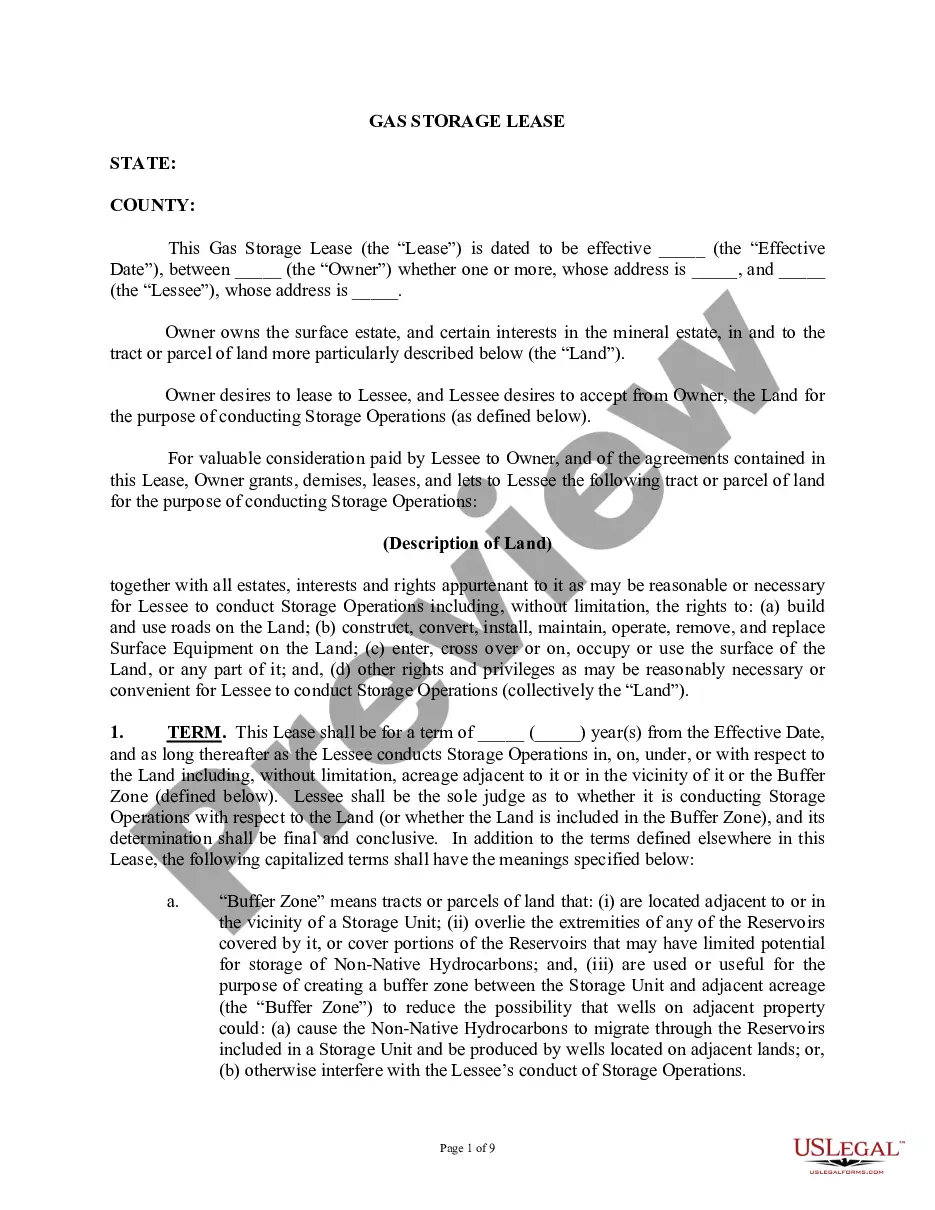

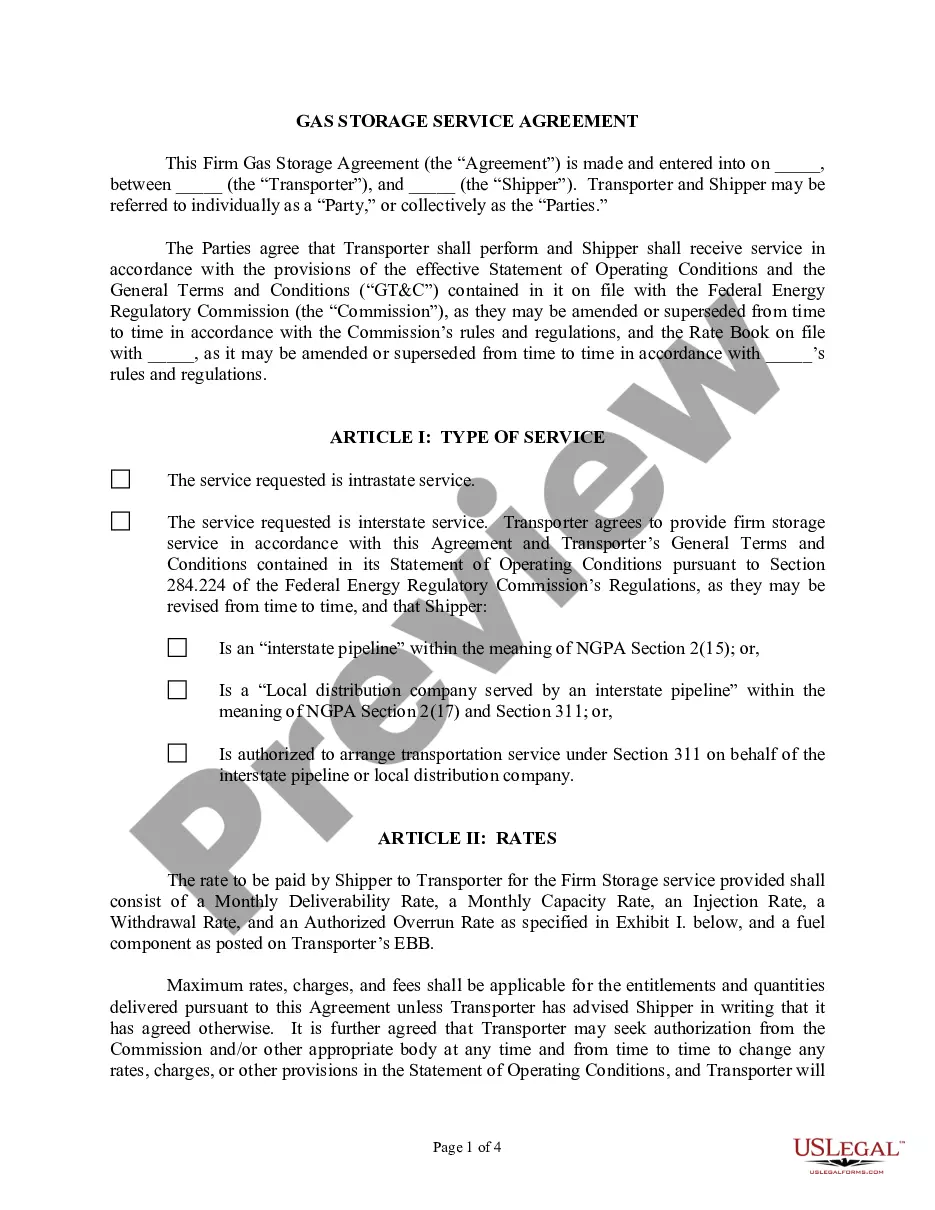

Louisiana Gas Storage Agreement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Gas Storage Agreement?

It is possible to commit time on the Internet trying to find the legitimate document format that suits the federal and state requirements you need. US Legal Forms gives thousands of legitimate types that happen to be reviewed by experts. You can actually download or produce the Louisiana Gas Storage Agreement from your support.

If you already possess a US Legal Forms bank account, you are able to log in and click on the Obtain key. After that, you are able to total, revise, produce, or sign the Louisiana Gas Storage Agreement. Each legitimate document format you acquire is your own property forever. To acquire an additional duplicate for any bought develop, proceed to the My Forms tab and click on the related key.

If you are using the US Legal Forms website initially, keep to the basic guidelines beneath:

- Initially, be sure that you have selected the best document format for the area/city that you pick. See the develop description to make sure you have selected the appropriate develop. If readily available, take advantage of the Review key to look through the document format also.

- If you would like find an additional version from the develop, take advantage of the Search discipline to get the format that fits your needs and requirements.

- After you have located the format you need, simply click Buy now to continue.

- Find the rates strategy you need, type your credentials, and sign up for a free account on US Legal Forms.

- Complete the financial transaction. You should use your bank card or PayPal bank account to purchase the legitimate develop.

- Find the format from the document and download it to the gadget.

- Make alterations to the document if required. It is possible to total, revise and sign and produce Louisiana Gas Storage Agreement.

Obtain and produce thousands of document web templates while using US Legal Forms web site, which offers the biggest assortment of legitimate types. Use professional and status-specific web templates to handle your company or individual demands.

Form popularity

FAQ

Individuals who are domiciled, reside, or have a permanent residence in Louisiana are required to file a Louisiana individual income tax return and report all of their income and pay Louisiana income tax on that income, if applicable.

All nonresident partners who were partners at any time during the taxable year and who do not have a valid agreement on file with LDR must be included in the Louisiana Composite Partnership Return (See LAC 61:I. 1401).

Who Must File? All corporations and entities taxed as corporations for federal income tax purposes deriving income from Louisiana sources, whether or not they have any net income, must file an income tax return.

Louisiana Revised Statute 1.1(F)(4) requires the electronic filing of all composite partnership returns. If tax credits are claimed on the composite return: ALL nonresident partners must be included on the return and on Schedule of Included Partner's Share of Income and Tax.

Composite returns required to be made for an entity treated as a partnership for state income tax purposes and which is made on the basis of the calendar year shall be made and filed with the secretary at Baton Rouge, Louisiana, on or before the fifteenth day of May, following the close of the calendar year.