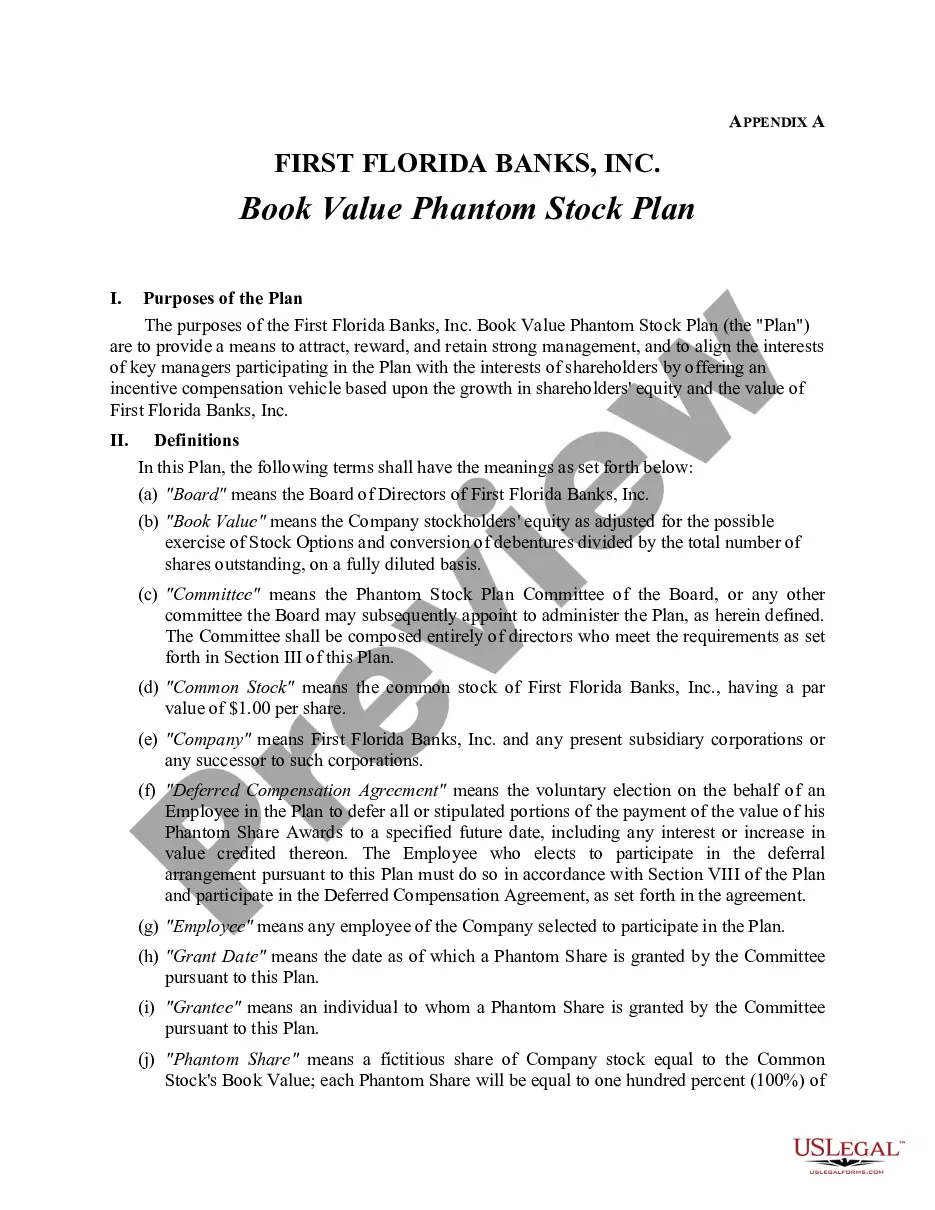

Louisiana Proposed book value phantom stock plan with appendices for First Florida Bank, Inc.

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Proposed Book Value Phantom Stock Plan With Appendices For First Florida Bank, Inc.?

You are able to invest hours on the web trying to find the legal document web template that suits the state and federal specifications you require. US Legal Forms provides thousands of legal forms that are examined by experts. You can easily down load or produce the Louisiana Proposed book value phantom stock plan with appendices for First Florida Bank, Inc. from my support.

If you have a US Legal Forms bank account, you are able to log in and then click the Acquire option. Following that, you are able to complete, change, produce, or indication the Louisiana Proposed book value phantom stock plan with appendices for First Florida Bank, Inc.. Every legal document web template you purchase is the one you have for a long time. To acquire another backup of the acquired form, check out the My Forms tab and then click the corresponding option.

Should you use the US Legal Forms internet site the very first time, adhere to the basic directions below:

- Initially, make sure that you have chosen the proper document web template for your county/area that you pick. Read the form explanation to ensure you have picked the correct form. If available, use the Review option to search throughout the document web template as well.

- If you wish to locate another version from the form, use the Research discipline to get the web template that meets your requirements and specifications.

- Upon having identified the web template you need, simply click Buy now to proceed.

- Select the costs program you need, type in your references, and sign up for a free account on US Legal Forms.

- Total the transaction. You may use your bank card or PayPal bank account to purchase the legal form.

- Select the format from the document and down load it to the gadget.

- Make changes to the document if necessary. You are able to complete, change and indication and produce Louisiana Proposed book value phantom stock plan with appendices for First Florida Bank, Inc..

Acquire and produce thousands of document themes utilizing the US Legal Forms site, which provides the greatest assortment of legal forms. Use skilled and state-distinct themes to take on your organization or personal demands.

Form popularity

FAQ

Phantom shares usually get liquid when the company gets acquired or goes public or if the company decides to do a buyback. Any gains from the assets must be reported to tax authorities as ordinary income upon vesting.

Providing phantom stock allows the company to reward employees for their hard work without worrying about those big problems. Phantom shares are typically used to encourage senior leadership to produce better results for the company.

Phantom stock plans are considered ?liability awards? for accounting purposes (assuming they will be settled in cash rather than stock). As such, the sponsoring company must recognize the plan expense ratably over the vesting period. Varying accrual schedules can be found in the market.

On redemption, in a phantom stock plan, the plan participant receives a cash payment. This is in comparison to a stock option plan, where the plan participant receives common stock. As a result, a phantom stock plan allows the participant to reap the benefits of an increasing share price without shareholder dilution.

The answer involves two variables: (a) the presumed value of the company, and (b) the number of shares to be used in the plan. Once these two answers are known, the phantom share price is calculated as the former (the value) divided by the latter (the number of shares).

For example, suppose an employee received 10 phantom shares with a starting value of $7, and assume the shares are valued on the payment date at $15. At the date of payment the employee would receive $150 under a ?full value? plan and $80 under an ?appreciation only? plan.

However, phantom stocks come with a considerable amount of disadvantages that can diminish participants' perceived control and influence, strain company liquidity, require extensive administrative efforts, introduce tax complexities, create disagreements, and subject participants to volatility in financial benefits ...

As a default, this form plan provides for forfeiture of all unvested phantom stock units upon a participant's termination of employment (subject to the terms of the award agreement).