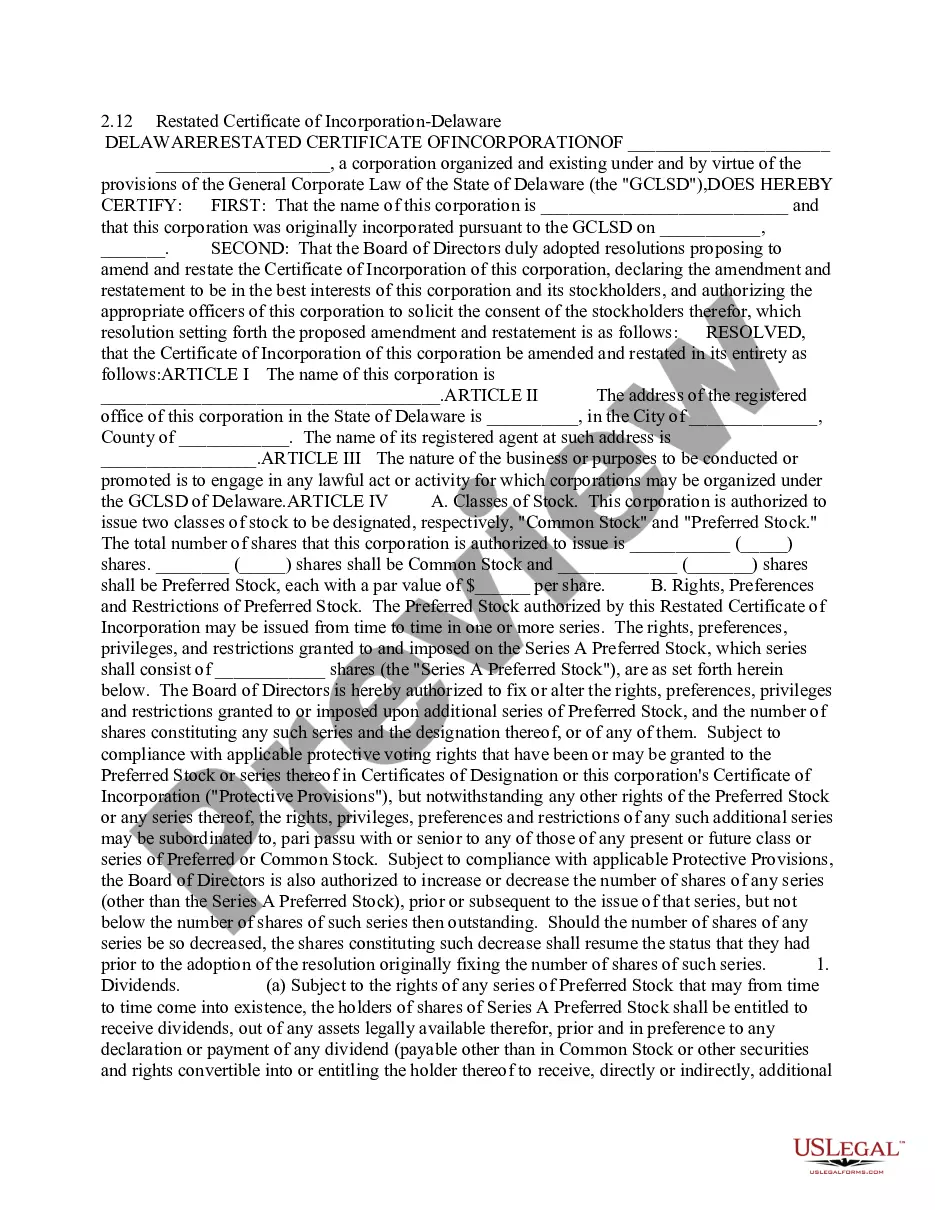

Kentucky Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock

Description

How to fill out Amendment Of Restated Certificate Of Incorporation To Change Dividend Rate On $10.50 Cumulative Second Preferred Convertible Stock?

You are able to spend hours online attempting to find the authorized record design that suits the federal and state requirements you need. US Legal Forms offers 1000s of authorized types that are analyzed by specialists. You can easily acquire or produce the Kentucky Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock from the services.

If you have a US Legal Forms bank account, you may log in and click the Down load key. Next, you may full, revise, produce, or sign the Kentucky Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock. Each authorized record design you acquire is your own property forever. To obtain one more copy of the obtained form, proceed to the My Forms tab and click the related key.

If you work with the US Legal Forms internet site the first time, keep to the simple instructions under:

- Initial, make sure that you have chosen the proper record design to the state/city of your liking. Look at the form outline to ensure you have selected the right form. If readily available, take advantage of the Preview key to look through the record design too.

- In order to locate one more model in the form, take advantage of the Search area to find the design that fits your needs and requirements.

- Once you have located the design you need, just click Buy now to move forward.

- Choose the pricing plan you need, enter your accreditations, and register for a free account on US Legal Forms.

- Total the financial transaction. You should use your Visa or Mastercard or PayPal bank account to purchase the authorized form.

- Choose the structure in the record and acquire it for your product.

- Make modifications for your record if possible. You are able to full, revise and sign and produce Kentucky Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock.

Down load and produce 1000s of record themes using the US Legal Forms Internet site, which provides the largest assortment of authorized types. Use skilled and express-specific themes to handle your organization or individual requirements.

Form popularity

FAQ

There may be a number of these over time and, in more complex and long-running transactions, it is common at some point for the original facility agreement with its changes to be ?amended and restated? ? in other words, consolidated and contained in a single document. That is as much for ease of reading as anything.

?Amended? means that the document has ?changed?? that someone has revised the document. ?Restated? means ?presented in its entirety?, ? as a single, complete document. ingly, ?amended and restated? means a complete document into which one or more changes have been incorporated.

This Agreement is intended to and does completely amend and restate, without novation, the Original Agreement. All credit extensions or loans outstanding under the Original Agreement are and shall continue to be outstanding under this Agreement.

Hear this out loud PauseAn Amended and Restated Certificate of Incorporation is a legal document filed with the Secretary of State that restates, integrates, and adjusts the startup's initial Articles of Incorporation (i.e. the company's Charter).