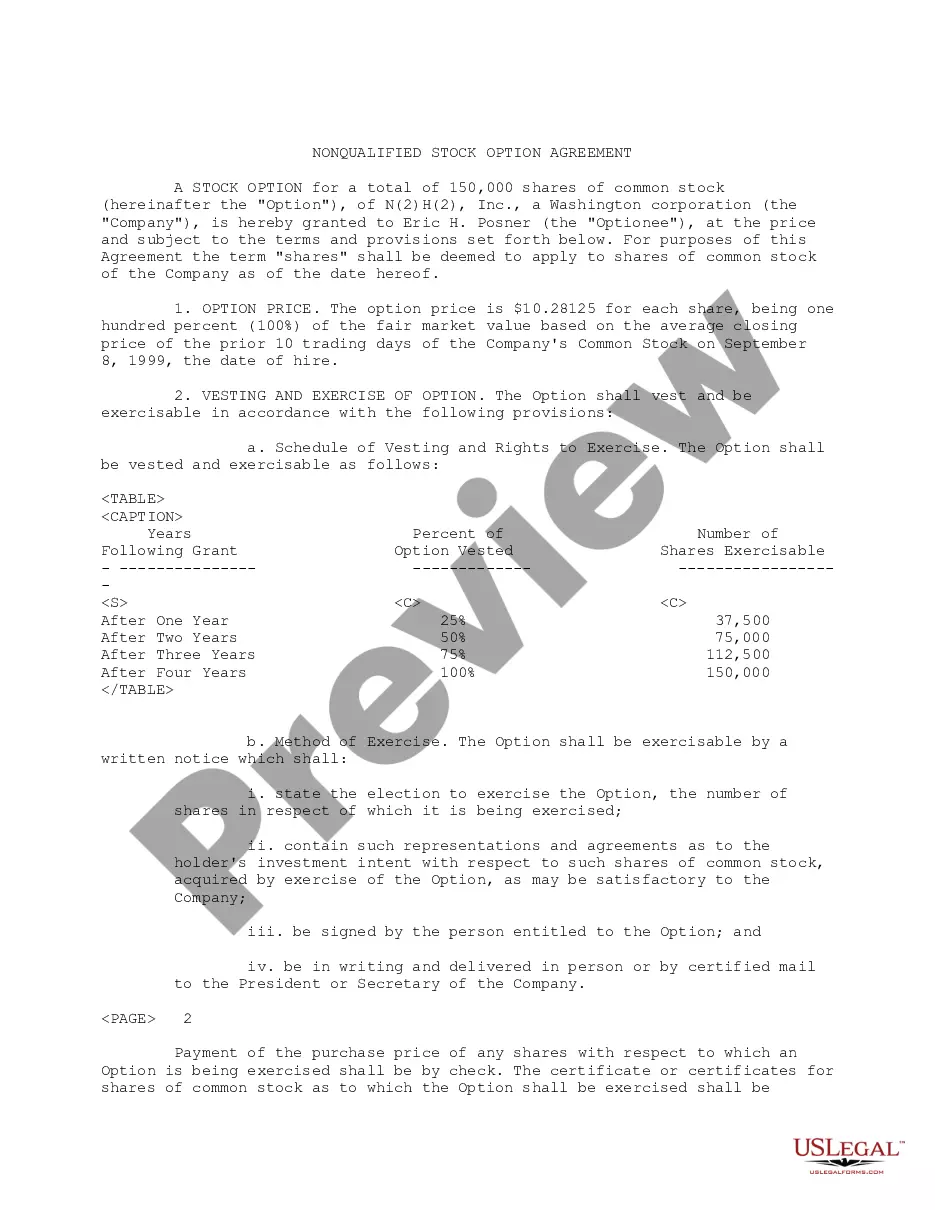

Kentucky Proposal Approval of Nonqualified Stock Option Plan

Description

How to fill out Proposal Approval Of Nonqualified Stock Option Plan?

If you have to total, download, or printing legitimate document themes, use US Legal Forms, the biggest assortment of legitimate varieties, that can be found on the web. Utilize the site`s simple and practical search to obtain the documents you want. Numerous themes for company and individual reasons are sorted by classes and suggests, or keywords. Use US Legal Forms to obtain the Kentucky Proposal Approval of Nonqualified Stock Option Plan in just a handful of mouse clicks.

When you are currently a US Legal Forms customer, log in to the profile and click the Obtain option to have the Kentucky Proposal Approval of Nonqualified Stock Option Plan. You can also entry varieties you in the past saved in the My Forms tab of your own profile.

If you use US Legal Forms the first time, follow the instructions beneath:

- Step 1. Ensure you have selected the shape for your correct metropolis/region.

- Step 2. Utilize the Preview solution to check out the form`s articles. Never neglect to learn the description.

- Step 3. When you are unsatisfied using the develop, utilize the Research industry at the top of the monitor to discover other types from the legitimate develop design.

- Step 4. After you have discovered the shape you want, click the Acquire now option. Pick the rates program you like and add your credentials to register for an profile.

- Step 5. Process the purchase. You may use your bank card or PayPal profile to finish the purchase.

- Step 6. Choose the formatting from the legitimate develop and download it on the system.

- Step 7. Comprehensive, revise and printing or sign the Kentucky Proposal Approval of Nonqualified Stock Option Plan.

Every single legitimate document design you buy is the one you have eternally. You have acces to every develop you saved inside your acccount. Click on the My Forms area and pick a develop to printing or download again.

Remain competitive and download, and printing the Kentucky Proposal Approval of Nonqualified Stock Option Plan with US Legal Forms. There are thousands of specialist and status-specific varieties you can use for your personal company or individual requires.

Form popularity

FAQ

Employee stock options are offered by companies to their employees as equity compensation plans. These grants come in the form of regular call options and give an employee the right to buy the company's stock at a specified price for a finite period of time.

NQOs, short for non-qualified stock options, are the most common type of employee stock option. They allow you to purchase stock for a fixed price for a defined period of time, as the market value of the stock continues to rise, allowing employees to profit off the difference. NQOs are just as they sound?unqualified.

Equity compensation is non-cash pay that is offered to employees. Equity compensation may include options, restricted stock, and performance shares; all of these investment vehicles represent ownership in the firm for a company's employees.

Once you have a plan in place, you can simply make amendments to increase the number of shares in the option pool on an as-needed basis. The initial plan and any expansions must be approved by your board of directors and then by shareholders.

The US federal tax laws do not generally address the level of approval required for equity awards, but the tax rules that govern the qualification of so-called incentive stock options require that the options be granted under a shareholder-approved plan.

If eligibility and holding period requirements are met, the bargain element is taxed as a capital gain to the employee. For non-qualified stock options, the bargain element is treated as ordinary income to the employee.

Stock Based Compensation (also called Share-Based Compensation or Equity Compensation) is a way of paying employees, executives, and directors of a company with equity in the business.

Board Approval The Company's board of directors must approve all stock option grants, including the name of the recipient, the number of shares, the vesting schedule and the exercise price. This can be done either in a board meeting or via unanimous written consent.