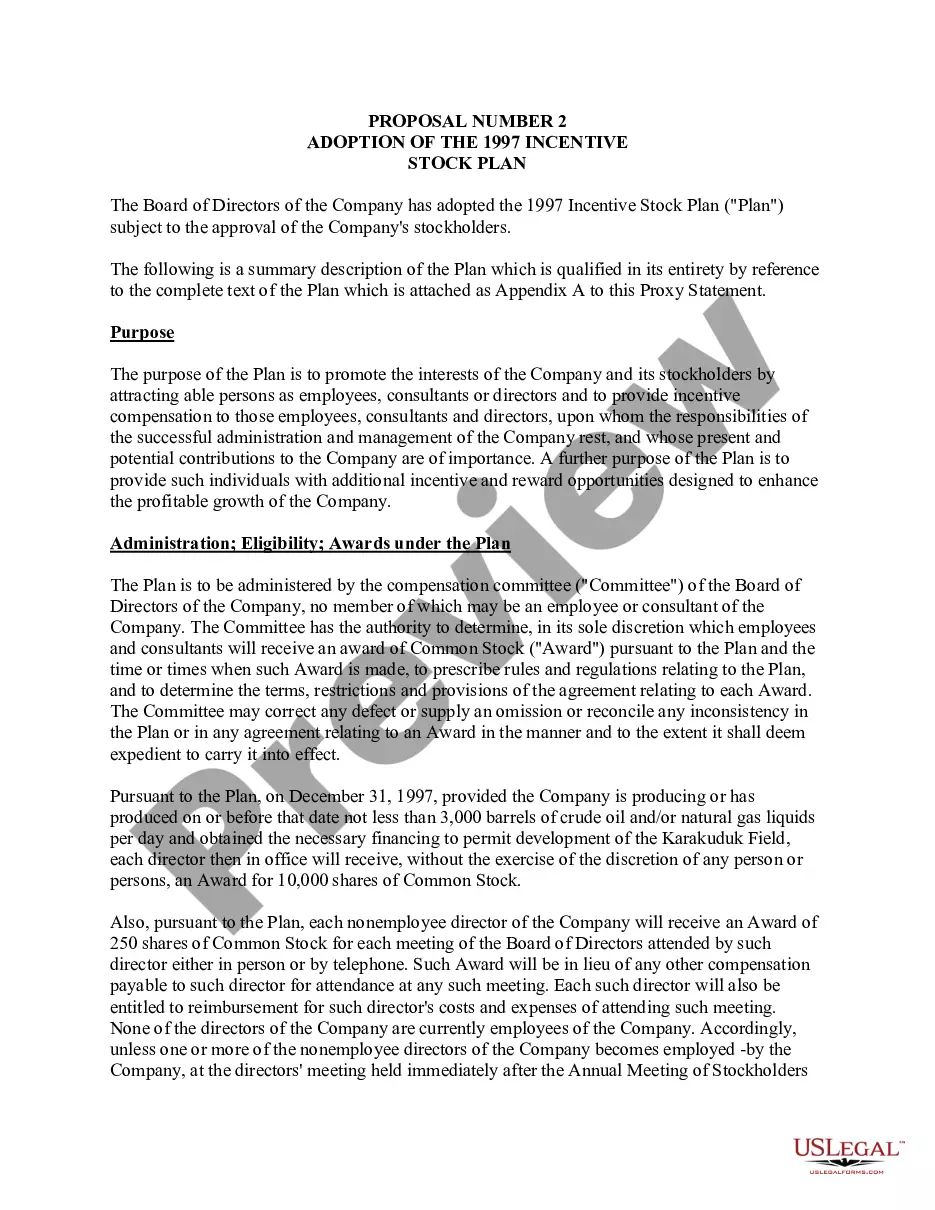

Kentucky Approval of Incentive Stock Option Plan

Description

How to fill out Approval Of Incentive Stock Option Plan?

US Legal Forms - one of several largest libraries of legal varieties in the United States - offers a wide array of legal papers themes you can obtain or produce. Using the internet site, you may get thousands of varieties for company and personal reasons, sorted by categories, claims, or key phrases.You can get the newest models of varieties like the Kentucky Approval of Incentive Stock Option Plan within minutes.

If you already have a subscription, log in and obtain Kentucky Approval of Incentive Stock Option Plan from your US Legal Forms local library. The Acquire option will show up on every single kind you view. You have accessibility to all previously saved varieties inside the My Forms tab of your own profile.

If you would like use US Legal Forms the very first time, allow me to share basic recommendations to obtain started off:

- Be sure to have picked the proper kind to your city/area. Go through the Review option to analyze the form`s articles. Read the kind information to ensure that you have selected the proper kind.

- In the event the kind doesn`t fit your requirements, take advantage of the Lookup discipline towards the top of the display screen to discover the one who does.

- In case you are satisfied with the form, confirm your selection by visiting the Purchase now option. Then, pick the costs program you prefer and provide your accreditations to register for the profile.

- Method the financial transaction. Make use of your Visa or Mastercard or PayPal profile to accomplish the financial transaction.

- Find the structure and obtain the form on the gadget.

- Make alterations. Load, edit and produce and indication the saved Kentucky Approval of Incentive Stock Option Plan.

Each design you included with your bank account lacks an expiry time which is yours permanently. So, if you would like obtain or produce yet another version, just check out the My Forms portion and then click around the kind you require.

Gain access to the Kentucky Approval of Incentive Stock Option Plan with US Legal Forms, by far the most comprehensive local library of legal papers themes. Use thousands of skilled and status-particular themes that fulfill your organization or personal requirements and requirements.

Form popularity

FAQ

Failure to get board approval Let's start with an obvious one that founders routinely miss in the early days: Stock option grants must be approved by the board. If the board doesn't approve (either at a board meeting or by unanimous written consent), the stock options haven't actually been granted.

There are many requirements on using ISOs. First, the employee must not sell the stock until after two years from the date of receiving the options, and they must hold the stock for at least a year after exercising the option like other capital gains. Secondly, the stock option must last ten years.

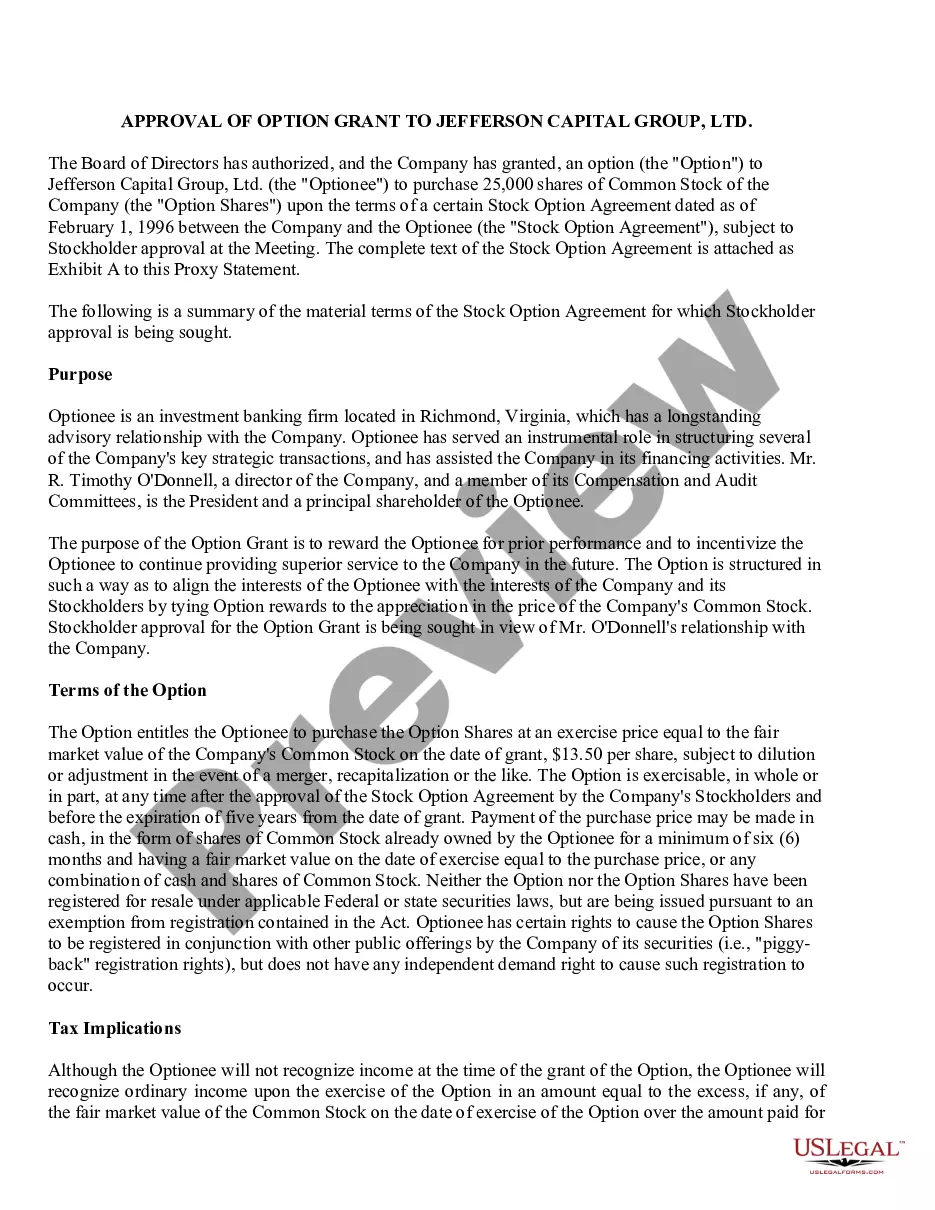

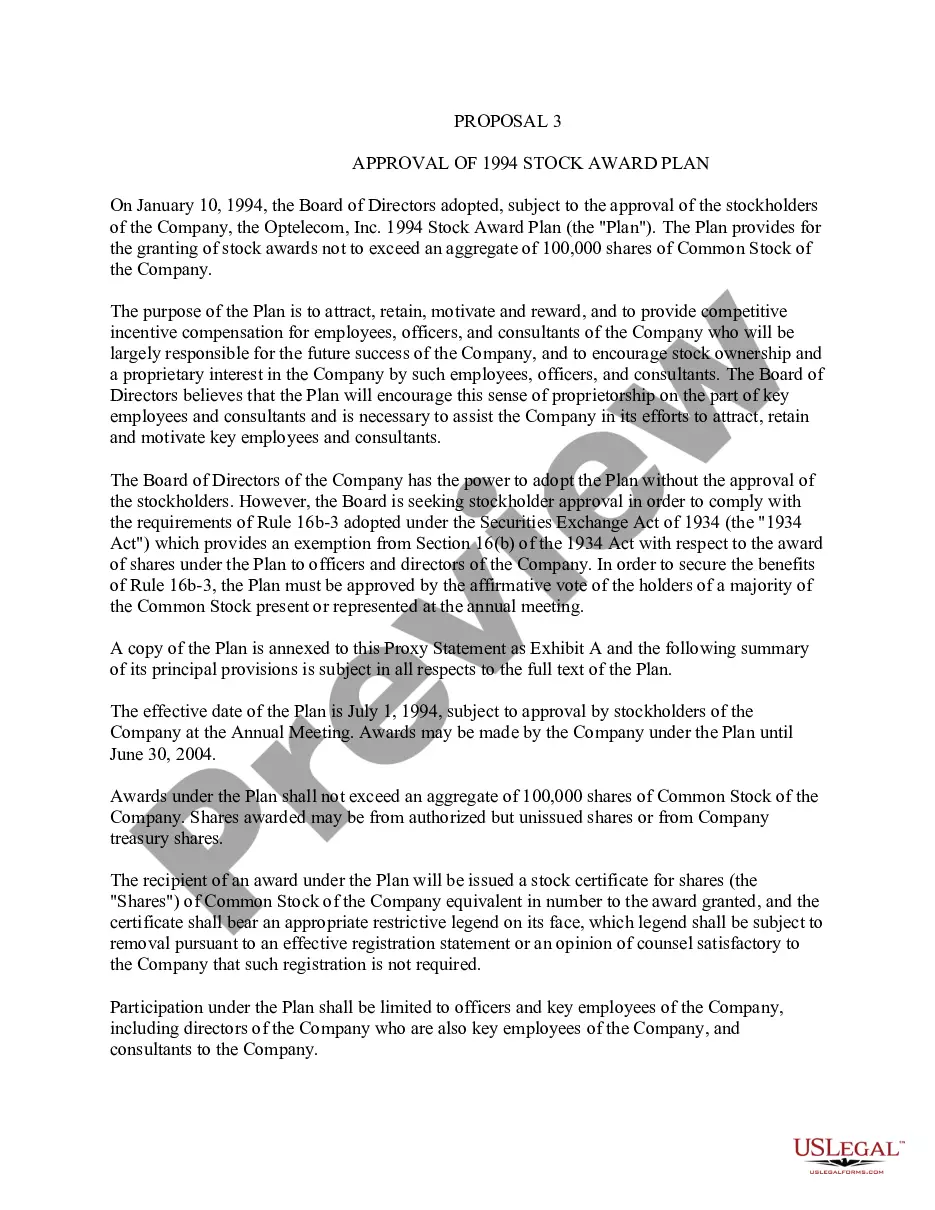

The US federal tax laws do not generally address the level of approval required for equity awards, but the tax rules that govern the qualification of so-called incentive stock options require that the options be granted under a shareholder-approved plan.

An incentive stock option (ISO) is a corporate benefit that gives an employee the right to buy shares of company stock at a discounted price with the added benefit of possible tax breaks on the profit. The profit on qualified ISOs is usually taxed at the capital gains rate, not the higher rate for ordinary income.

Corporate actions include stock splits, dividends, mergers and acquisitions, rights issues and spin-offs. All of these are major decisions that typically need to be approved by the company's board of directors and authorized by its shareholders.

To receive the incentive, you must hold (keep) ISOs for at least one year after exercise and two years after the grant date. If you hold your stock for at least a year after purchase, you will pay the lower capital gains tax rate on the increase in value.

Once you have a plan in place, you can simply make amendments to increase the number of shares in the option pool on an as-needed basis. The initial plan and any expansions must be approved by your board of directors and then by shareholders.

A stock option plan must be adopted by the company's directors and, in some cases, approved by the company's shareholders.