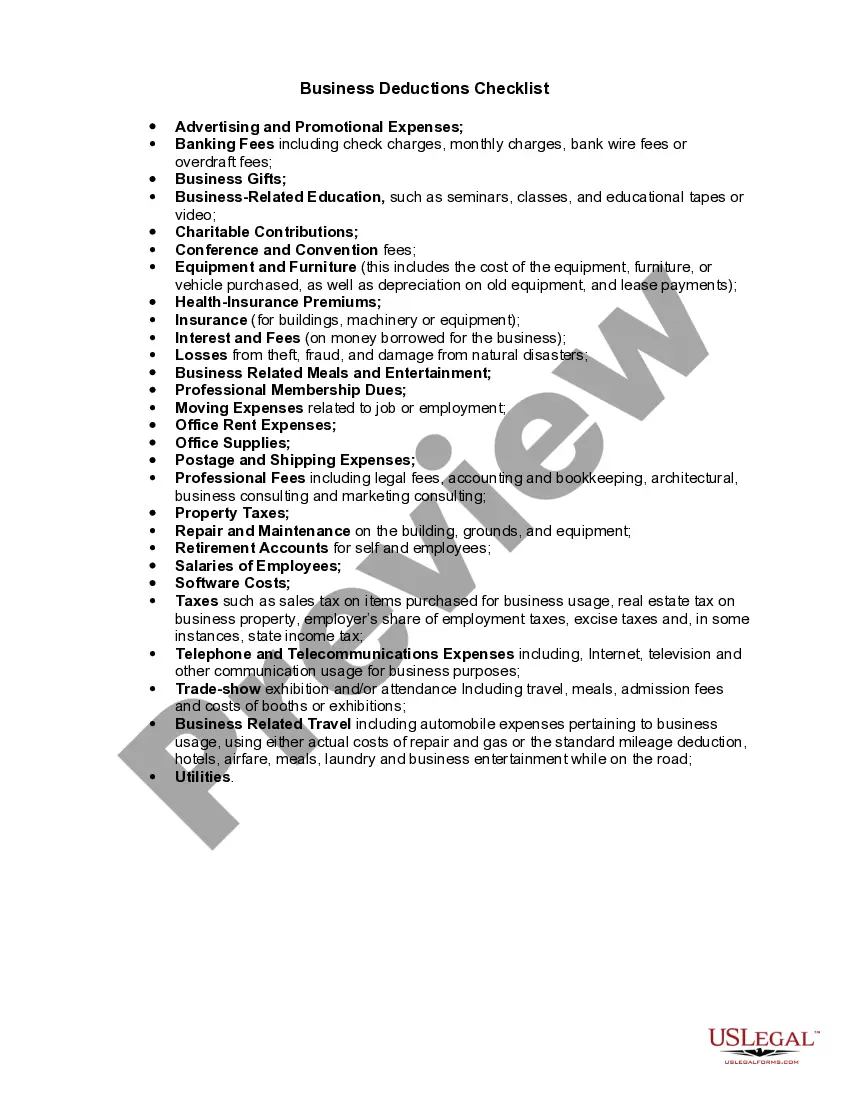

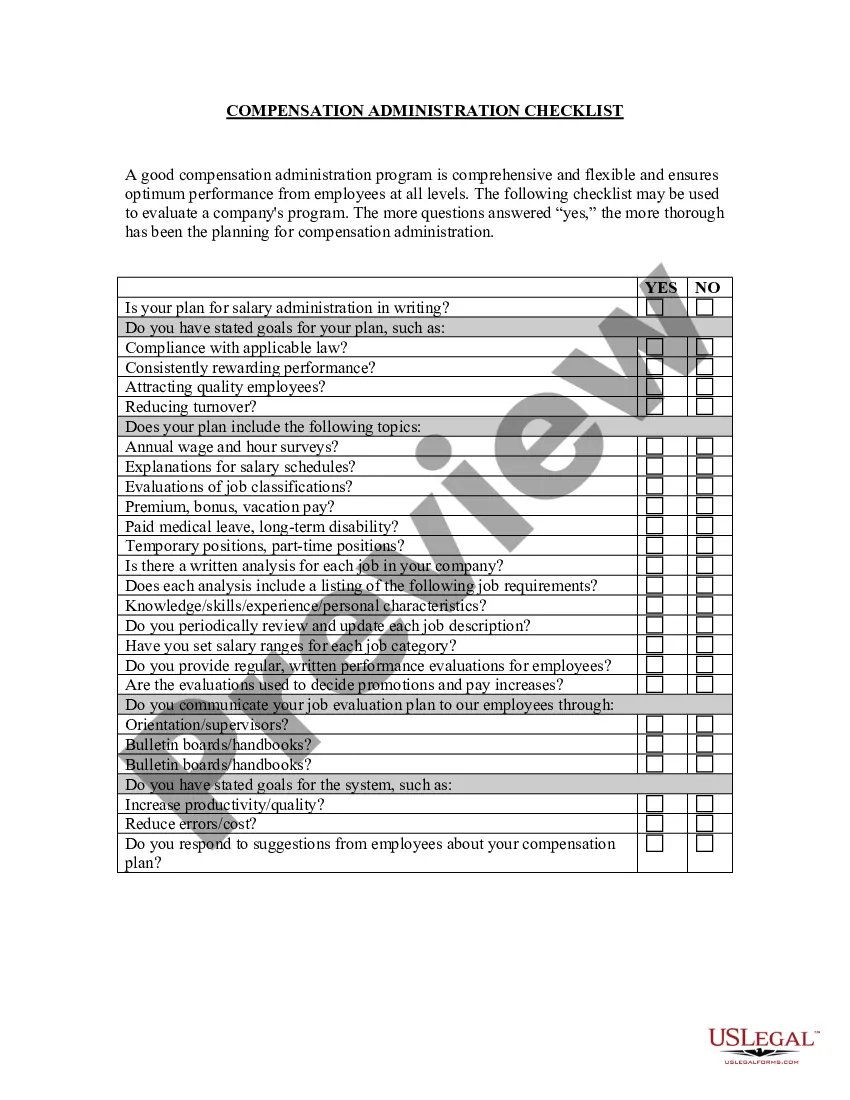

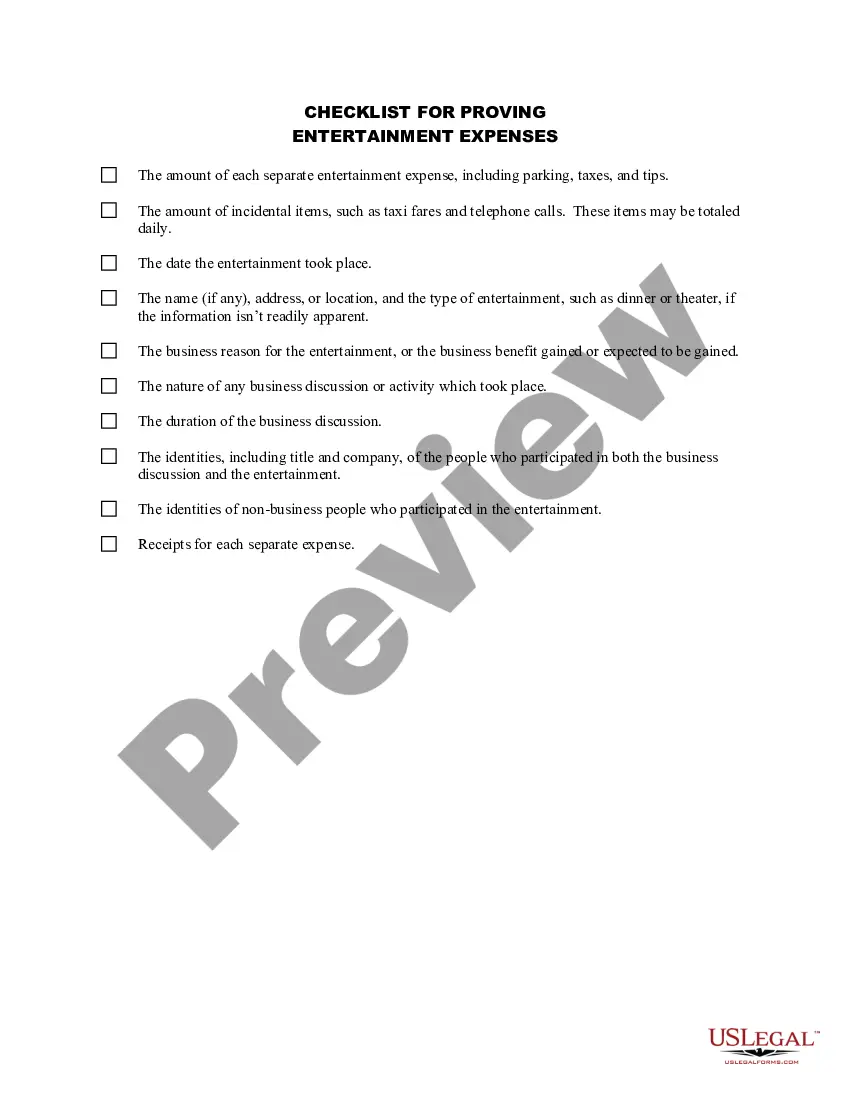

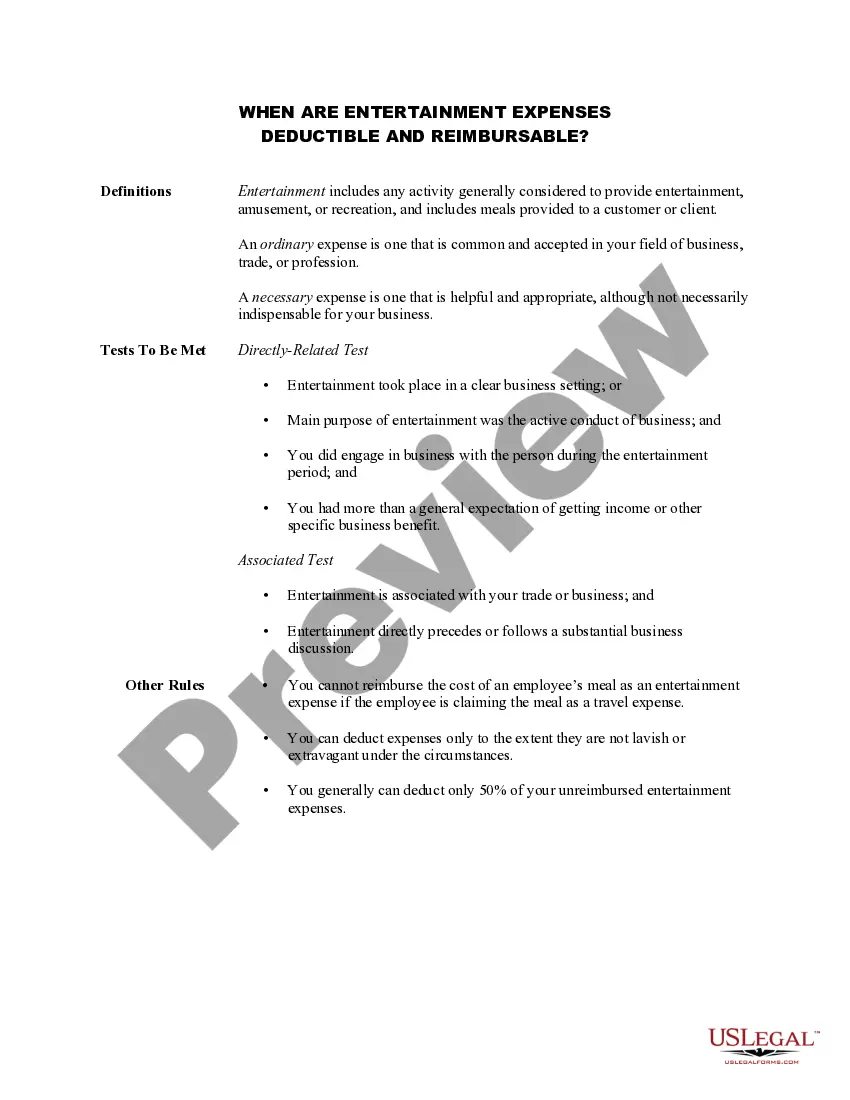

Kentucky Business Deductibility Checklist

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Business Deductibility Checklist?

US Legal Forms - one of the largest repositories of legal documents in the United States - offers a diverse collection of legal form templates that you can download or print.

By using the platform, you have access to thousands of forms for personal and business purposes, sorted by categories, states, or keywords. You can find the latest versions of forms like the Kentucky Business Deductibility Checklist in just a few moments.

If you have a monthly subscription, Log In to obtain the Kentucky Business Deductibility Checklist from the US Legal Forms library. The Acquire option will be visible on every form you view. You can access all previously downloaded forms from the My documents section of your account.

Complete the payment process. Use your credit card or PayPal account to finalize the transaction.

Choose the format and download the form to your device. Edit. Fill out, modify, print, and sign the downloaded Kentucky Business Deductibility Checklist. Each template saved in your account does not expire and belongs to you indefinitely. Therefore, if you wish to download or print another copy, simply navigate to the My documents section and click on the form you desire. Access the Kentucky Business Deductibility Checklist with US Legal Forms, the most extensive collection of legal document templates. Utilize thousands of professional and state-specific templates that cater to your business or personal requirements.

- Make sure to select the appropriate form for your region/state.

- Use the Preview option to check the contents of the form.

- Read the form details to confirm that you have chosen the correct document.

- If the form does not meet your needs, use the Search box at the top of the page to find the right one.

- If you are satisfied with the form, confirm your choice by clicking on the Acquire now button.

- Then, select your preferred payment plan and provide your details to register for an account.

Form popularity

FAQ

Kentucky's limited liability entity tax applies to traditional corporations, S corporations, LLCs, limited partnerships (LPs), and limited liability partnerships (LLPs). The tax is based on a business's annual gross receipts. For businesses with gross receipts less than $3 million, there is a minimum LLET of $175.

200bThe tax imposed by KRS 141.0401 is a tax imposed on those entities with limited liability in the state of Kentucky and not an income tax. Therefore, the Limited Liability Entity Tax (LLET) paid is not an add-back to determine Kentucky taxable income; it is deductible for Kentucky and federal purposes.

A Nonresident withholding and Composite Income Tax Return is filed on form 740NP-WH (with copy A of PTE-WH completed for each partner, member, or shareholder) by the 15th day of the fourth month following the close of the tax year. The withholding rate is at the maximum rate provided in KRS 141.020 or KRS 141.040.

The state calculates its franchise tax based on a company's margin which is computed in one of four ways: Total revenue multiplied by 70% Total revenue minus cost of goods sold (COGS) Total revenue minus compensation paid to all personnel.

Those who chose this option will now see the amount of federal and state taxes withheld in boxes 4 and 11 of Form 1099-G. Box 1 of Form 1099-G, labeled "unemployment compensation," contains the total amount of benefits before any taxes were taken out. Box 1's total includes the sum of pretax weekly benefit amounts.

Kentucky's limited liability entity tax applies to traditional corporations, S corporations, LLCs, limited partnerships (LPs), and limited liability partnerships (LLPs). The tax is based on a business's annual gross receipts. For businesses with gross receipts less than $3 million, there is a minimum LLET of $175.

To pay a bill, an estimated payment, an extension payment, or a payment for paper filed or electronically filed Corporation Income Tax and/or Limited Entity Tax (LLET) return: Electronic payment: Choose to pay directly from your bank account or by credit card. Service provider fees may apply.

The LLET may be calculated using the lesser of $0.095/$100 of Kentucky gross receipts or $0.75/$100 of Kentucky gross profits. A minimum tax of $175 applies regardless of the method used. Sole proprietorships and pass-through entities are exempt from state corporate income taxes.

Yes, Kentucky allows taxpayers either to: itemize deductions; or. claim a standard deduction.

What Is A Pass Through Entity? A pass-through entity (also known as flow-through entity) is a business structure in which business income is treated as personal income of the owners. It is used to avoid double taxation, when business income is subject to corporate tax and then to the owner's personal income.