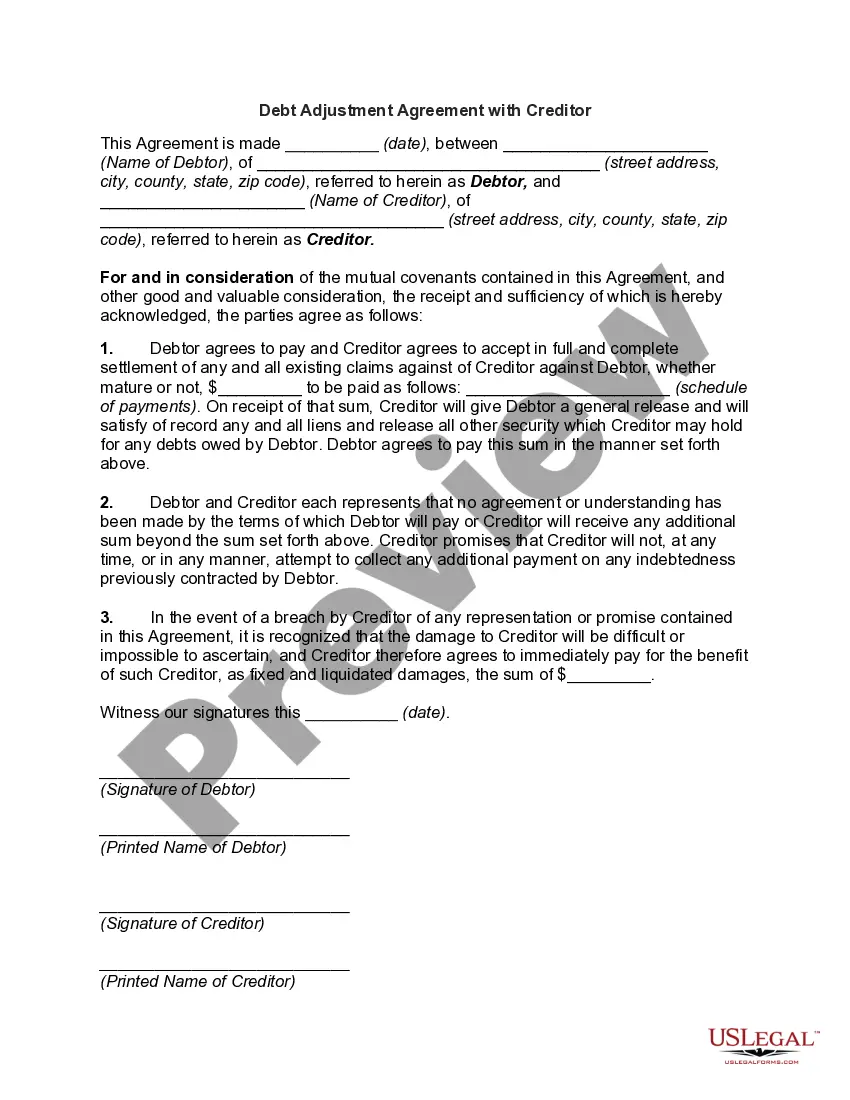

Kentucky Agreement that Statement of Account is True, Correct and Settled

Instant download

Description

A mineral lease is an agreement between a property owner and another party who is allowed to explore and extract minerals that are found on the property for a stated time. The property owner receives payments based on the value of the minerals that are extracted. In other words, a mineral lease is a right given to use land for the purpose of exploration for a particular period of time or indefinitely upon payment of royalties to the landowner.

How to fill out Agreement That Statement Of Account Is True, Correct And Settled?

Finding the correct legal document template can be a challenge.

Of course, there are numerous templates accessible online, but how can you find the legal form you require.

Utilize the US Legal Forms website. This service offers thousands of templates, including the Kentucky Agreement affirming that the Statement of Account is True, Correct, and Settled, suitable for both business and personal use.

First, ensure you have selected the correct form for your locality/state. You can preview the form using the Review button and examine the form description to confirm it is the appropriate one for you.

- All forms are verified by professionals and comply with state and federal requirements.

- If you are already registered, Log In to your account and click the Download button to retrieve the Kentucky Agreement affirming that the Statement of Account is True, Correct, and Settled.

- Utilize your account to review the legal forms you have previously acquired.

- Navigate to the My documents section of your account to download another copy of the documents you need.

- If you are a new user of US Legal Forms, here are straightforward steps for you to follow.