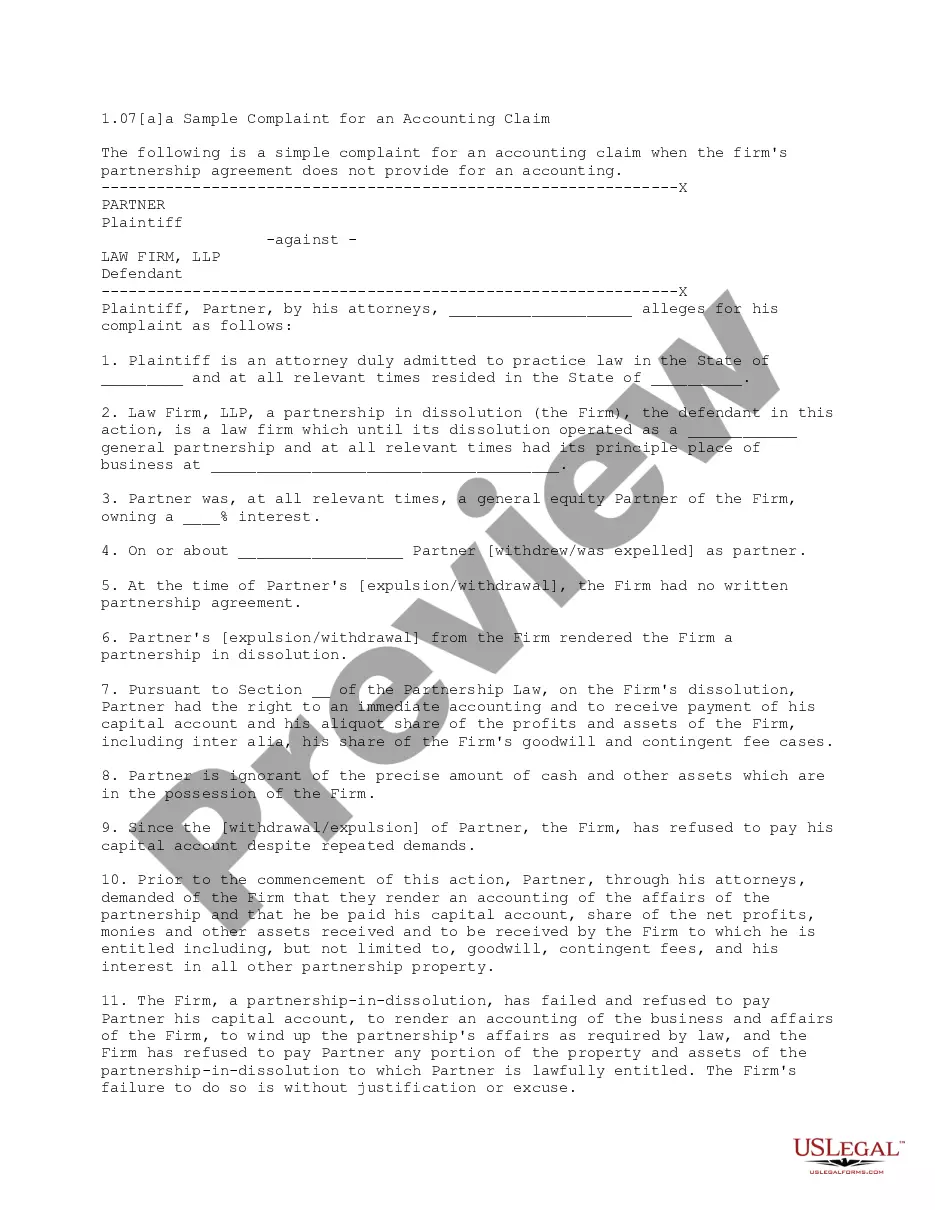

This complaint is for a plaintiff attorney who has been removed from the partnership of his former firm. The complaint requests an accounting of the former firm, stating that the plaintiff has been deprived of economic benefits rightfully due to him under the former partnership agreement, and also alleges egregious acts by his former partners.

Kansas Alternative Complaint for an Accounting which includes Egregious Acts

Category:

State:

Multi-State

Control #:

US-L0107A

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Alternative Complaint For An Accounting Which Includes Egregious Acts?

If you want to total, obtain, or printing lawful papers templates, use US Legal Forms, the most important selection of lawful types, which can be found on-line. Take advantage of the site`s simple and easy convenient look for to get the documents you will need. Various templates for company and specific functions are sorted by classes and states, or search phrases. Use US Legal Forms to get the Kansas Alternative Complaint for an Accounting which includes Egregious Acts in just a couple of clicks.

Should you be previously a US Legal Forms consumer, log in to the bank account and click on the Acquire switch to get the Kansas Alternative Complaint for an Accounting which includes Egregious Acts. Also you can entry types you previously downloaded inside the My Forms tab of your bank account.

If you work with US Legal Forms the first time, refer to the instructions listed below:

- Step 1. Be sure you have chosen the shape for that right metropolis/nation.

- Step 2. Make use of the Review option to look over the form`s articles. Do not overlook to learn the explanation.

- Step 3. Should you be not happy together with the develop, make use of the Research field near the top of the monitor to find other models in the lawful develop design.

- Step 4. Once you have located the shape you will need, select the Purchase now switch. Choose the pricing strategy you prefer and include your credentials to register on an bank account.

- Step 5. Process the transaction. You can utilize your credit card or PayPal bank account to accomplish the transaction.

- Step 6. Select the file format in the lawful develop and obtain it on your own product.

- Step 7. Complete, change and printing or indicator the Kansas Alternative Complaint for an Accounting which includes Egregious Acts.

Each lawful papers design you buy is your own eternally. You may have acces to every develop you downloaded within your acccount. Click the My Forms portion and decide on a develop to printing or obtain again.

Remain competitive and obtain, and printing the Kansas Alternative Complaint for an Accounting which includes Egregious Acts with US Legal Forms. There are thousands of expert and express-distinct types you may use for your personal company or specific requires.

Form popularity

FAQ

Contact our office at 913-715-3003 or file a formal complaint with us. You can also contact the Kansas Attorney General's Consumer Protection Office at 1-800-432-2310 or 913-296-3751.

The Attorney General's Office provides legal services to state agencies and boards, promotes open and accountable government, issues Attorney General's Opinions, protects consumers from fraud, assists the victims of crime and defends the state in civil proceedings.

Kansas. Kansas does not have a state license for contractors, so you can file a complaint against a contractor in Kansa, through the Kansas Attorney General. Online: To file a complaint online, visit the complaint form.

Contact Us Kansas Attorney General Kris W. Kobach. ... Consumer Protection. Consumer Protection Hotline: ... Concealed Carry. (785) 291-3765. ... Private Detective Licensing. (785) 296-4240. ... Victims' Services. (785) 291-3950. ... Crime Victims Compensation. (785) 296-2359. ... Medicaid Fraud & Abuse. (785) 368-6220. ... Media. (785) 296-2215.

It's one way to avoid pesky calls from telemarketers. Consumer Protection Hotline: 1-800-432-2310. (785) 296-3751. Fax: (785) 291-3699. File a complaint online. Attorney General Consumer Protection Division. 120 SW 10th Ave., 2nd Floor. Topeka, KS 66612. (785) 296-2215. 1-888-428-8436. Fax: (785) 296-6296.