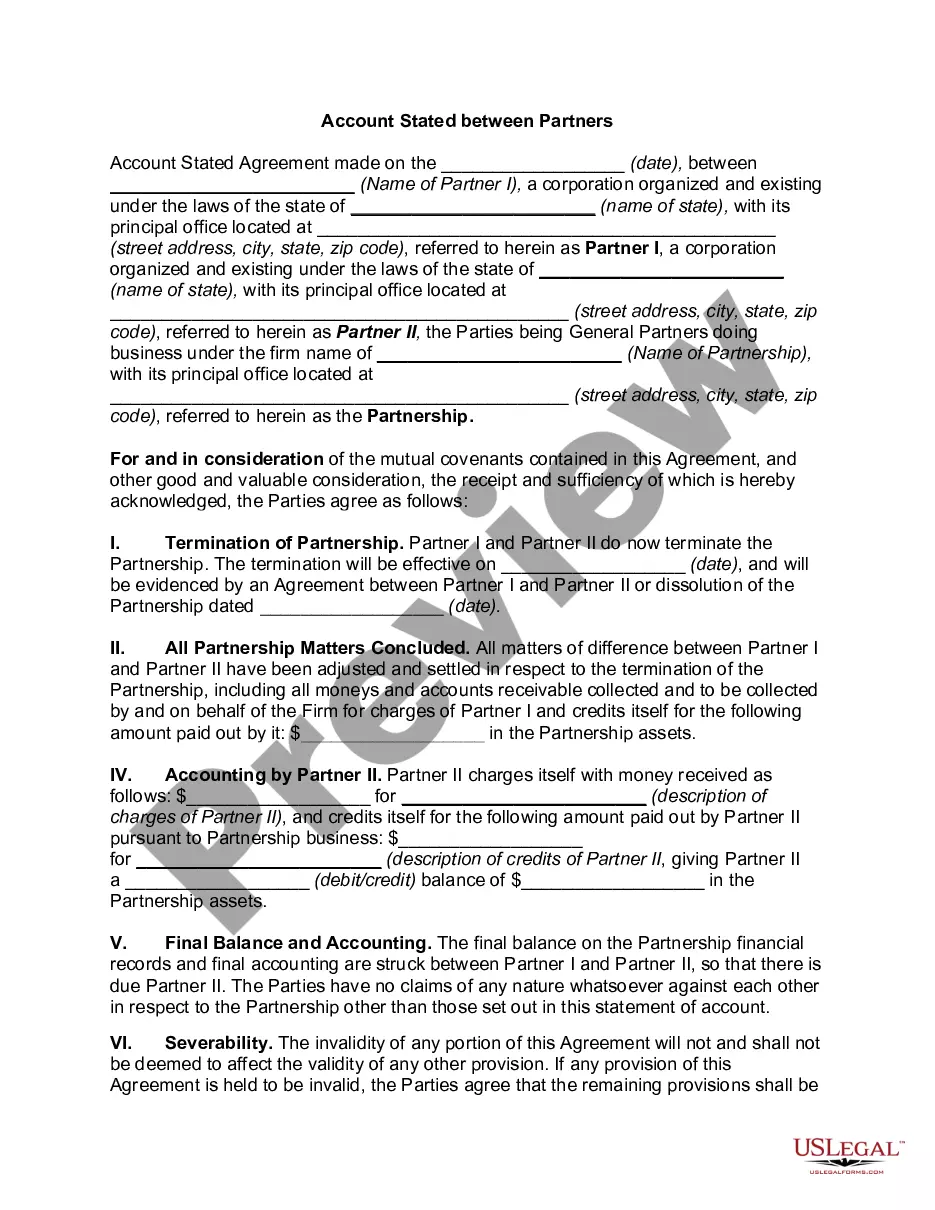

Indiana Account Stated Between Partners and Termination of Partnership

Description

How to fill out Account Stated Between Partners And Termination Of Partnership?

Are you presently in the situation the place you will need paperwork for either business or person functions just about every day time? There are plenty of lawful record templates available online, but getting kinds you can trust is not straightforward. US Legal Forms offers a huge number of develop templates, such as the Indiana Account Stated Between Partners and Termination of Partnership, that are written to fulfill state and federal specifications.

In case you are presently acquainted with US Legal Forms web site and also have your account, simply log in. Afterward, you can down load the Indiana Account Stated Between Partners and Termination of Partnership template.

Unless you offer an profile and need to begin to use US Legal Forms, adopt these measures:

- Find the develop you want and make sure it is for the right metropolis/area.

- Make use of the Preview option to examine the form.

- See the outline to actually have chosen the appropriate develop.

- In case the develop is not what you are trying to find, take advantage of the Search field to obtain the develop that suits you and specifications.

- Whenever you discover the right develop, click on Get now.

- Pick the costs plan you desire, fill out the required information and facts to make your account, and pay for the order utilizing your PayPal or bank card.

- Decide on a convenient paper structure and down load your backup.

Get each of the record templates you have purchased in the My Forms menu. You can get a additional backup of Indiana Account Stated Between Partners and Termination of Partnership at any time, if required. Just click on the needed develop to down load or printing the record template.

Use US Legal Forms, one of the most comprehensive collection of lawful varieties, to conserve time as well as stay away from errors. The services offers appropriately made lawful record templates that can be used for a range of functions. Produce your account on US Legal Forms and begin making your daily life easier.

Form popularity

FAQ

Visit the Indiana Department of Revenue website to close your sole proprietorship business account. Download Form BC-100 and send it to the address on the form (see Resources). Include documentation that proves the business has closed.

5 Key Steps in Dissolving a Partnership Review your partnership agreement. While some partnerships don't require a formal or written agreement, most partners choose to have one anyway for protection. ... Discuss with other partners. ... File dissolution papers. ... Notify others. ... Settle and close out all accounts.

A Limited Liability Partnership (LLP) is formed and governed based on the Indiana Uniform Partnership Act. An LLP is considered a blend of a corporation and a partnership. Beyond the assets that were invested in the partnership, none of the partners may be held personally responsible for the actions of other parties.

While both words are concerned with the end of a business partnership, dissolution refers to the process itself, and usually to the departure (or death) of one or more individuals from the entity, while termination refers to the cessation of all operations, including the disposal of all assets.

A deed of dissolution of partnership sets out the terms on which the partners of a partnership agree to dissolve the partnership.

To dissolve your LLC in Indiana, submit one original and one copy of the Indiana Articles of Dissolution (Form 49465) to the Indiana Secretary of State (SOS) by mail or in person. Articles of Dissolution can be filed online if you pay using an IN.gov payment account or a MasterCard, Discover or Visa credit card.

The dissolution process occurs when the entire partnership is terminated. A dissociation, in contrast, occurs when only one partner is attempting to end their association with the partnership. In the dissolution process, any partner may dissolve the partnership at any time by providing a notice of dissolution.

To dissolve a limited partnership in Indiana, you must file a certificate of dissolution with the Secretary of State. Regardless of which type of partnership you have, there are a few other things you'll need to consider when dissolving a partnership in Indiana.