Indiana Living Trust for individual, Who is Single, Divorced or Widow or Widower with Children

Overview of this form

This Living Trust form is a legal document tailored for individuals who are single, divorced, or widowed, and have children. Its primary purpose is to help in managing and transferring assets during one's lifetime and after death without the need for probate. Unlike a will, which only takes effect after death, a Living Trust allows the creator to maintain control over their assets while alive and ensures a seamless transfer to beneficiaries upon passing.

Form components explained

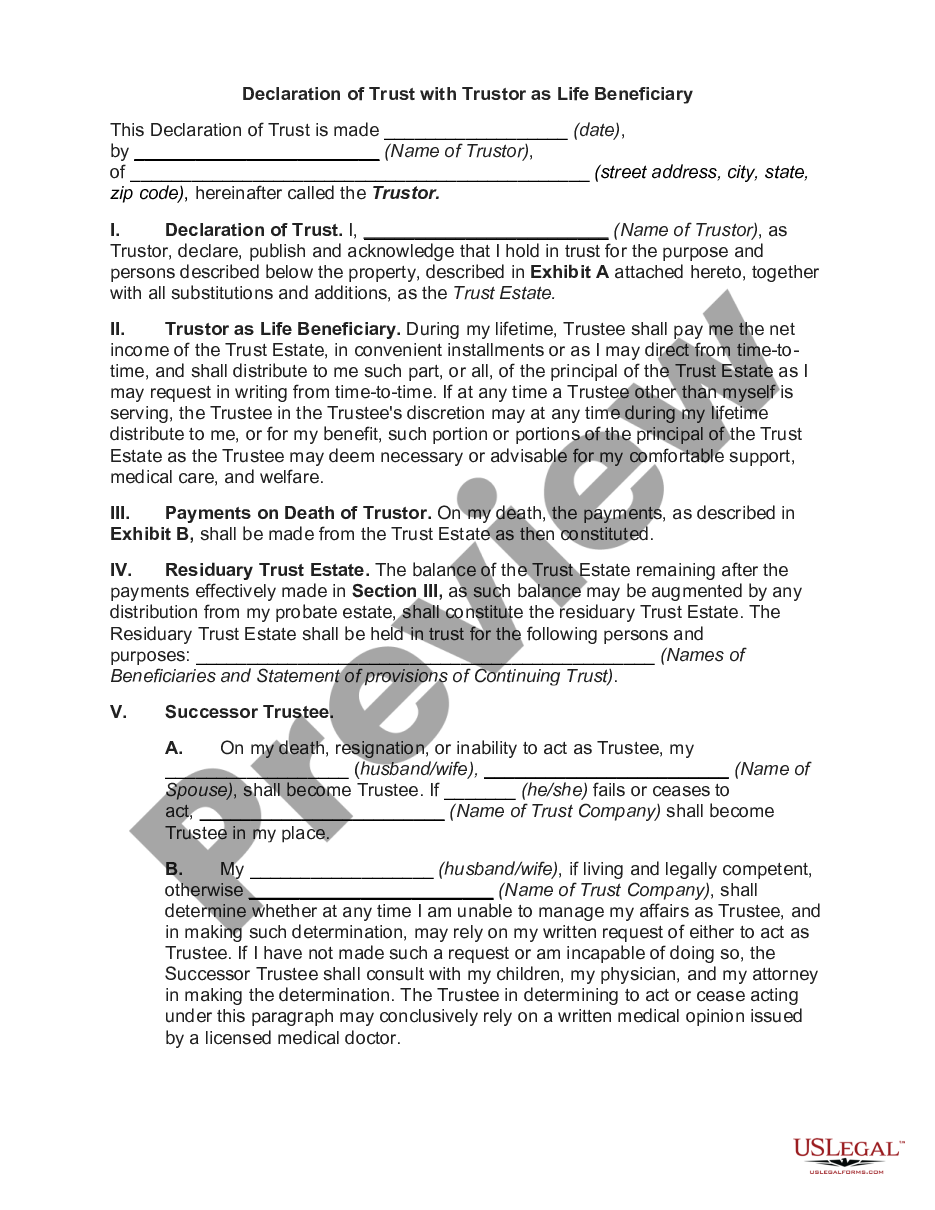

- Article I: Name of the Trust, allowing flexibility in naming the document.

- Article II: Identification of the Trustor, beneficiaries, and their relationships.

- Article III: Appointment of the Trustee or Successor Trustee.

- Article IV: Details regarding the assets included in the Trust.

- Article VIII: Guidelines on trust administration during the Trustor's lifetime and after death.

When to use this form

This form is beneficial when you wish to establish a plan for your assets, especially if you are a single parent, widowed, or divorced. It is ideal for those wanting to avoid the probate process, ensuring that assets are managed and distributed according to your wishes efficiently. This form is also useful during periods of incapacity, allowing for a smooth transition in asset management without court intervention.

Who should use this form

- Individuals who are single, divorced, or widowed.

- Parents with one or more children looking to manage their estate.

- Persons interested in avoiding probate for their assets.

- Individuals who want to retain control over their assets during their lifetime.

Steps to complete this form

- Identify the Trustor by entering your name and address as the creator of the Trust.

- Name your chosen Trustee and any Successor Trustees in the appropriate sections.

- List your children or beneficiaries clearly, including any specifications regarding their share of the Trust assets.

- Outline the assets you wish to include in the Trust, ensuring they are properly described in Schedule A.

- Sign and date the Trust agreement in the presence of a notary public if necessary.

Is notarization required?

This form does not typically require notarization unless specified by local law. However, having a notary public involved can add a layer of authenticity and legal standing to the document.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to notarize the document when required, which can invalidate the Trust.

- Omitting beneficiaries or incorrectly identifying them, causing potential disputes later.

- Not fully funding the Trust by transferring assets into it, leading to probate for unfunded assets.

- Neglecting to review and update the Trust after major life changes.

Benefits of using this form online

- Convenience of completing the form at your own pace from any location.

- Editability allows you to make necessary changes easily before finalizing.

- Access to reliable templates that are drafted by licensed attorneys.

- Affordability compared to traditional legal services.

Key takeaways

- A living trust can provide significant advantages over a traditional will, including avoiding probate.

- This specific trust is tailored for those who are single, divorced, or widowed with children.

- It ensures your assets are managed as per your wishes during your lifetime and distributed to your heirs after your death.

Looking for another form?

Form popularity

FAQ

A survivor's trust typically benefits the surviving spouse, allowing them access to the trust assets. In contrast, a marital trust aims to support the spouse during their lifetime and ultimately passes assets to other beneficiaries after their death. If you are looking into an Indiana Living Trust for an individual who is single, divorced, or widowed with children, understanding these differences can help you choose the right structure for your estate plan.

A living trust is designed to allow for the easy transfer of the trust creator or settlor's assets while bypassing the often complex and expensive legal process of probate. Living trust agreements designate a trustee who holds legal possession of assets and property that flow into the trust.

A will can also be declared invalid if someone proves in court that it was procured by undue influence. This usually involves some evil-doer who occupies a position of trust -- for example, a caregiver or adult child -- manipulating a vulnerable person to leave all, or most, of his property to the manipulator instead

Paperwork. Setting up a living trust isn't difficult or expensive, but it requires some paperwork. Record Keeping. After a revocable living trust is created, little day-to-day record keeping is required. Transfer Taxes. Difficulty Refinancing Trust Property. No Cutoff of Creditors' Claims.

Bank accounts. Brokerage or investment accounts. Retirement accounts and pension plans. A life insurance policy.

Property in a living trust. One of the ways to avoid probate is to set up a living trust. Retirement plan proceeds, including money from a pension, IRA, or 401(k) Stocks and bonds held in beneficiary. Proceeds from a payable-on-death bank account.

A trust is a fiduciary arrangement that allows a third party, or trustee, to hold assets on behalf of a beneficiary or beneficiaries. Trusts can be arranged in many ways and can specify exactly how and when the assets pass to the beneficiaries.Other benefits of trusts include: Control of your wealth.

An executor of a will cannot take everything unless they are the will's sole beneficiary.However, the executor cannot modify the terms of the will. As a fiduciary, the executor has a legal duty to act in the beneficiaries and estate's best interests and distribute the assets according to the will.

You and your spouse may have one of the most common types of estate plans between married couples, which is a simple will leaving everything to each other. With this type of plan, you leave all of your assets outright to your surviving spouse. The kids or other beneficiaries only get something after you are both gone.

A living trust, specifically a revocable living trust, is a legal document that places your assetsinvestments, bank accounts, real estate, vehicles and valuable personal propertyin trust for your benefit during your lifetime, and spells out where you'd like these things to go upon your death.