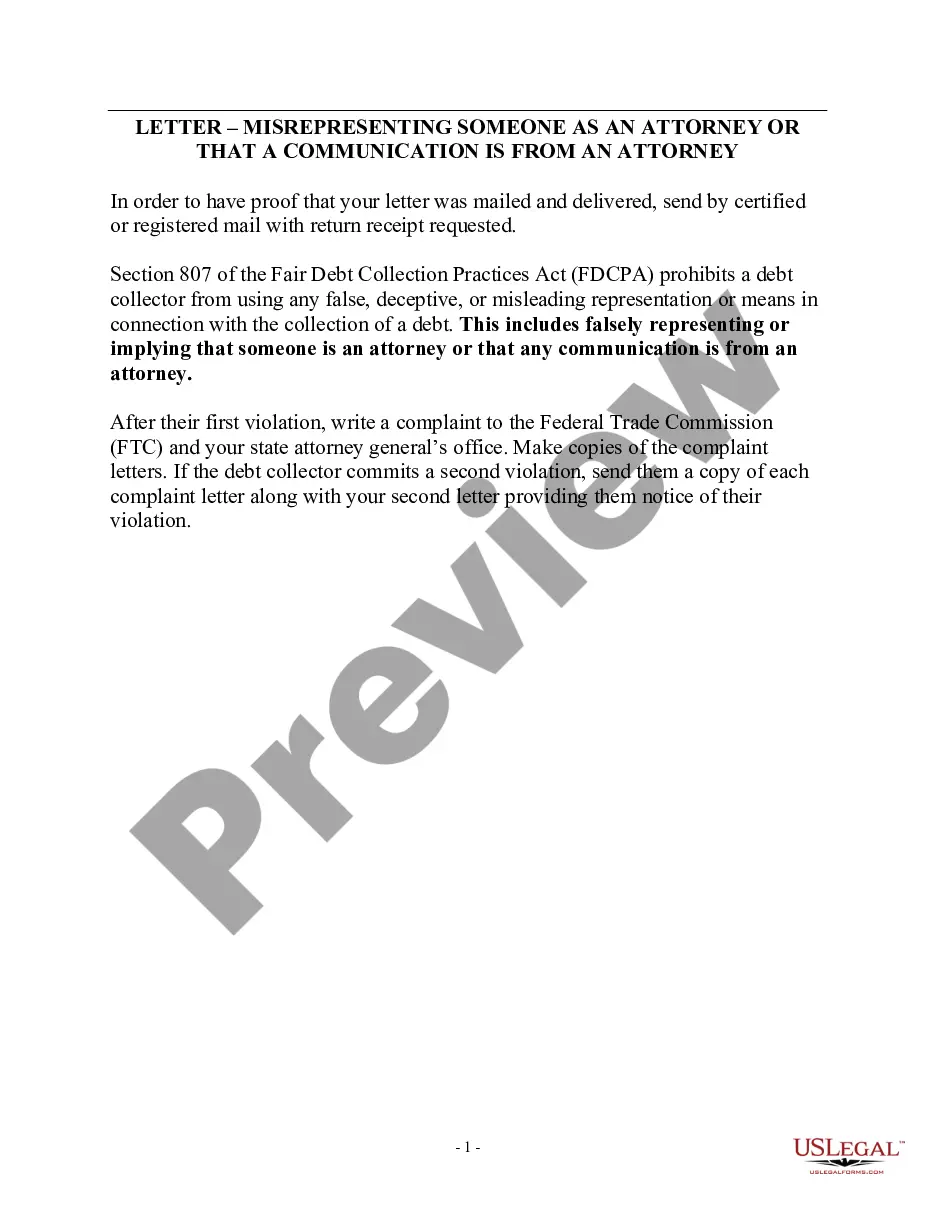

Illinois Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself

Description

How to fill out Notice Of Violation Of Fair Debt Act - Creditor Misrepresented Himself?

US Legal Forms - one of the largest collections of approved templates in the United States - offers a diverse selection of legal document formats that you can download or create.

By utilizing the website, you can access numerous forms for business and personal purposes, organized by categories, states, or keywords. You'll find the latest versions of forms such as the Illinois Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself in just minutes.

If you already have an account, Log In and download the Illinois Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself from the US Legal Forms library. The Download button will be visible on every form you review. You can access all previously downloaded forms in the My documents section of your account.

Process the transaction. Use your Visa, Mastercard, or PayPal account to finalize the transaction.

Select the format and download the form onto your device. Make modifications. Fill out, edit, and print and sign the downloaded Illinois Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself. Each template you added to your account does not expire and is your property indefinitely. Therefore, if you want to download or print another copy, simply head to the My documents section and click on the form you need. Access the Illinois Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself with US Legal Forms, the most comprehensive library of legal document templates. Utilize a multitude of professional and state-specific templates that fulfill your business or personal needs and requirements.

- If you are using US Legal Forms for the first time, here are simple steps to get started.

- Make sure you select the correct form for your city/state. Click the Review button to examine the form's details.

- Check the form description to ensure you have selected the appropriate form.

- If the form does not meet your needs, use the Search feature at the top of the page to find the one that does.

- If you are satisfied with the form, confirm your choice by clicking the Purchase now button.

- Then, choose the pricing plan you prefer and provide your information to register for the account.

Form popularity

FAQ

The most common violation of the Fair Debt Collection Practices Act involves debt collectors calling consumers outside of legally permitted times. Additionally, misrepresenting the debt amount or failing to provide written notice of the debt are also frequent violations. If you experience such misconduct, consider filing an Illinois Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself to assert your rights.

Debts that may not be covered are those that are not incurred voluntarily, such as income taxes, parking and speeding tickets, and domestic support obligations like child support and alimony, or spousal support.

Under the Fair Credit Reporting Act, debts can appear on your credit report generally for seven years and in a few cases, longer than that. Under state laws, if you are sued about a debt, and the debt is too old, you may have a defense to the lawsuit.

Highlights: Most negative information generally stays on credit reports for 7 years. Bankruptcy stays on your Equifax credit report for 7 to 10 years, depending on the bankruptcy type. Closed accounts paid as agreed stay on your Equifax credit report for up to 10 years.

On debts based on written contracts, the statute of limitation is 10 years. On unwritten contracts, it's 5 years.

According to Illinois law, the statute of limitations on credit card debt is five years. Statutes of limitations are used by all states to prevent legal action on claims that have become old or "stale." A state may have dozens of different statutes of limitations applying to hundreds of different types of claims.

If a debt collector fails to verify the debt but continues to go after you for payment, you have the right to sue that debt collector in federal or state court. You might be able to get $1,000 per lawsuit, plus actual damages, attorneys' fees, and court costs.

They can sue you, or threaten to sue you, in court. They can send you letters or call you. Within 5 days of the first time they contact you, debt collectors have to send you a written notice about the debt (see below). If you receive a Complaint and Summons , this means a lawsuit has been filed.

The FDCPA broadly prohibits a debt collector from using 'any false, deceptive, or misleading representation or means in connection with the collection of any debt. ' 15 U.S.C. § 1692e. The statute enumerates several examples of such practices, 15 U.S.C.

The Fair Debt Collection Practices Act (FDCPA) The FDCPA prohibits debt collection companies from using abusive, unfair or deceptive practices to collect debts from you.