Illinois Promissory Note

What is this form?

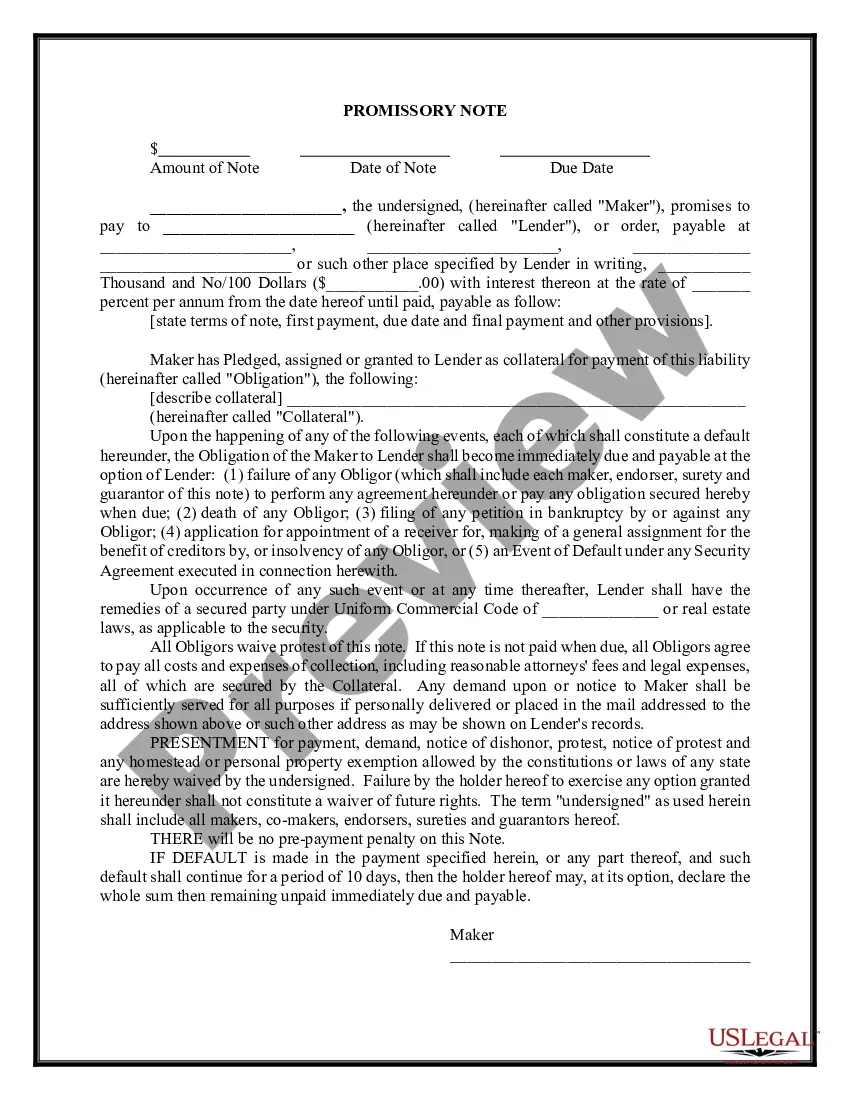

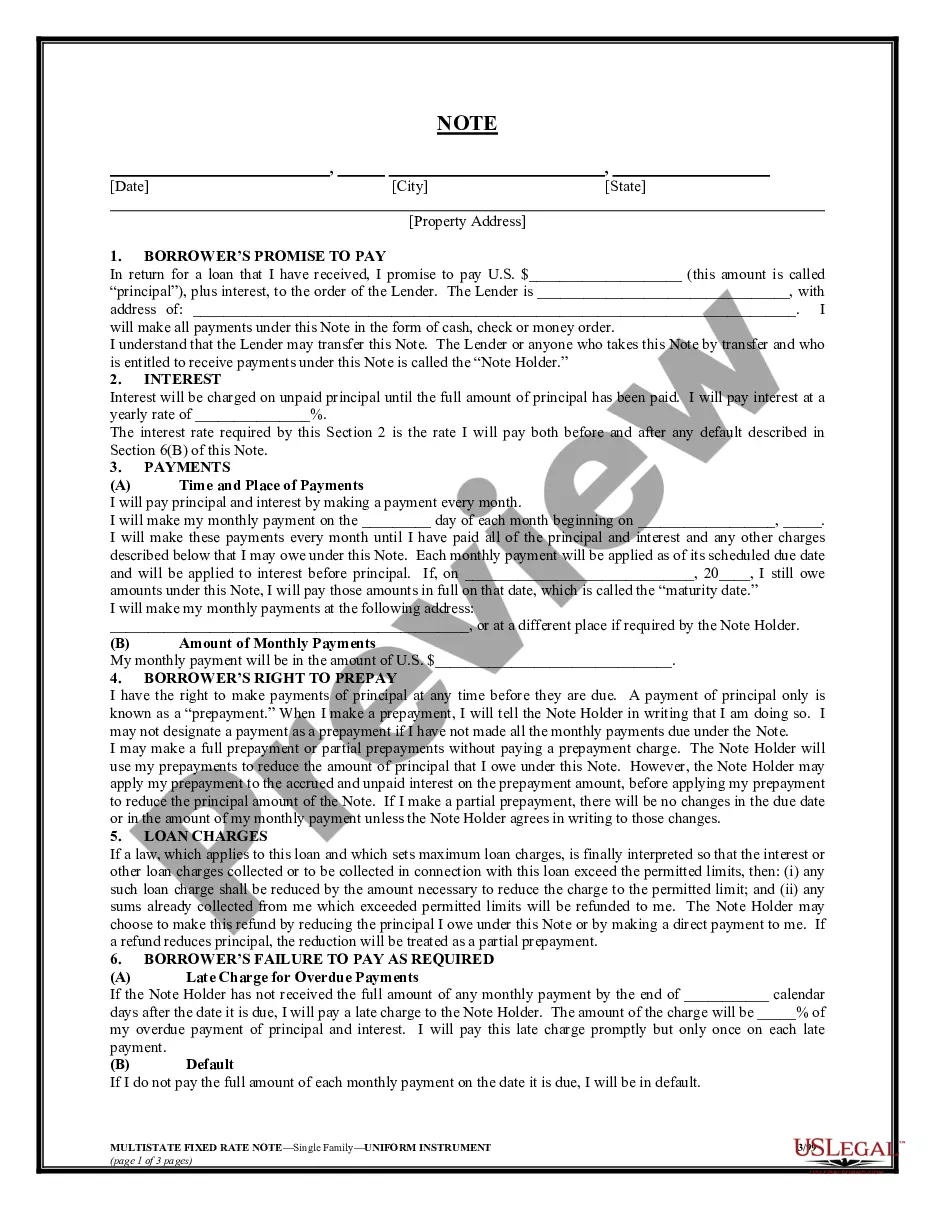

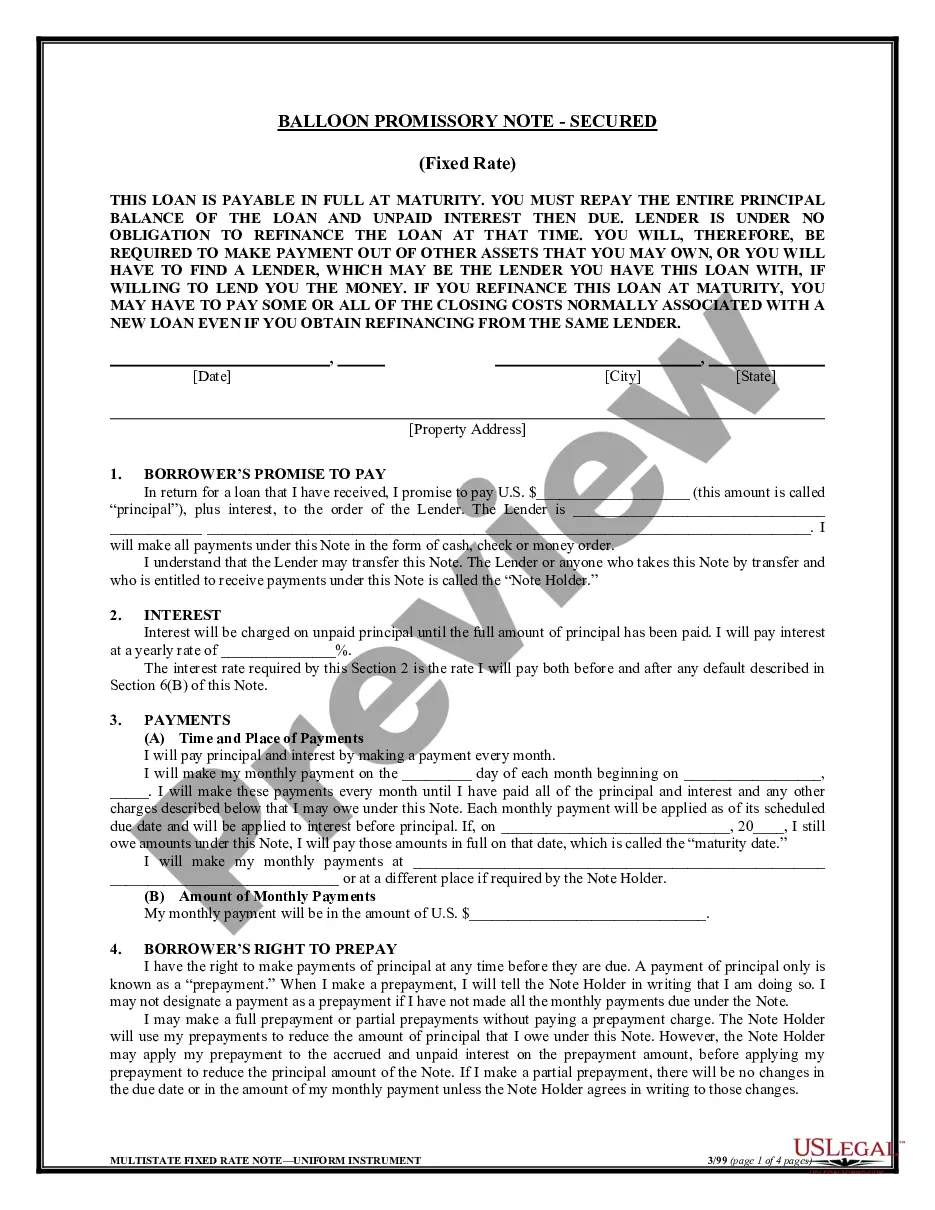

A promissory note is a written promise between a creditor and a debtor that details the terms of a loan. This legal document outlines the amount borrowed, the repayment schedule, and what happens in the event of default. Unlike informal agreements, a promissory note provides a clear framework for repayment and protects both parties' rights.

Key parts of this document

- Principal amount: Specifies the total loan amount due.

- Interest rate: Details the rate of interest to be paid on the loan.

- Payment schedule: Outlines when and how payments will be made.

- Late charge: Indicates any fees applicable for late payments.

- Default clause: Describes what happens if the debtor fails to repay.

- Guarantor: Names any individuals guaranteeing repayment of the loan.

Common use cases

This promissory note should be used when one party lends money to another and formalizes the arrangement with a legally binding document. It is particularly useful in cases of personal loans, business loans, or loans between family members to ensure that terms are clear and agreed upon.

Who needs this form

This promissory note is suitable for:

- Individuals or businesses borrowing money.

- Lenders who want to formalize loan agreements.

- Parties seeking to clarify the terms of a loan transaction.

- Anyone requiring legal protection for loan conditions and repayment scheduling.

How to complete this form

- Identify the creditor and debtor: Fill in the full names of both parties involved.

- Specify the loan amount: Clearly state the total amount of the loan.

- Detail the repayment terms: Include the interest rate and payment schedule.

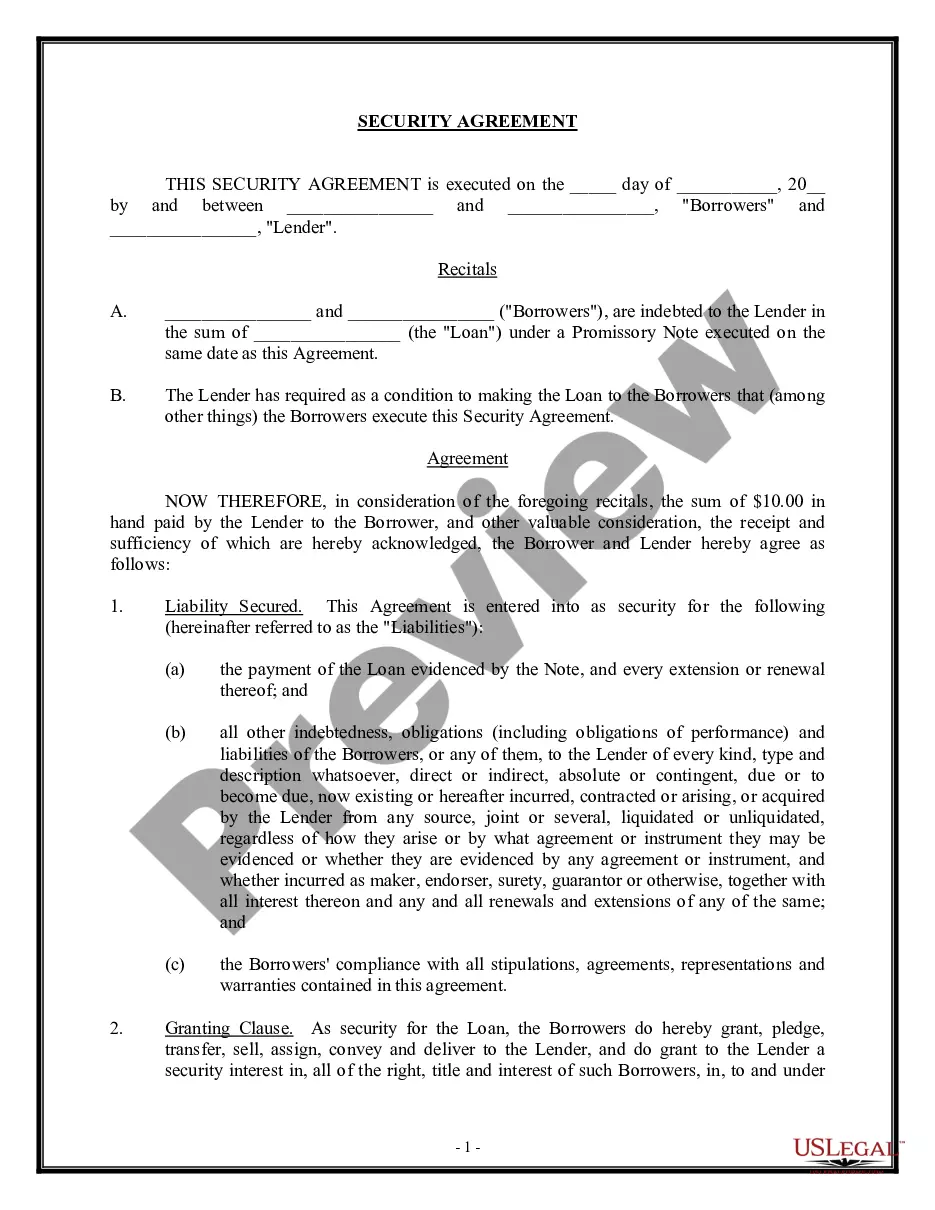

- Add any security provisions: Note any collateral securing the loan, if applicable.

- Sign and date: Ensure both parties sign and date the document to make it legally binding.

Does this document require notarization?

In most cases, this form does not require notarization. However, some jurisdictions or signing circumstances might. US Legal Forms offers online notarization powered by Notarize, accessible 24/7 for a quick, remote process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Not specifying the interest rate clearly.

- Failing to outline consequences for late payments.

- Omitting signatures or dates from the document.

- Not including necessary details about collateral, if applicable.

Advantages of online completion

- Convenience: Download and fill out the form from anywhere.

- Editability: Easily make changes if needed before finalizing.

- Reliability: Forms created by licensed attorneys ensure legal validity.

- Time-saving: Quick access to necessary documents without visiting a lawyer.

Looking for another form?

Form popularity

FAQ

A valid Illinois promissory note must contain specific elements, including the principal amount, interest rate, due date, and the names of the parties involved. Additionally, it should be in writing and signed by the maker of the note. These essentials ensure clarity and enforceability.

A Promissory Note must always be written by hand. It must include all the mandatory elements such as the legal names of the payee and maker's name, amount being loaned / to be repaid, full terms of the agreement and the full amount of liability, beside other elements.

Writing the Promissory Note Terms You can use a template or create a promissory note online. But before you begin, you'll need to gather some information and make decisions about the way the loan will be structured. First, you'll need the names and addresses of both the lender (or "payee") and the borrower.

Write the date of the writing of the promissory note at the top of the page. Write the amount of the note. Describe the note terms. Write the interest rate. State if the note is secured or unsecured. Include the names of both the lender and the borrower on the note, indicating which person is which.

Borrower and Lender Details. A promissory note outlines information about both parties including the names, streets addresses, city, state and zip code of each party. Loan Information. Legal Language. Signatures. Warnings.

A promissory note basically includes the name of both parties (lender and borrower), date of the loan, the amount, the date the loan will be repaid in full, frequency of loan payments, the interest rate charged on the loan payments, and any security agreement.

Amount of repayment. Repayment terms. Interest rate. Default penalties.

However, it is still smart to contact a lawyer to help you prepare a personal promissory note, even if you already used an online template. A lawyer can prepare and/or review the note to ensure that all state law requirements are included. This will help with enforceability if there are any issues down the road.

In order for a promissory note to be valid, both the lender and the borrower must sign the documentation. If you are a co-signer for the loan, you are required to sign the promissory note. Being a co-signer requires you to repay the loan amount in the instance that the borrower defaults on payment.