Illinois Collection Letter - Consumer Debtor

About this form

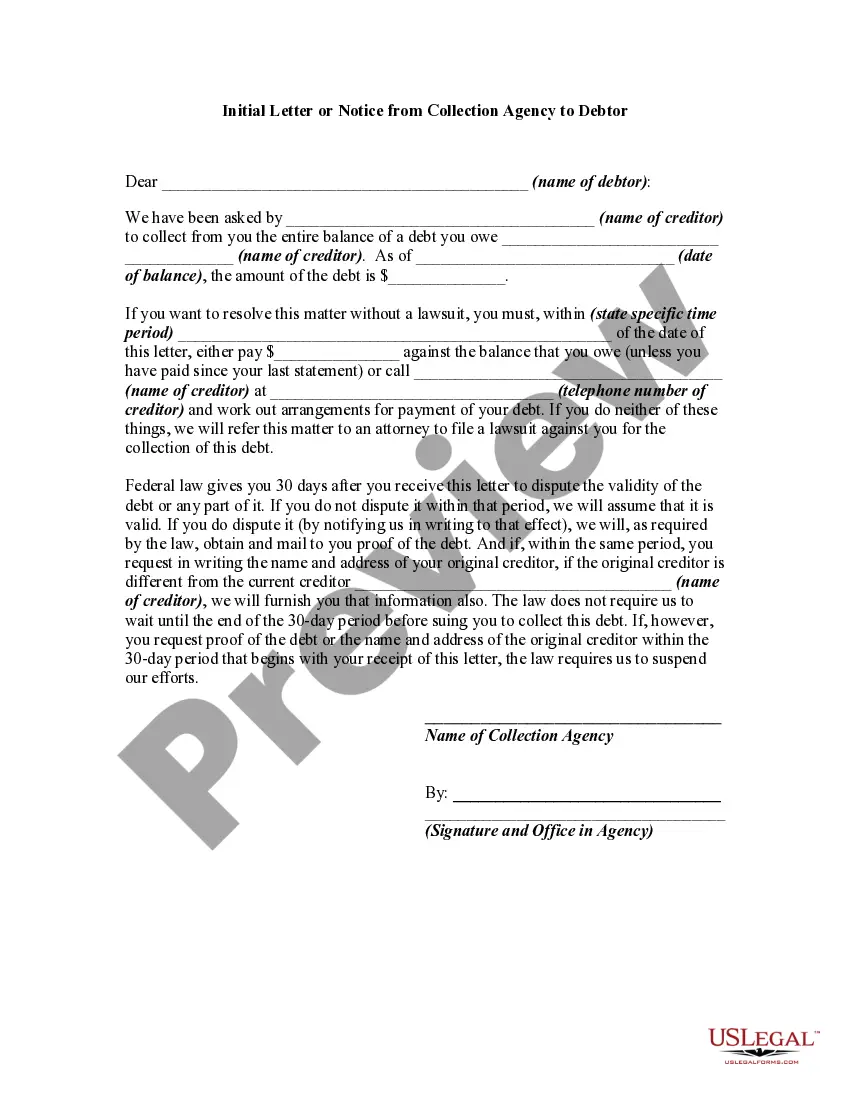

The Collection Letter - Consumer Debtor is a formal correspondence used by a creditor to request payment from a debtor for a past due account. This letter outlines the outstanding balance, the services provided, and the consequences of non-payment, setting it apart from other collection notices. It serves as a key step in the collection process, clearly stating the creditor's intentions while adhering to legal requirements under debt collection laws.

Main sections of this form

- Creditor's information: Names and contact details of the creditor.

- Debtor's details: The debtor's name and contact information.

- Outstanding balance: The total amount owed, including any extras.

- Actions for non-payment: Clear statements regarding potential legal actions if payment is not received.

- Dispute notification: Information on the debtor's rights to dispute the debt within a specified period.

- Response deadline: A date by which the debtor must respond to the letter.

When this form is needed

This form is utilized when a debtor has failed to pay the amount due for services rendered. It is appropriate for use after previous attempts at collection have been made but have not resulted in payment. Common scenarios include unpaid invoices for goods or services provided, missed loan payments, or unresolved fees.

Who this form is for

- Businesses seeking to collect outstanding debts from consumers.

- Freelancers or independent contractors owed money for services provided.

- Landlords dealing with overdue rents from tenants.

- Service providers requiring payment for completed work.

Instructions for completing this form

- Identify the creditor's details: Fill in the name, address, and contact information of the creditor.

- Enter the debtor's information: Provide the relevant details of the debtor, including their name and address.

- Specify the outstanding balance: Clearly state the total amount owed, ensuring it includes all applicable fees and extras.

- Set a response deadline: Indicate a date by which the debtor must respond to avoid further actions.

- Review the form for accuracy: Double-check all entries before sending to ensure clarity and correctness.

Does this form need to be notarized?

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to include precise contact information for both creditor and debtor.

- Not clearly stating the outstanding balance, leading to confusion.

- Not setting a reasonable deadline for the debtor's response.

- Using ambiguous language that may mislead the debtor.

- Neglecting to inform the debtor of their rights under debt collection laws.

Benefits of completing this form online

- Convenience: Easily downloadable and editable formats allow for quick customization.

- Reliability: Templates are crafted by licensed attorneys, ensuring legal soundness.

- Time-saving: Generate a collection letter swiftly without the need for lengthy legal consultations.

- Accessibility: Access the form anytime, from anywhere, streamlining the debt collection process.

Legal use & context

- The Collection Letter is a legal tool for initiating collection procedures.

- Using this form enhances the credibility of your claim for outstanding debts.

- Failure to comply with the Federal Debt Collection Act can result in legal repercussions for the creditor.

Main things to remember

- The Collection Letter for Consumer Debtor is essential for formal collection efforts.

- It outlines the debtor's responsibilities and consequences for non-payment.

- Proper completion of this form can encourage debt resolution before taking further legal action.

Looking for another form?

Form popularity

FAQ

In Illinois, the Statute of Limitations on debt ranges from 5 years to 10 years. Some debt collection agencies buy old debts, out the Statute of Limitation period for pennies on the dollar from the original creditor in order to collect what they can.

Even though debts still exist after seven years, having them fall off your credit report can be beneficial to your credit score.Note that only negative information disappears from your credit report after seven years. Open positive accounts will stay on your credit report indefinitely.

In Illinois, the Statute of Limitations on debt ranges from 5 years to 10 years. Some debt collection agencies buy old debts, out the Statute of Limitation period for pennies on the dollar from the original creditor in order to collect what they can.

The statute of limitations in Illinois is five years for open accounts for debt collections and oral contracts and ten years for written contracts. The good news is that the debts are time-barred and you can't be sued for them.

There is no statute of limitations on how long a creditor can attempt to collect an unpaid debt, but there is a deadline for when they can still use litigation to receive a court judgment against the debtor.

How Long Can a Debt Collector Pursue an Old Debt? Each state has a law referred to as a statute of limitations that spells out the time period during which a creditor or collector may sue borrowers to collect debts. In most states, they run between four and six years after the last payment was made on the debt.

Although there's no debtor's prison, it's possible to wind up in jail in a collection case. But, not because you owe money, or can't pay it. Jail can only happen if you're able to pay, and refuse to, or if you miss a court-ordered court date.

We contract with collection agencies to help us collect the amount of tax, penalty, and interest that you owe.

There is no statute of limitations on how long a creditor can attempt to collect an unpaid debt, but there is a deadline for when they can still use litigation to receive a court judgment against the debtor.Creditors can request methods of enforcing the court order, such as wage garnishment.