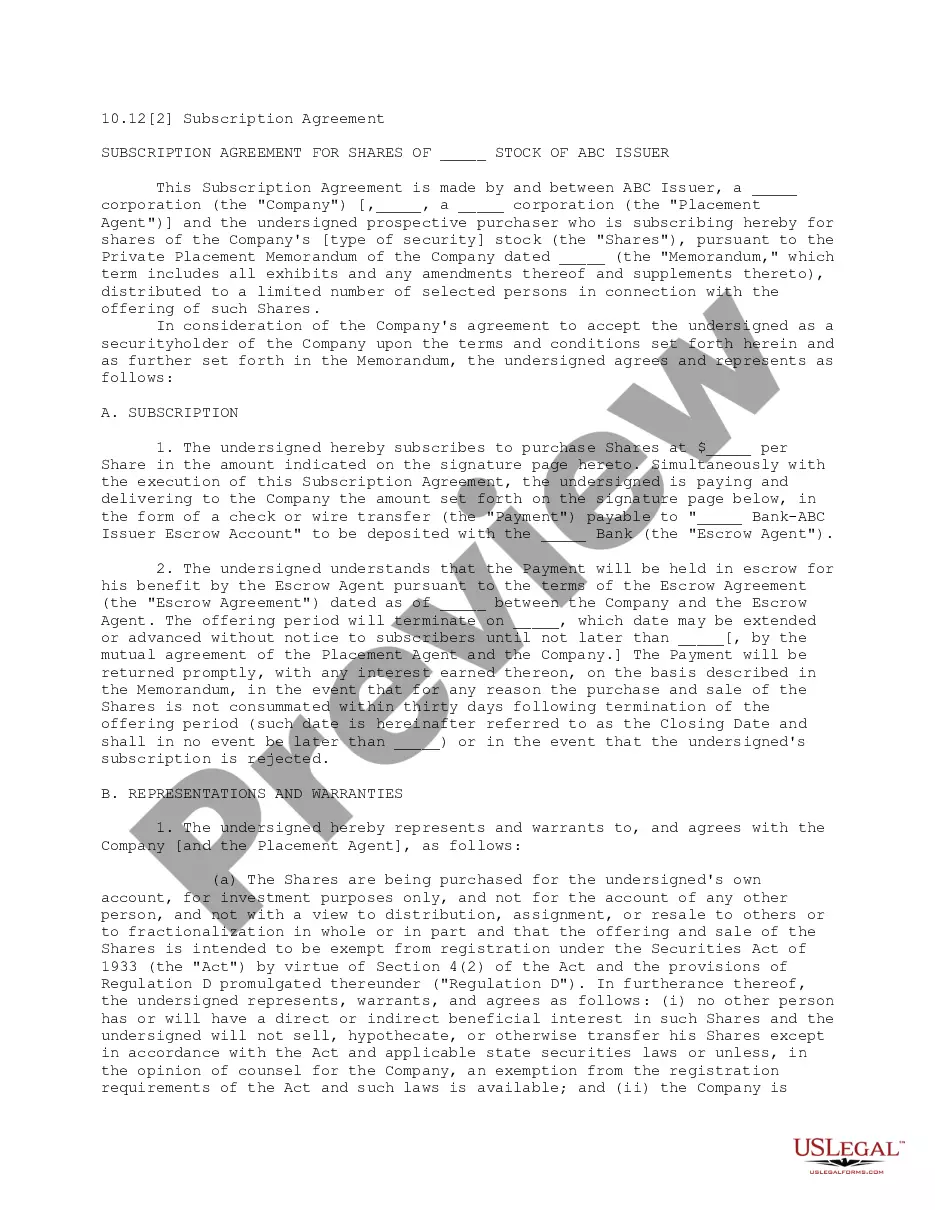

Idaho Subscription Agreement - A Section 3C1 Fund

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Subscription Agreement - A Section 3C1 Fund?

It is possible to devote several hours on-line looking for the legitimate document template that suits the federal and state requirements you will need. US Legal Forms supplies a large number of legitimate kinds which can be reviewed by pros. It is possible to acquire or printing the Idaho Subscription Agreement - A Section 3C1 Fund from the service.

If you already possess a US Legal Forms account, you can log in and click on the Acquire button. Afterward, you can complete, change, printing, or indicator the Idaho Subscription Agreement - A Section 3C1 Fund. Each and every legitimate document template you get is your own property eternally. To acquire an additional backup of the bought develop, go to the My Forms tab and click on the corresponding button.

Should you use the US Legal Forms site initially, adhere to the basic recommendations under:

- Initial, be sure that you have selected the best document template for that region/metropolis of your choice. Read the develop explanation to ensure you have picked out the correct develop. If readily available, utilize the Preview button to check throughout the document template also.

- In order to find an additional variation of the develop, utilize the Search field to obtain the template that suits you and requirements.

- After you have identified the template you want, click Acquire now to proceed.

- Select the rates prepare you want, type your qualifications, and sign up for a free account on US Legal Forms.

- Total the financial transaction. You may use your charge card or PayPal account to pay for the legitimate develop.

- Select the structure of the document and acquire it in your product.

- Make alterations in your document if required. It is possible to complete, change and indicator and printing Idaho Subscription Agreement - A Section 3C1 Fund.

Acquire and printing a large number of document layouts using the US Legal Forms website, which offers the biggest selection of legitimate kinds. Use professional and condition-particular layouts to deal with your business or personal requires.

Form popularity

FAQ

3(c)(1) In other words, 3C1 allows private funds with 100 or fewer investors (and venture capital funds with fewer than 250 investors) and no plans for an initial public offering to sidestep SEC registration and other requirements, including ongoing disclosure and restrictions on derivatives trading.

Accredited investors can invest only in 3(c)(1) funds, whereas qualified purchasers can typically invest in both 3(c)(1) funds and 3(c)(7) funds. A 3(c)(1) fund allows only 100 accredited investors, or 250 accredited investors if the fund size is less than $10M.

Analysis. Section 3(c)(11) of the 1940 Act, in pertinent part, excepts from the definition of "investment company" any "employee's stock bonus, pension, or profit-sharing trust which meets the requirements for qualification under section 401 of the Internal Revenue Code of 1986" (i.e., the "single trust exception").

Section 3(a)(1) of the 1940 Act defines the term ?investment company.? Specifically, Section 3(a)(1)(A) of the 1940 Act defines ?investment company? to mean ?any issuer which is or holds itself out as being engaged primarily, or proposes to engage primarily, in the business of investing, reinvesting, or trading in ...

Private funds must not plan to issue an IPO and their investors must be qualified purchases to qualify for the 3C7 exemption. There is no maximum limit for the number of purchasers of 3C7 funds. In contrast to 3C7, 3C1 funds deal with no more than 100 accredited investors.

Section 11(a) of the Investment Company Act prohibits a registered open-end investment company or its principal underwriter from making an exchange offer to holders of securities of that company or of any other open-end investment company on any basis other than the relative net asset values of the securities to be ...

A 3(c)(1) fund is a pooled investment vehicle that is excluded from the definition of investment company in the Investment Company Act because it has no more than 100 beneficial owners (or, in the case of a qualifying venture capital fund, 250 beneficial owners) and otherwise meets criteria outlined in Section 3(c)(1) ...

For the purpose of section 3(c)(1) of the Act, beneficial ownership by a com- pany owning 10 per centum or more of the outstanding voting securities of any issuer which is a small business in- vestment company licensed to operate under the Small Business Investment Act of 1958, or which has received from the Small ...

3(c)(1) In other words, 3C1 allows private funds with 100 or fewer investors (and venture capital funds with fewer than 250 investors) and no plans for an initial public offering to sidestep SEC registration and other requirements, including ongoing disclosure and restrictions on derivatives trading.

3(c)(1) In other words, 3C1 allows private funds with 100 or fewer investors (and venture capital funds with fewer than 250 investors) and no plans for an initial public offering to sidestep SEC registration and other requirements, including ongoing disclosure and restrictions on derivatives trading.