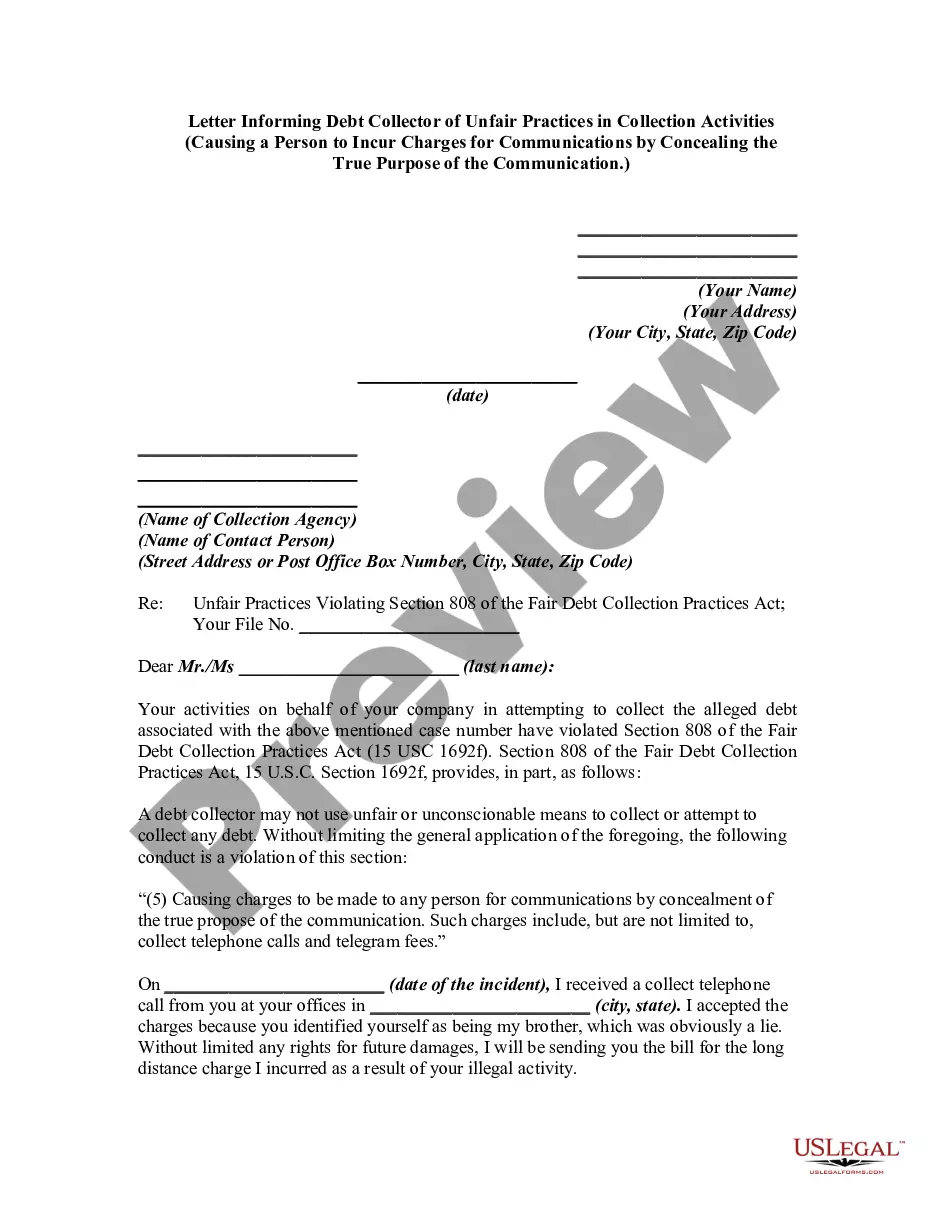

A debt collector may not use unfair or unconscionable means to collect a debt. This includes causing a person to incur charges for communications by concealing the true propose of the communication.

Hawaii Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication

Category:

State:

Multi-State

Control #:

US-DCPA-44

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

How to fill out Notice To Debt Collector - Causing A Consumer To Incur Charges For Communications By Concealing The Purpose Of The Communication?

US Legal Forms - one of the largest collections of legal documents in the United States - offers a broad selection of legal form categories that you can obtain or print.

By using the website, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords.

You can find the most recent versions of forms such as the Hawaii Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication in moments.

If the form does not meet your requirements, use the Lookup box at the top of the screen to identify the one that does.

If you are satisfied with the form, confirm your selection by clicking on the Purchase now button. Then, choose the pricing plan you prefer and provide your details to sign up for an account.

- If you have a current membership, Log In and obtain the Hawaii Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication from the US Legal Forms catalog.

- The Download option will be visible on every document you access.

- You can access all of your previously saved forms in the My documents section of your account.

- If you are using US Legal Forms for the first time, here are some simple steps to help you get started.

- Ensure you have selected the correct form for your area/state.

- Click the Review option to check the content of the form.

Form popularity

FAQ

To determine if a debt collector's email is legitimate, check for official branding, such as a company logo, and verify the sender's address. Additionally, look for proper language and details regarding your debt, which should align with any previous communications. By understanding the guidelines set by the Hawaii Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication, you can better protect yourself against scams.

Don't be surprised if debt collectors slide into your DMs. A new rule allows debt collectors to contact you on social media, text or email not just by phone. The rule, which was approved last year by the Consumer Financial Protection Bureau's former president Kathleen L. Kraninger, took effect Tuesday, Nov.

A debt collector may not use any false, deceptive, or misleading representation or means in connection with the collection of any debt.

I am responding to your contact about collecting a debt. You contacted me by phone/mail, on date and identified the debt as any information they gave you about the debt. I do not have any responsibility for the debt you're trying to collect.

§ 1006.34 Notice for validation of debts.Deceased consumers.Bankruptcy proofs of claim.In general.Subsequent debt collectors.Last statement date.Last payment date.Transaction date.Assumed receipt of validation information.More items...

Your credit card debt, auto loans, medical bills, student loans, mortgage, and other household debts are covered under the FDCPA.

The FDCPA forbids harassing, oppressive, and abusive conductno matter what kind of communication media the debt collector uses. So, this prohibition applies to in-person interactions, telephone calls, audio recordings, paper documents, mail, email, text messages, social media, and other electronic media.

If the consumer notifies the debt collector in writing within the thirty-day period described in subsection (a) of this section that the debt, or any portion thereof, is disputed, or that the consumer requests the name and address of the original creditor, the debt collector shall cease collection of the debt, or any

7 Most Common FDCPA ViolationsContinued attempts to collect debt not owed.Illegal or unethical communication tactics.Disclosure verification of debt.Taking or threatening illegal action.False statements or false representation.Improper contact or sharing of info.Excessive phone calls.

No. If the debt collector knows that an attorney is representing you about the debt, the debt collector must contact your attorney and cannot contact you. The CFPB's Debt Collection Rule clarifying certain provisions of the Fair Debt Collection Practices Act (FDCPA) became effective on November 30, 2021.