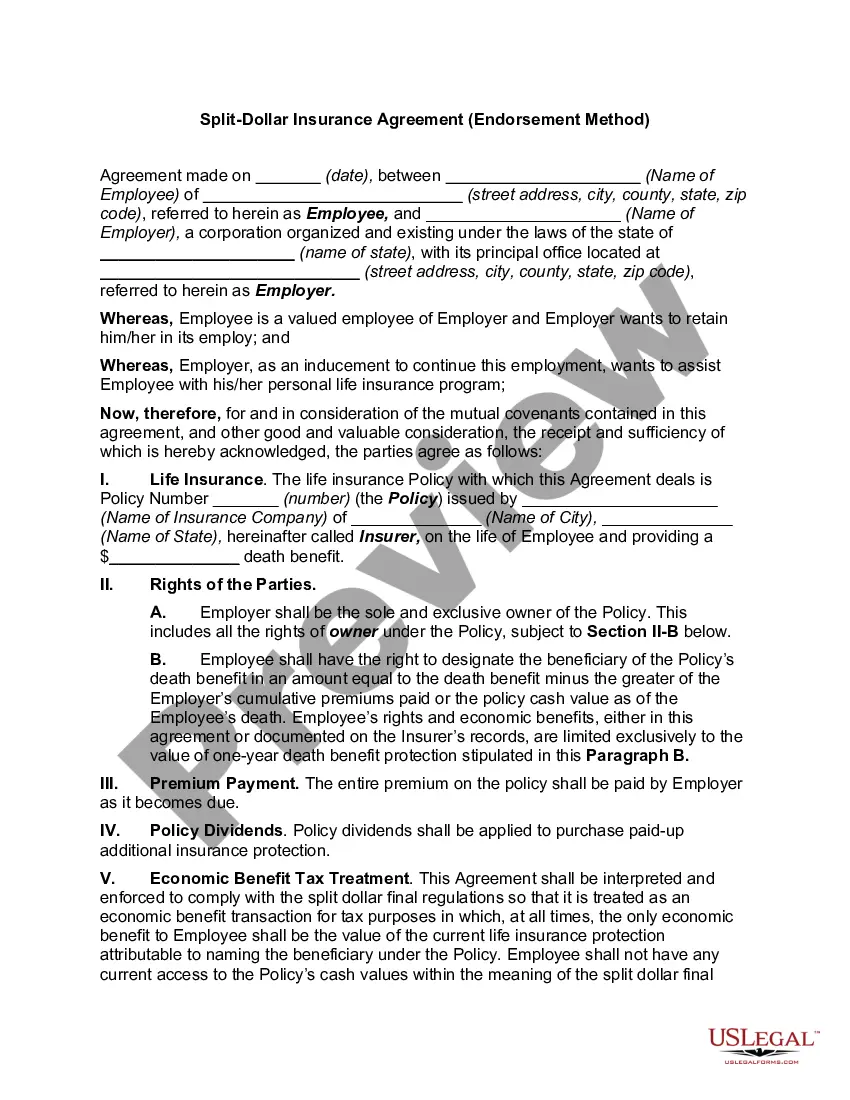

Hawaii Split-Dollar Life Insurance

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Split-Dollar Life Insurance?

US Legal Forms - one of many most significant libraries of legal varieties in America - delivers a wide range of legal record layouts you may acquire or produce. Utilizing the site, you may get thousands of varieties for enterprise and individual purposes, categorized by categories, states, or key phrases.You will find the newest variations of varieties much like the Hawaii Split-Dollar Life Insurance in seconds.

If you already have a membership, log in and acquire Hawaii Split-Dollar Life Insurance through the US Legal Forms catalogue. The Obtain button can look on every single develop you view. You get access to all earlier downloaded varieties from the My Forms tab of the bank account.

If you would like use US Legal Forms the very first time, listed here are easy recommendations to help you get started off:

- Be sure to have picked out the correct develop for your metropolis/county. Click on the Review button to examine the form`s articles. Browse the develop information to ensure that you have chosen the right develop.

- In case the develop does not match your demands, use the Search discipline towards the top of the display screen to find the one who does.

- If you are satisfied with the form, validate your option by visiting the Get now button. Then, opt for the pricing plan you prefer and give your credentials to sign up for an bank account.

- Process the deal. Utilize your charge card or PayPal bank account to complete the deal.

- Select the file format and acquire the form in your device.

- Make adjustments. Fill out, change and produce and indicator the downloaded Hawaii Split-Dollar Life Insurance.

Each and every format you put into your bank account lacks an expiration date and it is your own for a long time. So, if you wish to acquire or produce yet another backup, just check out the My Forms segment and click on in the develop you require.

Gain access to the Hawaii Split-Dollar Life Insurance with US Legal Forms, by far the most considerable catalogue of legal record layouts. Use thousands of specialist and condition-certain layouts that meet your business or individual requires and demands.

Form popularity

FAQ

With a classic split-dollar plan, the employer pays some of the premium (the part that is equal to cash value), while the employee pays the rest. If the employees dies, or the plan is terminated, the surrender cash value is paid to the company, and the death benefits are paid out to beneficiaries.

Split Dollar Loan Regime Agreement & Contract Generally, at the employee's death, the employer receives a portion of the death benefit (usually equal to the total premiums plus interest from the loan) and the employee's beneficiary receives the balance.

Employers are responsible for making split-dollar life insurance premiums, regardless of the plan's type. However, it is important to note that under loan arrangements, employees must repay the premiums via collateral assignments made to their employer.

The best way is to contact the policy's issuer (the life insurance company). Their records are key: even if you see your name listed on an old policy document, the deceased may have changed their beneficiaries (or the allocation of benefits among those beneficiaries) after that document was printed.

If the employer is the owner of the split-dollar policy, the employer's premium payments are treated as providing taxable economic benefits to the executive. The economic benefits include the executive's interest in the policy's accessible cash value and current life insurance protection.

dollar life insurance agreement (or ?splitdollar plan?) is a strategy generally used as an employer benefit or for estate planning involving life insurance. It's an agreement between two or more parties to share the ownership, costs, and benefits of a permanent life insurance policy, like whole life.

There is no cost to the employee-participant unless the policy is transferred to them. This endorsement split-dollar plan is most often used to provide a low-cost death benefit to the employee-participant as a fringe benefit or where the employer wishes to own the policy and/or obtain key person protection.

While split-dollar life insurance arrangements offer numerous advantages, they also come with potential drawbacks, such as complexity, tax considerations, and limited availability. Both employers and employees must carefully weigh the benefits and disadvantages of this type of arrangement before deciding to pursue it.