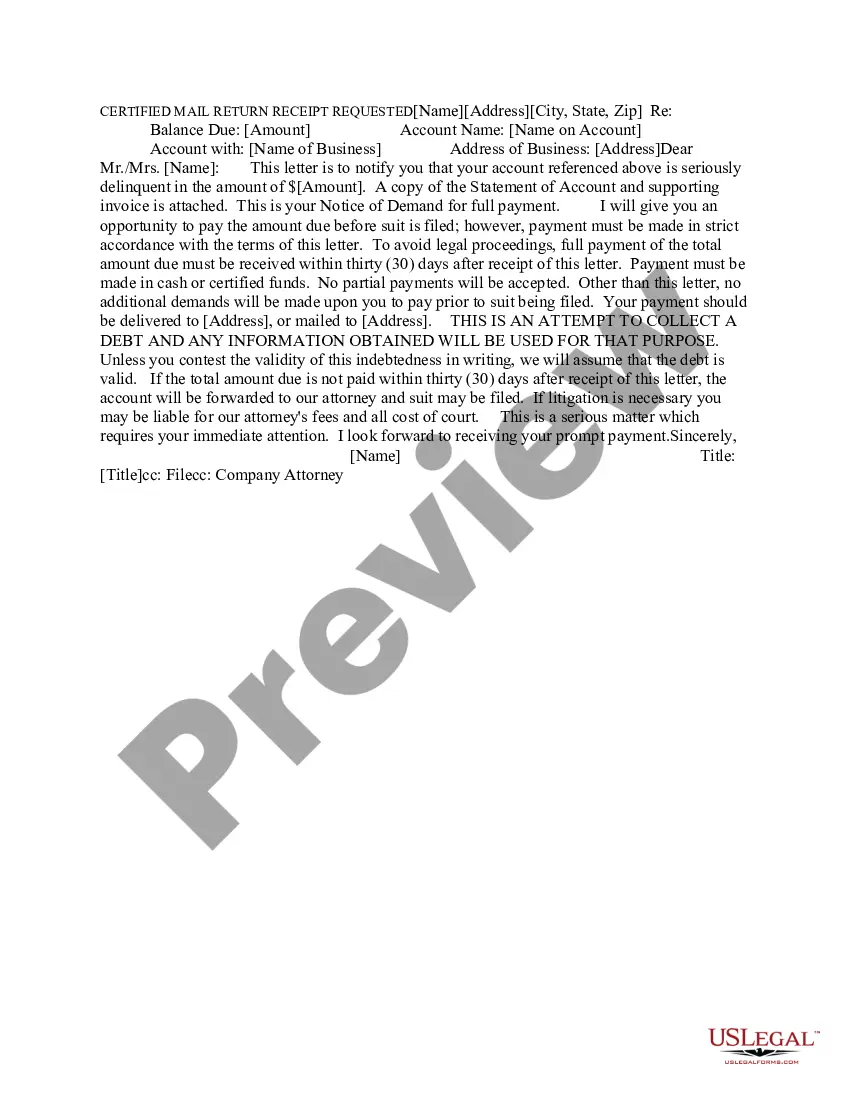

Hawaii Demand for Payment of an Open Account by Creditor

Description

How to fill out Demand For Payment Of An Open Account By Creditor?

You can devote time online searching for the authorized file format that suits the federal and state requirements you require. US Legal Forms gives a huge number of authorized kinds that are examined by specialists. You can easily down load or produce the Hawaii Demand for Payment of an Open Account by Creditor from my support.

If you currently have a US Legal Forms profile, it is possible to log in and then click the Download switch. Following that, it is possible to total, edit, produce, or indication the Hawaii Demand for Payment of an Open Account by Creditor. Each authorized file format you purchase is your own forever. To have another backup associated with a purchased type, visit the My Forms tab and then click the related switch.

If you use the US Legal Forms website for the first time, keep to the basic guidelines under:

- Initial, make certain you have chosen the right file format for your state/city of your choosing. See the type outline to make sure you have picked out the right type. If accessible, make use of the Preview switch to check through the file format as well.

- If you would like get another edition from the type, make use of the Research field to find the format that meets your needs and requirements.

- Once you have located the format you need, click Acquire now to carry on.

- Choose the prices plan you need, type in your references, and register for a free account on US Legal Forms.

- Comprehensive the purchase. You can use your Visa or Mastercard or PayPal profile to purchase the authorized type.

- Choose the formatting from the file and down load it in your device.

- Make adjustments in your file if necessary. You can total, edit and indication and produce Hawaii Demand for Payment of an Open Account by Creditor.

Download and produce a huge number of file themes making use of the US Legal Forms site, which provides the biggest selection of authorized kinds. Use expert and express-specific themes to handle your small business or individual requirements.

Form popularity

FAQ

Open accounts/written contracts: The Hawaii statute of limitations on open accounts and written contracts is six years. Credit card accounts, loans that do not fall within the ambit of the Uniform Commercial Code, and debts arising under other written agreements all fall under the same six year statute of limitations.

Typical debt settlement offers range from 10% to 50% of the amount you owe. Creditors are under no obligation to accept an offer and reduce your debt, even if you are working with a reputable debt settlement company.

Can debt collectors see your bank account balance? A judgment creditor cannot see your online account balances. But a creditor can ascertain account balances using post-judgment discovery. The judgment creditor can subpoena a bank for bank statements or other records which reveal a typical balance in the account.

?Offering 25%-50% of the total debt as a lump sum payment may be acceptable. The actual percentage may vary depending on the circumstances of the borrower as well as the prevailing practices of that particular collection agency.? One benefit of negotiating settlement terms is likely to reduce stress.

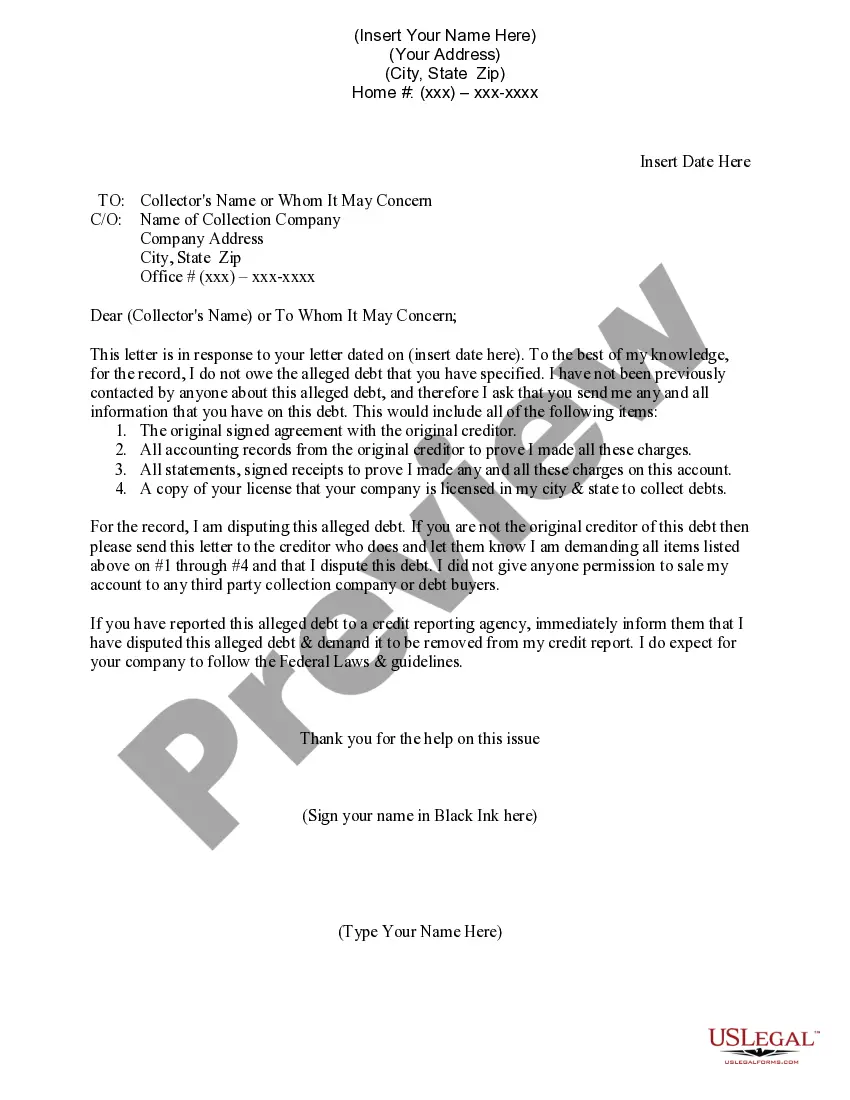

A creditor is a someone to whom you owe a debt. If someone owes you money, you are a creditor of that person. If you can't pay a debt when it's due, the creditor may try to collect the debt by sending you a demand for payment, or the creditor may assign the debt to a debt collection agency.

Although the average settlement amounts to 48% of what you originally owed, that number is a bit skewed. If your debts are still with the original creditor, settlement amounts tend to be much higher. You can end up paying up to 80% of what you owe if the debt is still with the original creditor.

While one agency may accept one-third of what you owe, another one may require 75% of your full debt amount. Before you suggest a lump-sum amount, determine the maximum amount you can afford and don't budge. Start with a low offer, such as 25% of the debt you owe, and work toward a middle ground.

Some want 75%?80% of what you owe. Others will take 50%, while others might settle for one-third or less. If you can afford it, proposing a lump-sum settlement is generally the best option?and the one most collectors will readily agree to.