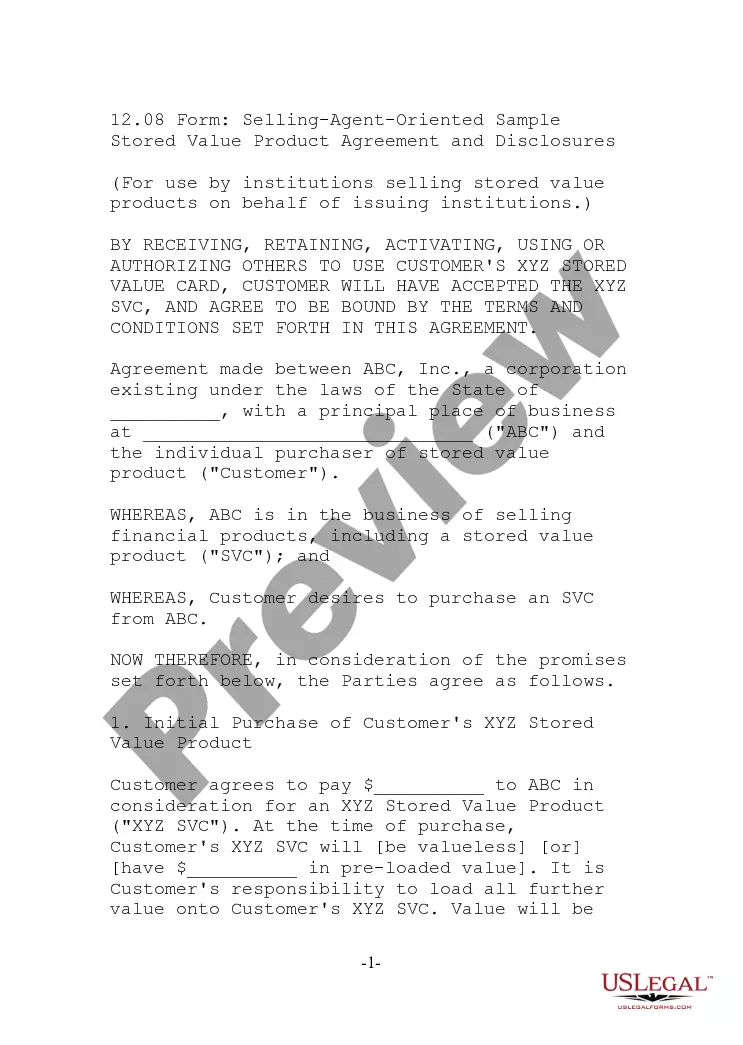

Guam Issuer - Underwriter - Oriented Sample Stored Value Product Agreement and Disclosures

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Issuer - Underwriter - Oriented Sample Stored Value Product Agreement And Disclosures?

Discovering the right lawful document web template can be quite a have difficulties. Naturally, there are tons of templates accessible on the Internet, but how do you obtain the lawful type you require? Utilize the US Legal Forms website. The support gives a large number of templates, such as the Guam Issuer - Underwriter - Oriented Sample Stored Value Product Agreement and Disclosures, that you can use for enterprise and personal needs. Every one of the forms are checked out by experts and meet up with federal and state needs.

If you are currently registered, log in in your profile and click the Download button to have the Guam Issuer - Underwriter - Oriented Sample Stored Value Product Agreement and Disclosures. Make use of profile to search with the lawful forms you have bought previously. Check out the My Forms tab of your own profile and have yet another duplicate of the document you require.

If you are a whole new end user of US Legal Forms, listed below are simple instructions that you can comply with:

- Initial, ensure you have selected the appropriate type for the metropolis/area. It is possible to look over the form making use of the Review button and study the form outline to make certain it will be the right one for you.

- When the type fails to meet up with your expectations, take advantage of the Seach area to get the appropriate type.

- When you are sure that the form is proper, click the Buy now button to have the type.

- Select the pricing plan you want and enter in the needed information. Make your profile and buy the order with your PayPal profile or charge card.

- Choose the document structure and down load the lawful document web template in your gadget.

- Complete, modify and printing and signal the attained Guam Issuer - Underwriter - Oriented Sample Stored Value Product Agreement and Disclosures.

US Legal Forms will be the greatest catalogue of lawful forms in which you will find numerous document templates. Utilize the company to down load expertly-made documents that comply with condition needs.

Form popularity

FAQ

Topic 815 states that an entity should follow other generally accepted accounting principles (GAAP) to determine whether allocation on either a portfolio basis or an individual asset basis is appropriate for disclosure purposes.

ASC 280 requires disclosure of certain general information related to segments. This includes information about the factors used to identify reportable segments, the types of products and services from which reportable segments generate revenues, and whether operating segments have been aggregated.

Hedge accounting disclosures shall provide information about: an entity's risk management strategy and how it is applied to manage risk; how the entity's hedging activities may affect the amount, timing and uncertainty of its future cash flows; and.

The required hedge accounting disclosures apply where the entity elects to adopt hedge accounting and require information to be provided in three broad categories: (1) the entity's risk management strategy and how it is applied to manage risk (2) how the entity's hedging activities may affect the amount, timing and ...

ASC 815 "Derivatives and Hedging" provides guidance on a complex area of accounting. Derivatives are highly leveraged instruments that provide each party exposure to an economic risk without significant upfront costs. Derivatives are mainly used by entities to mitigate risk by offsetting existing financial exposures.

ASC 815-10-15-83 defines a derivative instrument. A derivative instrument is a financial instrument or other contract with all of the following characteristics: Underlying, notional amount, payment provision.

ASC 815 requires a derivative to be recorded on the balance sheet as an asset or liability and to be measured at fair value. Changes in fair value each period are reported in earnings, unless the derivative is designated in a qualifying hedge relationship.

Following are the items that an entreprise must disclose for each reportable segment: Segment revenue. Segment result. Total carrying amount of segment assets. Total amount of segment liabilities. Cost incurred in a given period to acquire segment assets expected to be used during more than one period.