Guam Notice of Adverse Action - Non-Employment - Due to Credit Report

Description

How to fill out Notice Of Adverse Action - Non-Employment - Due To Credit Report?

Locating the appropriate sanctioned document template can be challenging.

Of course, there is an array of formats accessible online, but how can you locate the sanctioned version you require.

Utilize the US Legal Forms website. This service provides thousands of templates, such as the Guam Notice of Adverse Action - Non-Employment - Due to Credit Report, suitable for both business and personal needs.

You can preview the document using the Preview button and review the document outline to confirm it is the right one for you.

- All templates are reviewed by experts and comply with federal and state regulations.

- If you are already registered, Log In to your account and click the Download button to access the Guam Notice of Adverse Action - Non-Employment - Due to Credit Report.

- Utilize your account to browse through the legal templates you have previously purchased.

- Visit the My documents section of your account to download another copy of the document you need.

- If you are a new user of US Legal Forms, here are simple steps for you to follow.

- First, ensure that you have selected the correct template for your location/state.

Form popularity

FAQ

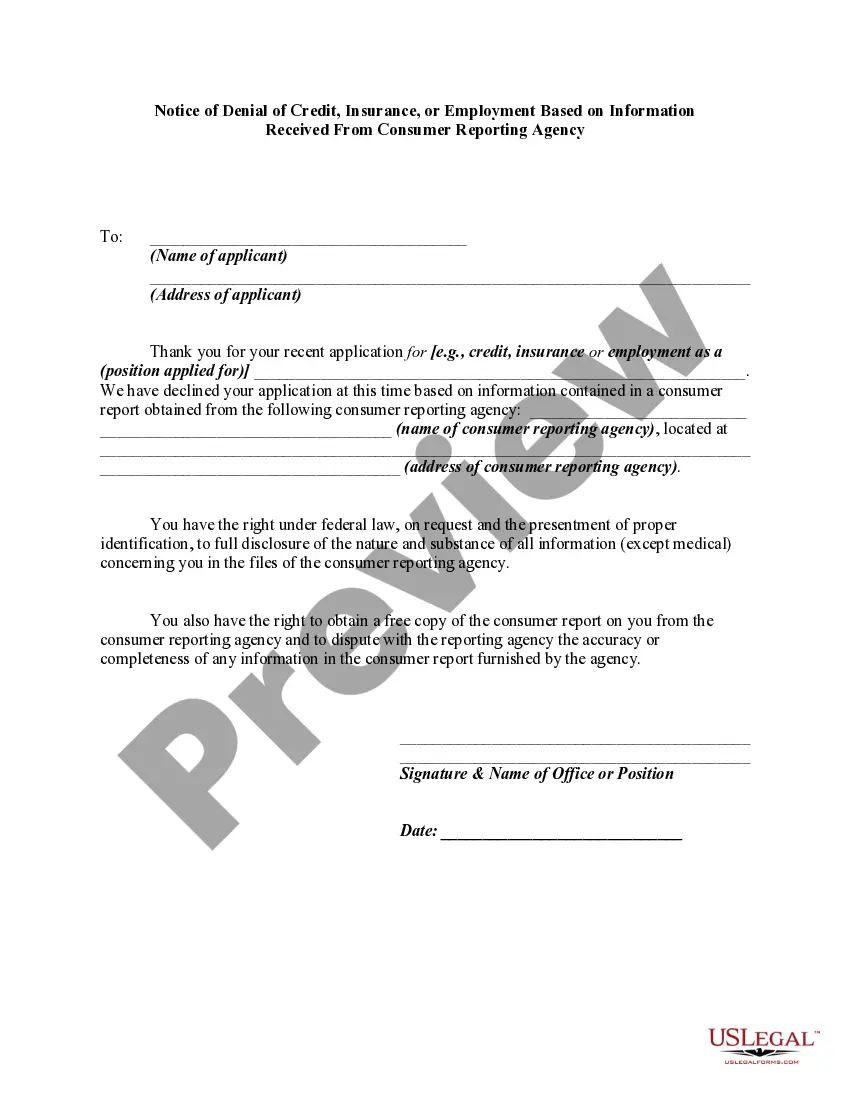

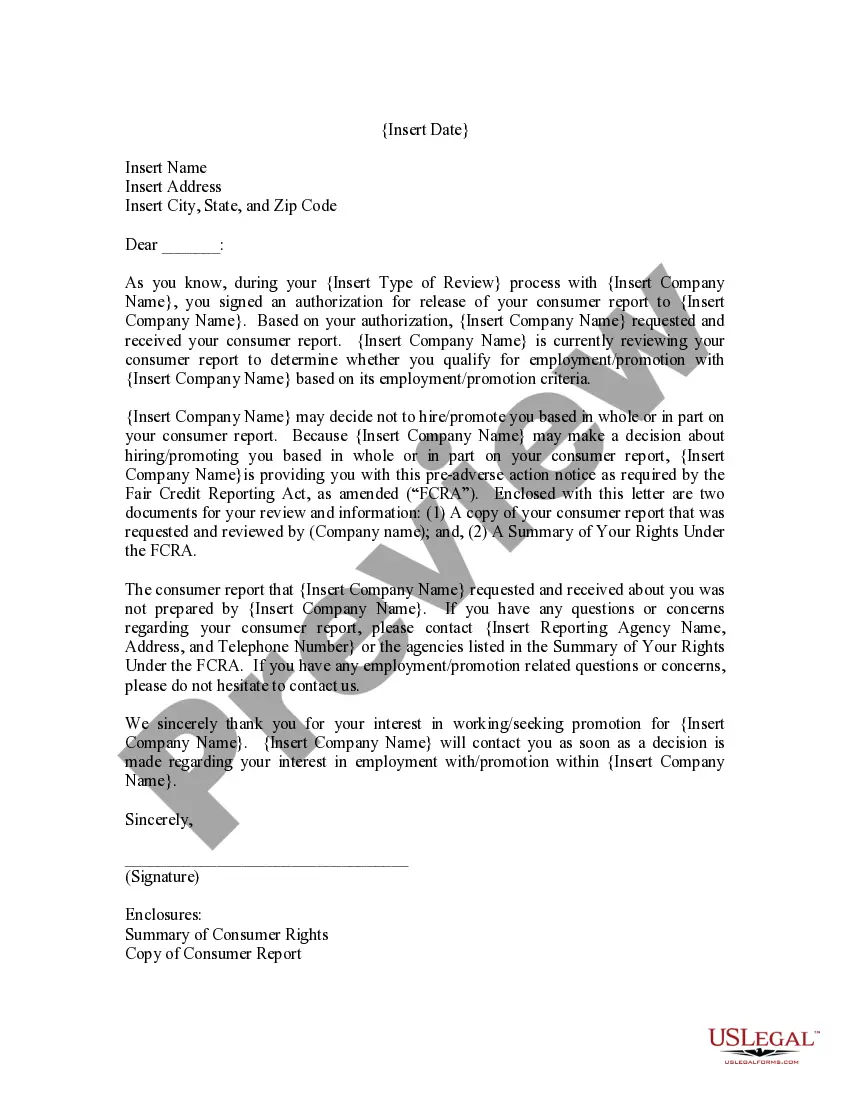

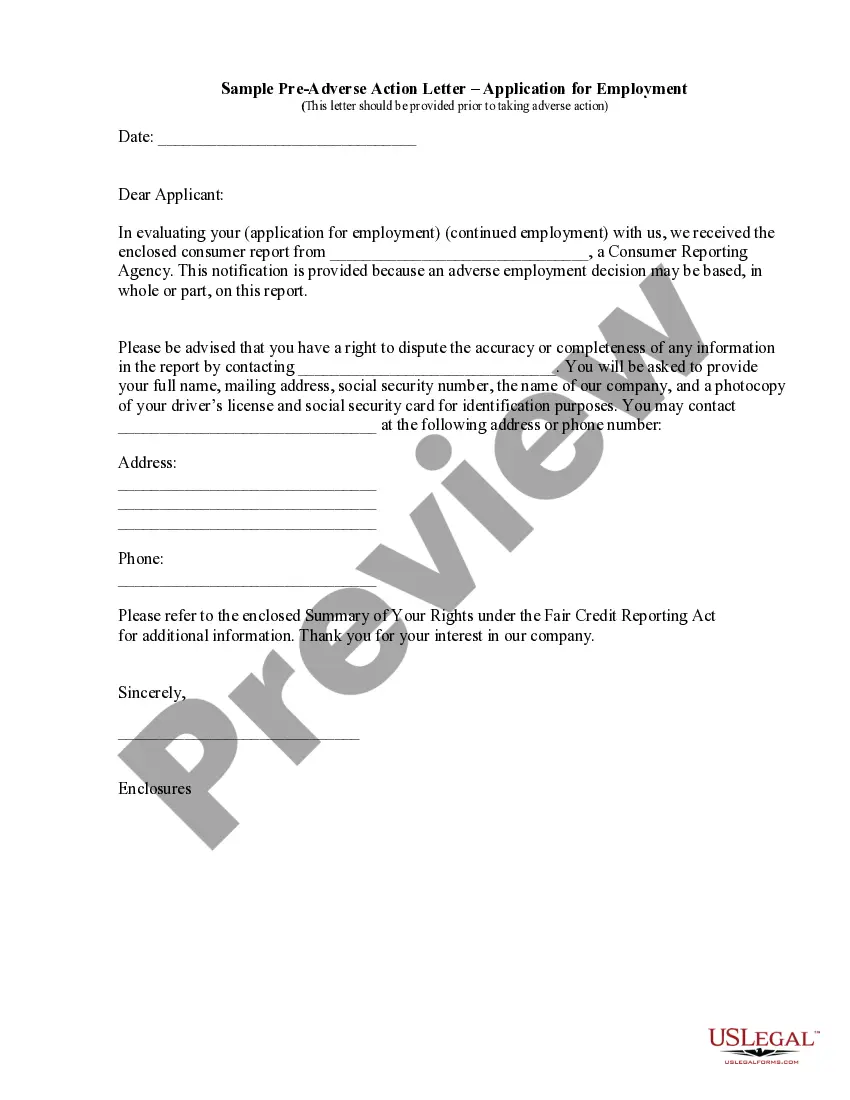

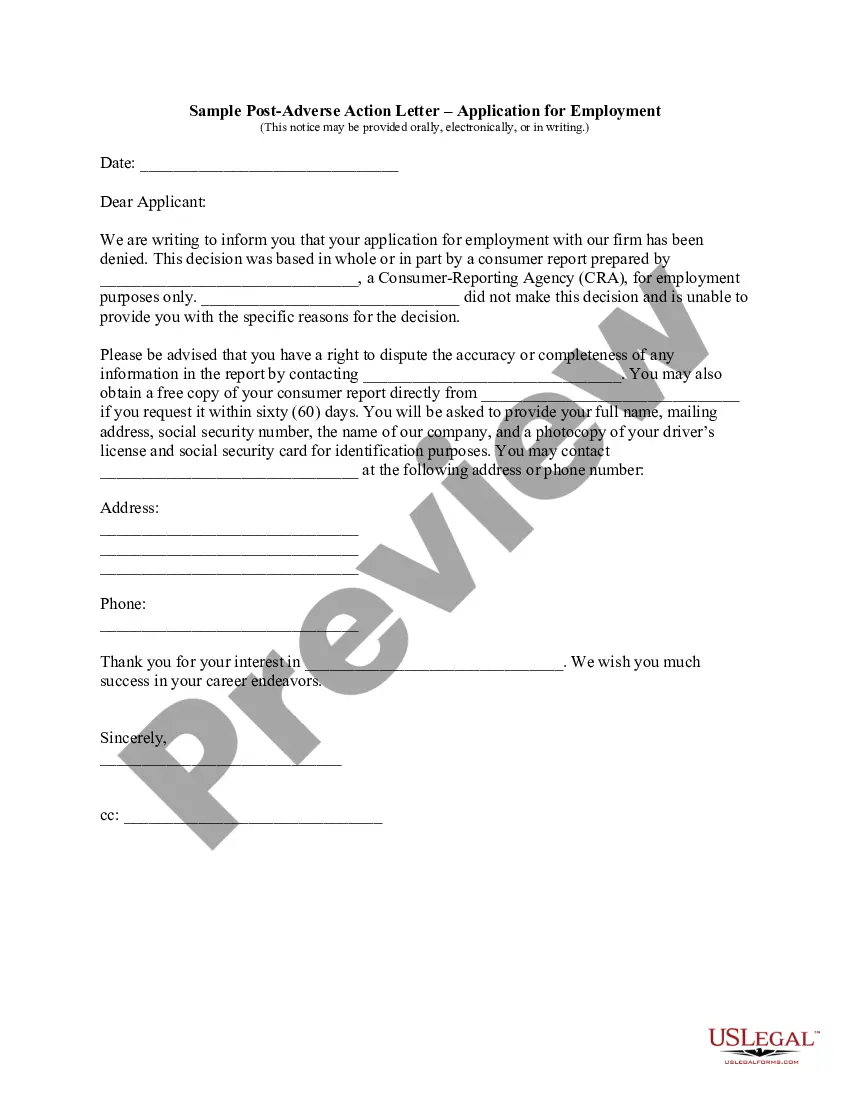

An adverse action notice is an explanation that issuers must give you if you're denied credit or if you're given less favorable financing terms based on your credit history. You may also get an adverse action notice if your credit is a reason an employer turns you down for a job.

It must include information about the credit bureau used, an explanation of the specific reasons for the adverse action, a notice of the consumer's right to a free credit report and to dispute its accuracy and the consumer's credit score.

An adverse action notice is to inform you that you have been denied credit, employment, insurance, or other benefits based on information in a credit report. The notice should indicate which credit reporting agency was used, and how to contact them.

Continue with the hire or take adverse action Taking adverse action is regrettable for both the organization and the candidate, but eventually you'll need to decide to rescind your job offer or proceed with hiring.

A creditor must disclose a consumer's credit score and information relating to a credit score on a risk-based pricing notice when the score of the consumer to whom the creditor extends credit or whose extension of credit is under review is used in setting the material terms of credit.

An adverse action notice will not hurt your credit score or show up on your credit report. However, if the creditor pulls a hard credit inquiry, this may temporarily lower your scoreand all hard inquiries remain on your credit report for two years.

A creditor must notify the applicant of adverse action within: 30 days after receiving a complete credit application. 30 days after receiving an incomplete credit application. 30 days after taking action on an existing credit account.

In the credit score exception notices, creditors are required to disclose the distribution of credit scores among consumers who are scored under the same scoring model that is used to generate the consumer's credit score using the same scale as that of the credit score provided to the consumer.

It must include information about the credit bureau used, an explanation of the specific reasons for the adverse action, a notice of the consumer's right to a free credit report and to dispute its accuracy and the consumer's credit score.