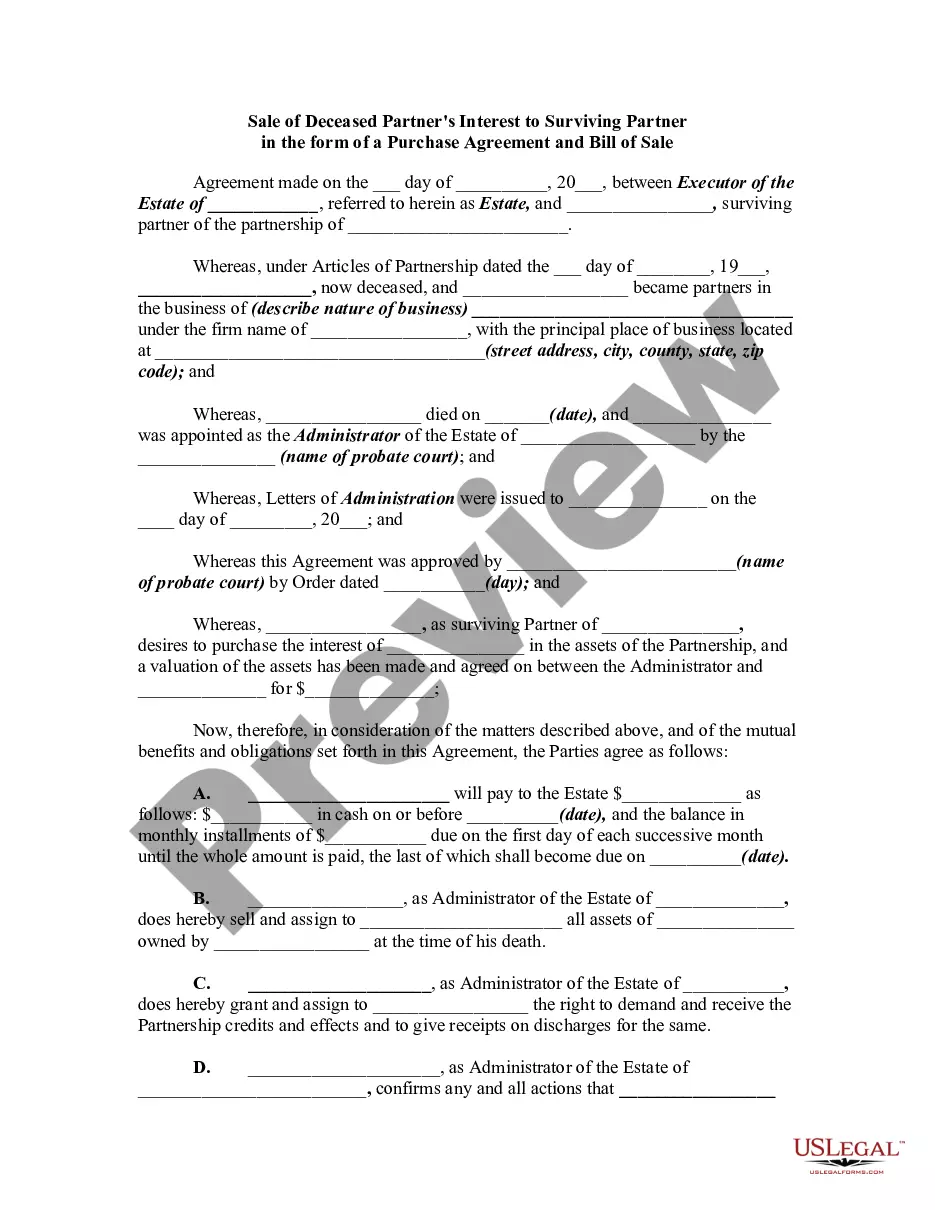

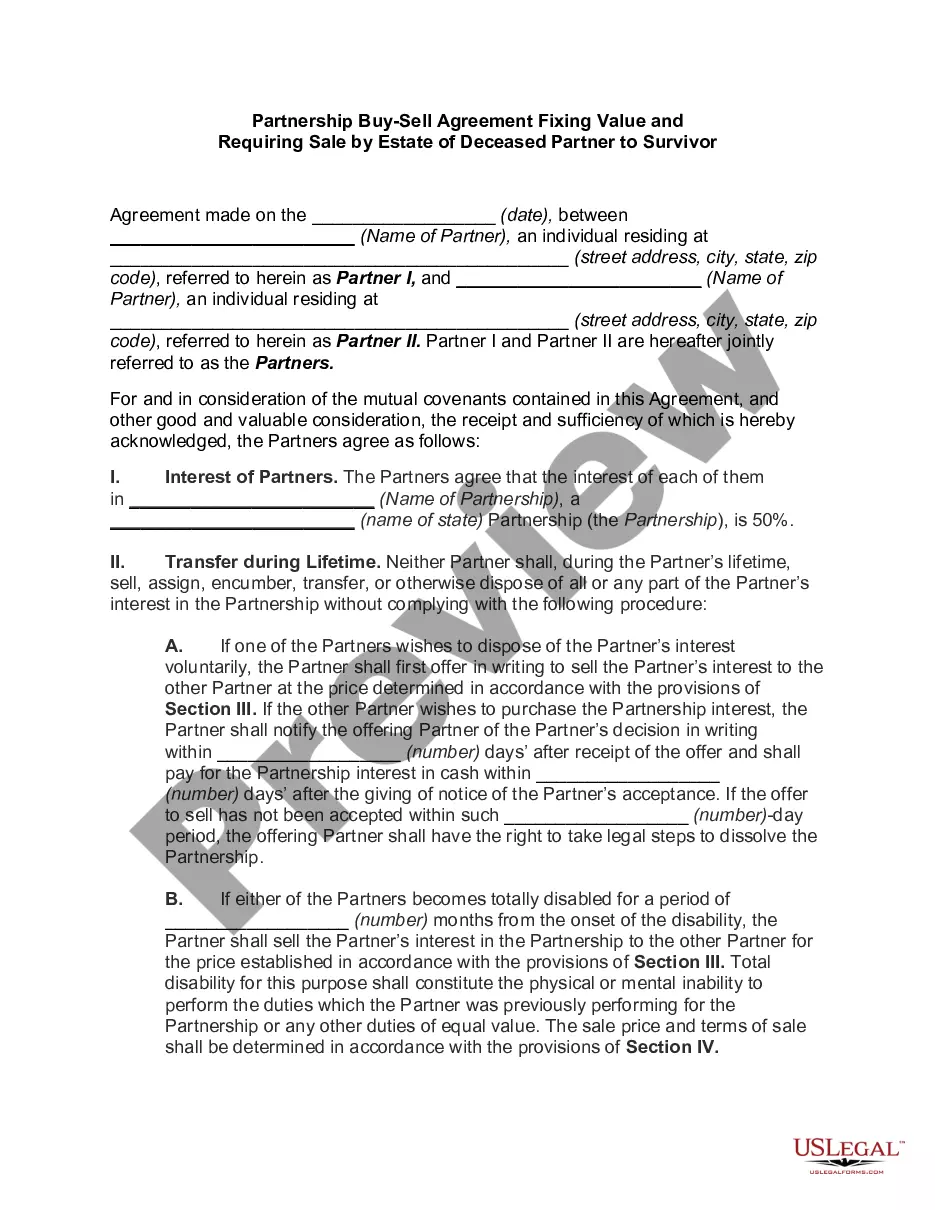

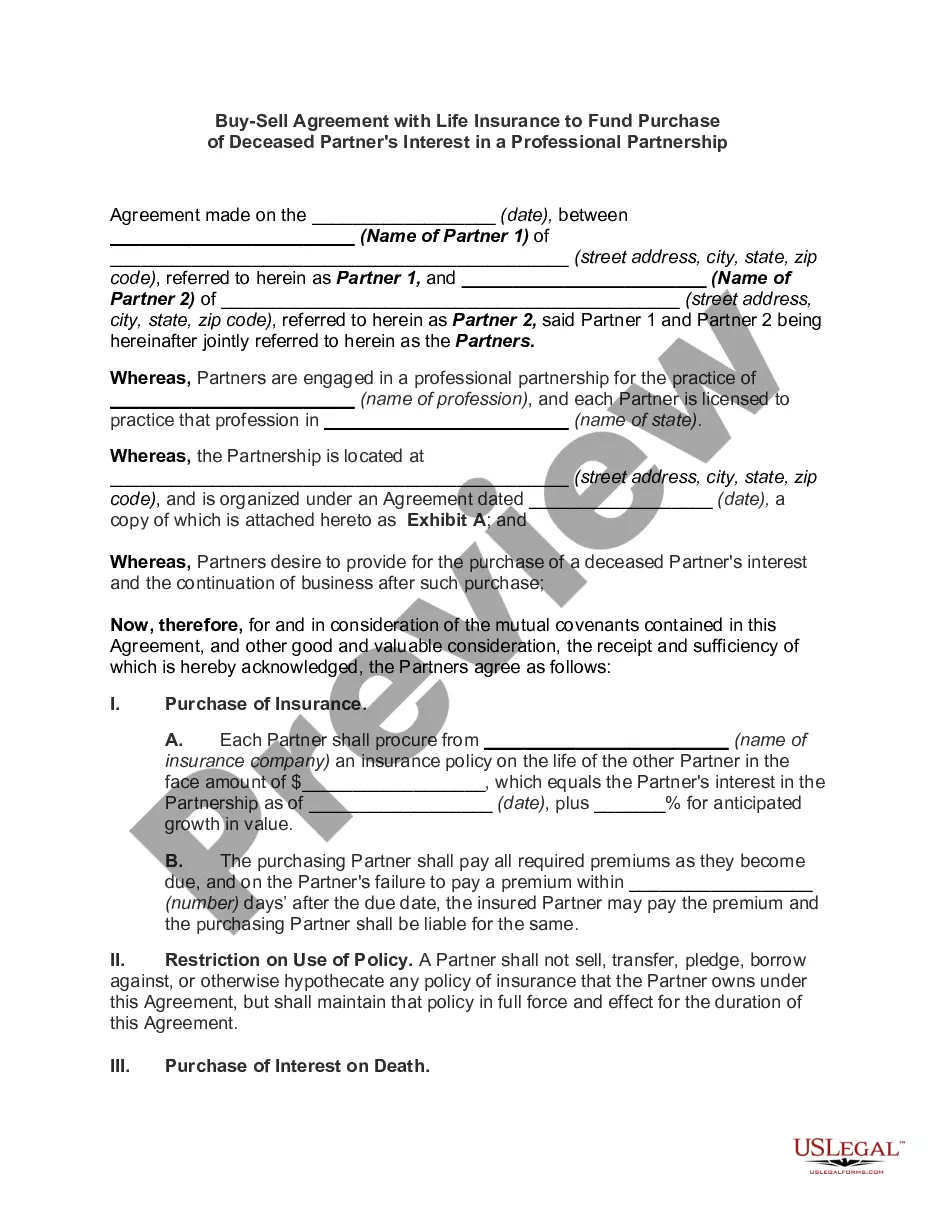

The purpose of this Agreement is to provide for the continuance of the partnership business on the death or retirement of a partner and the purchase of his or her interest in the partnership by the partnership.

Guam Sale of Deceased Partner's Interest

Instant download

Description

Free preview

How to fill out Sale Of Deceased Partner's Interest?

You have the ability to invest hours online searching for the authentic document template that fulfills the federal and state requirements you need.

US Legal Forms provides thousands of authentic forms that are verified by experts.

You can download or print the Guam Sale of Deceased Partner's Interest from our platform.

If you wish to find another version of the template, use the Search section to locate the template that meets your needs and specifications. Once you have identified the template you require, click Buy now to proceed. Choose the pricing plan you need, enter your credentials, and register for your account on US Legal Forms. Complete the transaction. You may use your credit card or PayPal account to pay for the authentic form. Choose the format of the document and download it to your device. Make adjustments to the document if needed. You can complete, edit, and sign the Guam Sale of Deceased Partner's Interest. Download and print thousands of document templates using the US Legal Forms website, which offers the largest collection of authentic forms. Utilize professional and state-specific templates to meet your business or personal needs.

- If you currently hold a US Legal Forms account, you can Log In and click on the Download button.

- Then, you can complete, modify, print, or sign the Guam Sale of Deceased Partner's Interest.

- Every authentic document template you acquire is yours forever.

- To obtain another copy of the purchased form, visit the My documents tab and click on the relevant button.

- If you are using the US Legal Forms website for the first time, follow the simple instructions outlined below.

- First, ensure that you have selected the correct document template for the state/city of your choice.

- View the form description to confirm you have chosen the right template.

- If available, utilize the Preview button to check through the document template as well.

Form popularity

FAQ

As soon as the person dies, the account becomes property of the decedent's estate. As a result, any interest earned after the decedent's death must be included in the estate tax return. However, if the estate pays that interest out to the beneficiary, the beneficiary includes that interest on his income tax return.

person partnership does not terminate upon a partner's death if the deceased partner's successor in interest (usually the estate) continues to share in the partnership's profits or losses (Regs. Sec. 1. 7081(b)(1)(I)).

2012 Review Schedule D, Form 8949 and Form 4797 to determine the amount of gain or loss the partner reported on the sale of the partnership interest. After determining a partner sold its interest in the partnership, establish other relevant facts that can impact the tax treatment of this transaction.

Partnerships file Form 8308 to report the sale or exchange by a partner of all or part of a partnership interest where any money or other property received in exchange for the interest is attributable to unrealized receivables or inventory items (that is, where there has been a section 751(a) exchange).

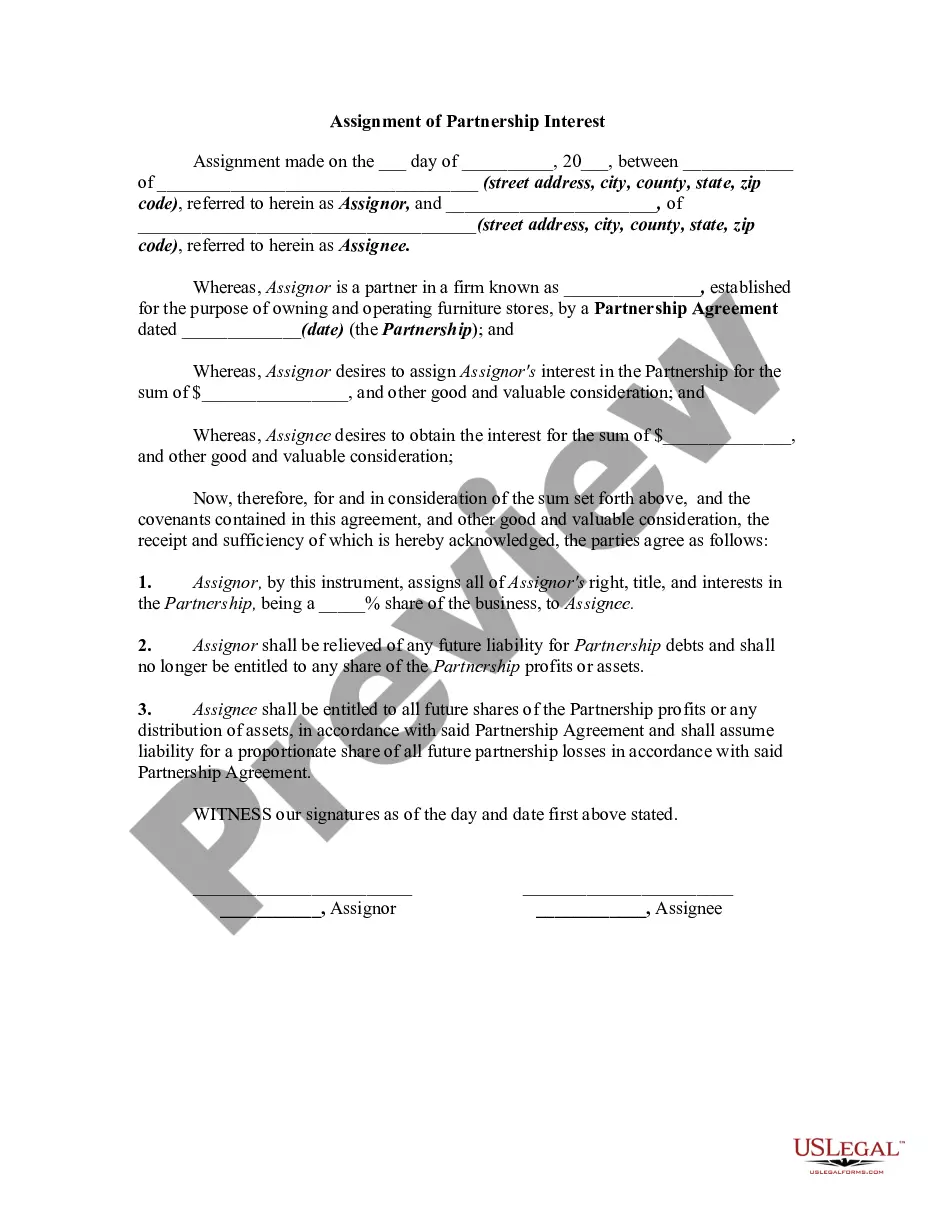

A partner may acquire an interest in a partnership in a variety of ways. For example, the partner may purchase his interest from an existing partner. Like any other asset, a partnership interest may be acquired through a gift or an inheritance.

The sale of a partnership interest is generally treated as a sale of a capital asset, resulting in capital gain or loss for the selling partner.

The death of a partner in a two-person partnership will terminate the partnership for federal tax purposes if it results in the partnership's immediately winding up its business (Sec. 708(b)(1)(A)). If this occurs, the partnership's tax year closes on the partner's date of death.

Most legislation states that the partnership will end upon the death or bankruptcy of any partner. If your partner dies, you will then owe your partner's estate their share of the partnership that accrues at the date of their death.

How to Report a Sale of a Share of a Partnership on a 1065Complete Part I and Part II, Items E through I, on each partner's K-1. This is used to provide personal information.Complete Part III of each partner's K-1.Complete the selling partner's K-1.Complete the remaining partners' K-1s.