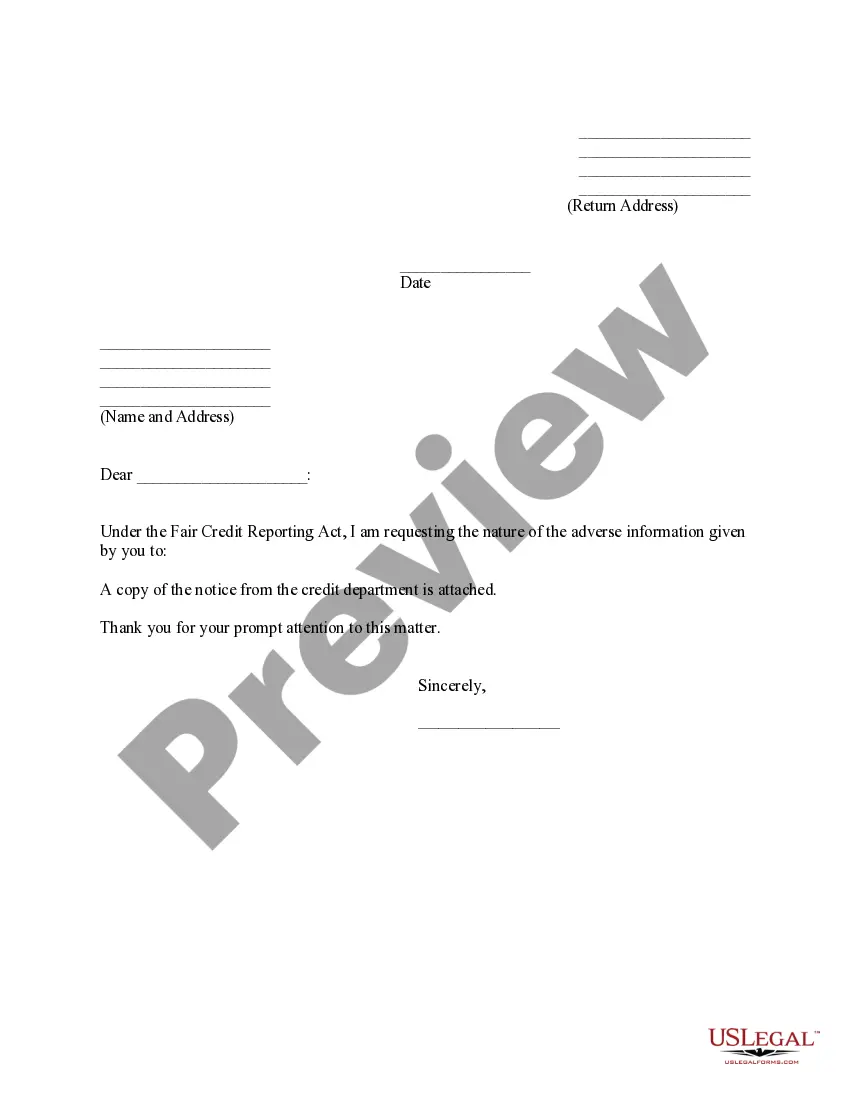

Georgia Credit Information Request

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Credit Information Request?

Are you currently in a circumstance where you require documents for either business or personal purposes nearly every day.

There are numerous legitimate document templates accessible online, but finding ones you can trust is challenging.

US Legal Forms provides thousands of template options, such as the Georgia Credit Information Request, which can be tailored to fulfill state and federal requirements.

Utilize US Legal Forms, the most extensive collection of legitimate templates, to save time and avoid mistakes.

This service provides expertly crafted legal document templates that can be used for various purposes. Create an account on US Legal Forms and start making your life easier.

- If you are already familiar with the US Legal Forms website and have an account, simply Log In.

- Then, you can download the Georgia Credit Information Request template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Find the template you need and ensure it is for the correct area/state.

- Use the Preview button to review the document.

- Read the description to ensure you have selected the correct template.

- If the template is not what you are looking for, utilize the Search section to find a template that meets your needs and specifications.

- Once you find the appropriate template, click Purchase now.

- Select the pricing plan you prefer, fill in the required details to create your account, and pay for the order using PayPal or your credit card.

- Choose a convenient document format and download your copy.

- Access all the document templates you have purchased in the My documents menu. You can obtain another copy of the Georgia Credit Information Request at any time if needed. Just select the required template to download or print the document.

Form popularity

FAQ

The Consumer Credit Act and the General Data Protection Regulation (GDPR) gives you the right to request a one-off statutory credit file from TransUnion. Your statutory credit file gives you the details about your credit accounts, missed payments and the people with whom you have financial links.

The Consumer Credit Act and the General Data Protection Regulation (GDPR) gives you the right to request a one-off statutory credit file from TransUnion. Your statutory credit file gives you the details about your credit accounts, missed payments and the people with whom you have financial links.

A Consumer Disclosure is a complete account of all the information on your credit file as mandated by consumer reporting legislation. A Consumer Disclosure does not include your TransUnion Credit Score.

Not everything in your credit file ends up on your credit report. Records of most late debt payments, for instance, shouldn't appear on your credit report if they're more than 7 years old. Your credit report is used to generate your credit scores and may be viewed by lenders to assess your creditworthiness.

This information is reported to Equifax by your lenders and creditors and includes the types of accounts (for example, a credit card, mortgage, student loan, or vehicle loan), the date those accounts were opened, your credit limit or loan amount, account balances, and your payment history.

In short, this is a disclosures that includes things like the credit score of the applicant, the range of possible scores, key factors that adversely affected the credit score, the date of the score, and the name of the person or entity that provided the score.

The credit score exception notice (model forms H-3, H-4, H-5) is a disclosure that is provided in lieu of the risk-based-pricing notice (RBPN, which are H-1, H-2, H-6 & H-7). The RBPN is required any time a financial institution provides different rates based on the credit score of the applicant.

Credit reports list your bill payment history, loans, current debt, and other financial information.

A creditor must disclose a consumer's credit score and information relating to a credit score on a risk-based pricing notice when the score of the consumer to whom the creditor extends credit or whose extension of credit is under review is used in setting the material terms of credit.

A credit inquiry is a request by an institution for credit report information from a credit reporting agency. Credit inquiries can be from all types of entities for various reasons, but they are typically made by financial institutions. They are classified as either a hard inquiry or a soft inquiry.