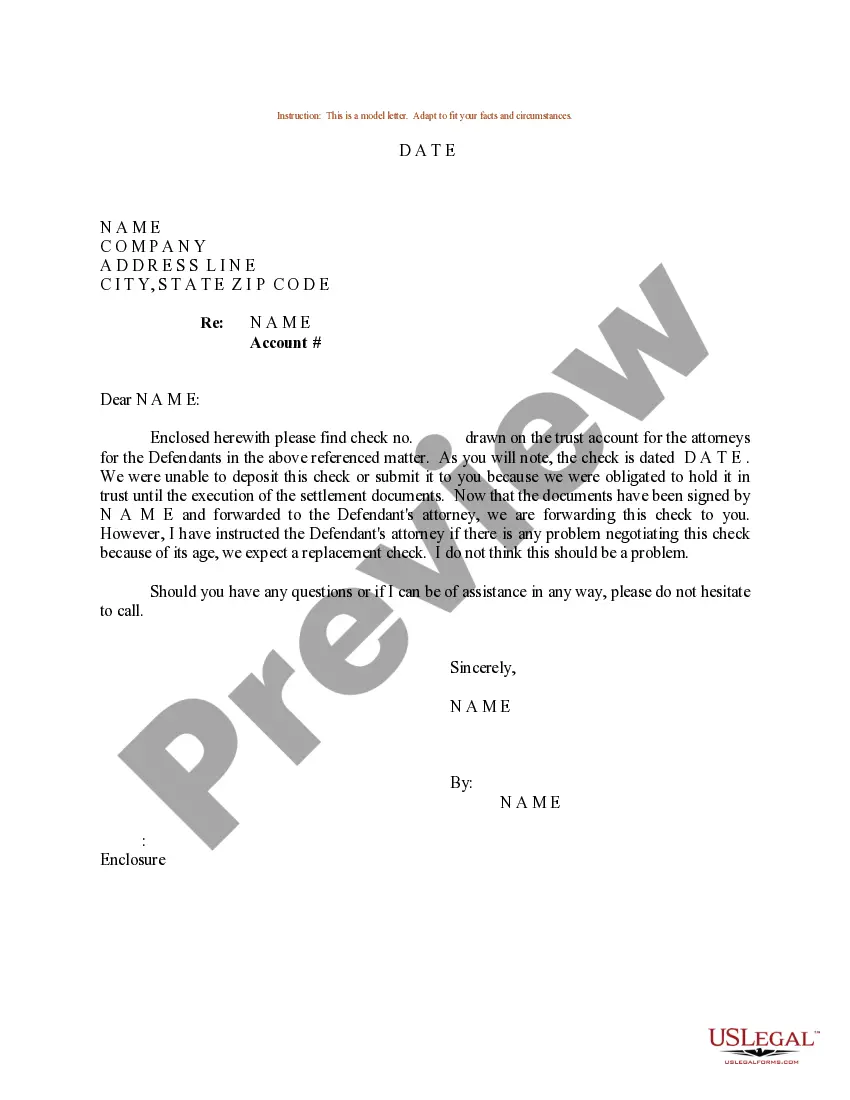

Georgia Sample Letter concerning Stop Payment Notice

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Sample Letter Concerning Stop Payment Notice?

Are you currently in a situation where you need documents for either business or personal reasons every day.

There are numerous legal document templates available online, but finding ones you can trust is not simple.

US Legal Forms offers thousands of form templates, such as the Georgia Sample Letter regarding Stop Payment Notice, which are designed to meet federal and state regulations.

Access all the document templates you have purchased in the My documents section. You can download another copy of the Georgia Sample Letter regarding Stop Payment Notice at any time, if needed. Just click on the desired form to download or print the document template.

Utilize US Legal Forms, the largest collection of legal forms, to save time and avoid mistakes. The service provides professionally crafted legal document templates that can be used for various purposes. Create your account on US Legal Forms and start making your life a bit easier.

- If you are already familiar with the US Legal Forms website and have your account, simply Log In.

- Then, you can download the Georgia Sample Letter regarding Stop Payment Notice template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Obtain the form you need and ensure it is for the correct city/area.

- Use the Preview feature to review the form.

- Check the description to confirm that you have selected the right form.

- If the form does not match what you seek, utilize the Search field to find the form that meets your needs and requirements.

- Once you find the right form, click Get now.

- Choose the subscription plan you prefer, fill in the required information to create your account, and complete the transaction using your PayPal or credit card.

- Select a convenient file format and download your copy.

Form popularity

FAQ

To stop the next scheduled payment, give your bank the stop payment order at least three business days before the payment is scheduled. You can give the order in person, over the phone or in writing. To stop all future payments, you might have to send your bank the stop payment order in writing.

To stop payment on a check, go to a bank branch or contact the bank by phone and speak to a human being, not a recording. Request a Stop Payment Order. Make sure to report the check number, the amount, the recipient's name, and the date on the check.

Your dated stop payment letter should include details like: the name and address of the account owner, the bank or credit union's address, the account number, check number, date, amount, the signer, and the payee; an explanation for the stop payment order (e.g., the check is presumed lost, it's not authorized, or ...

You can contact your bank and place a stop payment order on the recurring transaction. Generally, a stop payment order is only good for six months. To stop payment, you will need to notify your bank at least three business days before the next payment is scheduled to be made. Notice may be made orally or in writing.

To stop payment, you need to notify your bank at least three business days before the transaction is scheduled to be made and your bank may charge a fee. The notice to stop the transaction may be made orally or in writing. A bank can require written confirmation of an oral stop payment request.

When issuing a stop payment order to a bank, an account holder can call the financial institution to ask for a stop payment to be issued immediately, with a promise to visit the bank and issue a written order.

To withdraw consent, simply tell whoever issued your card (the bank, building society or credit card company) that you don't want the payment to be made. You can tell the card issuer by phone, email or letter. Your card issuer has no right to insist that you ask the company taking the payment first.