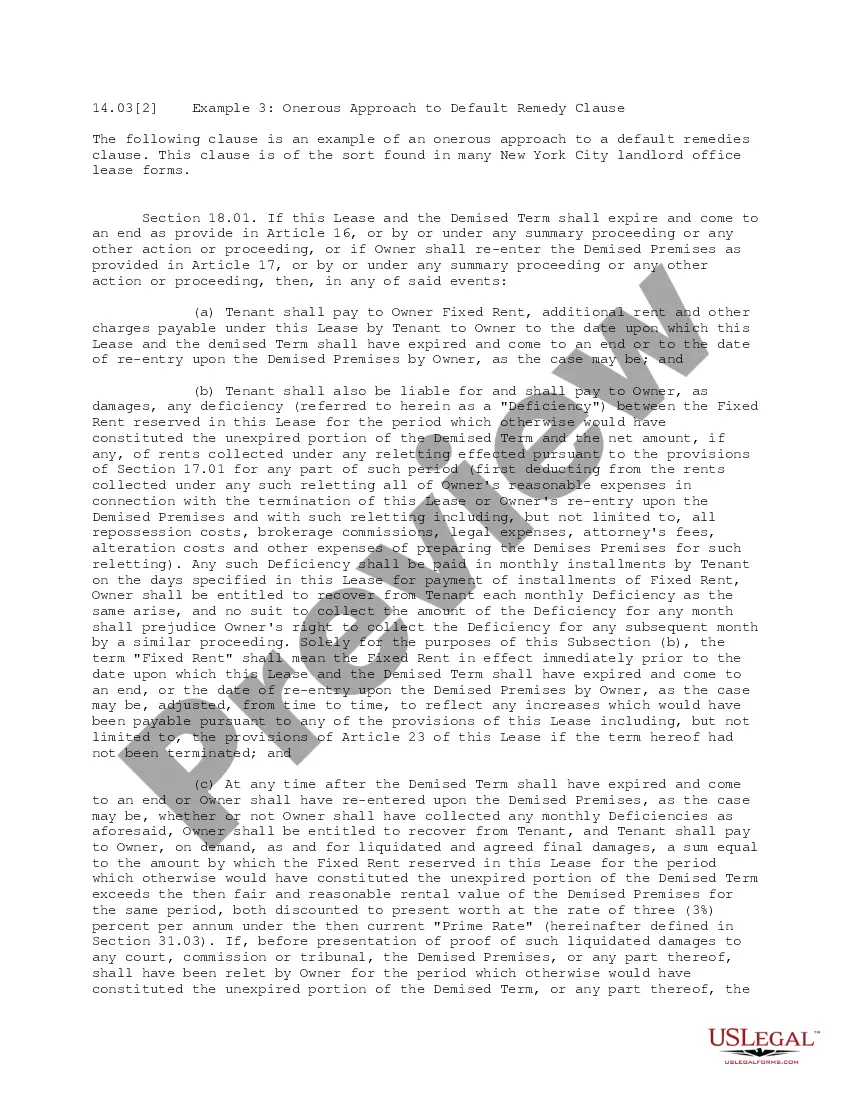

This office lease form is a standard default remedy clause, providing for the collection of the difference between the rent due and owing under the lease and the rents collected in the event of mitigation.

Florida Default Remedy Clause

Category:

State:

Multi-State

Control #:

US-OL14031

Format:

Word;

PDF

Instant download

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Default Remedy Clause?

You can commit hrs on-line attempting to find the lawful papers web template that fits the state and federal needs you need. US Legal Forms supplies thousands of lawful forms that happen to be examined by professionals. It is possible to acquire or produce the Florida Default Remedy Clause from the support.

If you have a US Legal Forms bank account, you are able to log in and click on the Obtain switch. Afterward, you are able to comprehensive, edit, produce, or signal the Florida Default Remedy Clause. Each lawful papers web template you buy is your own eternally. To have another duplicate associated with a obtained form, proceed to the My Forms tab and click on the corresponding switch.

If you use the US Legal Forms internet site the first time, adhere to the easy guidelines beneath:

- First, be sure that you have chosen the correct papers web template for that state/town of your choice. See the form information to ensure you have selected the proper form. If accessible, use the Review switch to look throughout the papers web template too.

- In order to find another edition of your form, use the Look for field to discover the web template that suits you and needs.

- Once you have discovered the web template you would like, just click Acquire now to carry on.

- Choose the rates prepare you would like, type in your credentials, and register for an account on US Legal Forms.

- Comprehensive the purchase. You can use your credit card or PayPal bank account to purchase the lawful form.

- Choose the file format of your papers and acquire it for your system.

- Make changes for your papers if necessary. You can comprehensive, edit and signal and produce Florida Default Remedy Clause.

Obtain and produce thousands of papers web templates while using US Legal Forms website, which offers the most important assortment of lawful forms. Use expert and condition-distinct web templates to deal with your small business or specific requires.

Form popularity

FAQ

An example of a legal remedy in contract law is compensatory damages. Compensatory damages are intended to compensate the non-breaching party for their actual losses. This may include damages for lost wages, medical bills, or property damage. Compensatory damages may also include emotional distress damages.

This provision specifies the remedies for an Event of Default and also outlines the order in which available funds will be disbursed to the lenders. all outstanding borrowings become immediately due and payable. all outstanding borrowings become immediately due and payable.

There are several remedies for breach of contract, such as award of damages, specific performance, rescission, andrestitution. In courts of limited jurisdiction, the main remedy is an award of damages.

What does Remedy mean? The means by which a court enforces a right or orders redress for a wrong. It can include damages (whether compensatory or restitutionary), injunctive relief (whether interim or final) and specific performance (of outstanding obligations).

The Company acknowledges that monetary damages would not be adequate compensation for any loss incurred by reason of a breach by it of the provisions of this Agreement and the Company hereby agrees to waive the defense in any action for specific performance that a remedy at law would be adequate.

The rights and remedies clause is categorised as one of the boilerplate clauses of an agreement. It provides that the remedies available to the parties under an agreement do not exclude any other available remedies and that any accrued rights and claims of the parties will survive termination.

A boilerplate rights and remedies clause (or cumulative remedies clause) recording that the parties to an agreement intend the rights and remedies provided under the agreement to co-exist with any other rights and remedies available to them under the general law, and not to displace them.

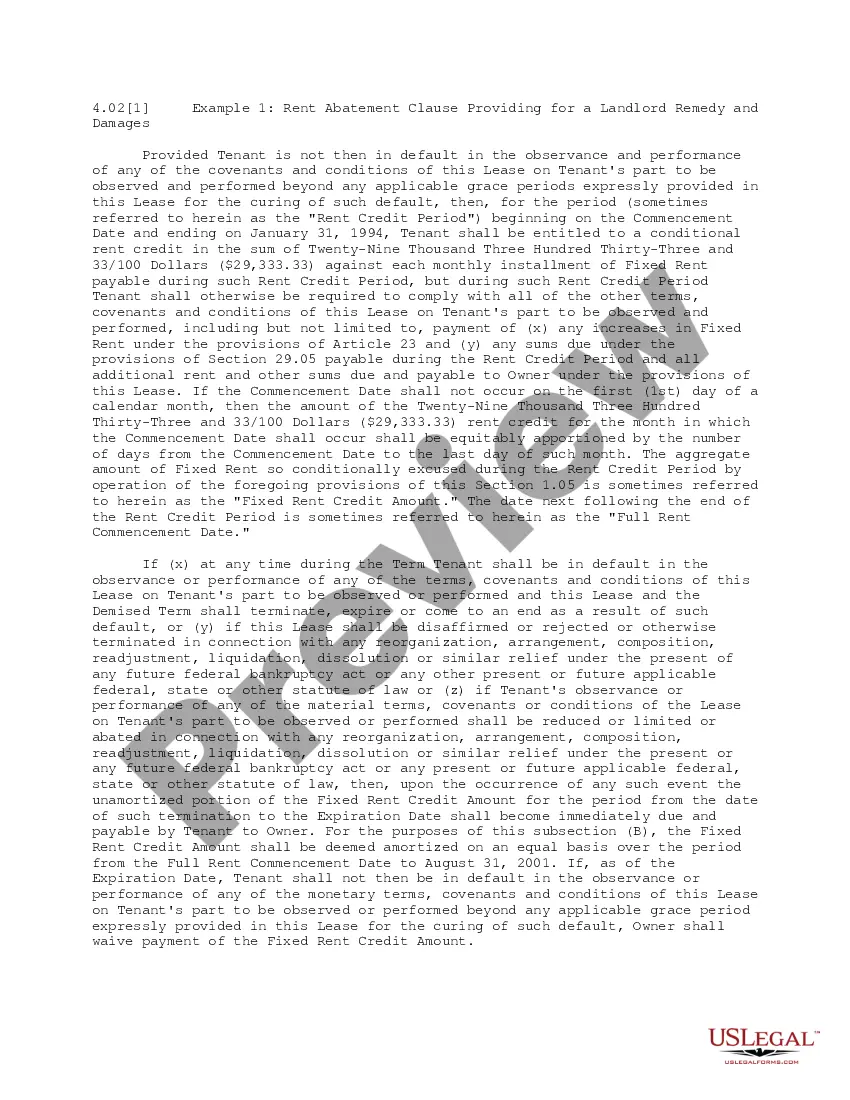

A ?default? is a failure to comply with a provision in the lease. ?Curing? or ?remedying? the default means correcting the failure or omission. A common example is a failure to pay the rent on time.