Courts vary in their approach to enforcing releases depending on the particular facts of each case, the effect of the release on other statutes and laws, and the view of the court of the benefits of releases as a matter of public policy. Many courts will invalidate documents signed on behalf of minors. Also, Courts do not permit persons to waive their responsibility when they have exercised gross negligence or misconduct that is intentional or criminal in nature. Such an agreement would be deemed to be against public policy because it would encourage dangerous and illegal behavior.

A lactation consultant is a healthcare provider recognized as having expertise in the fields of human lactation and breastfeeding

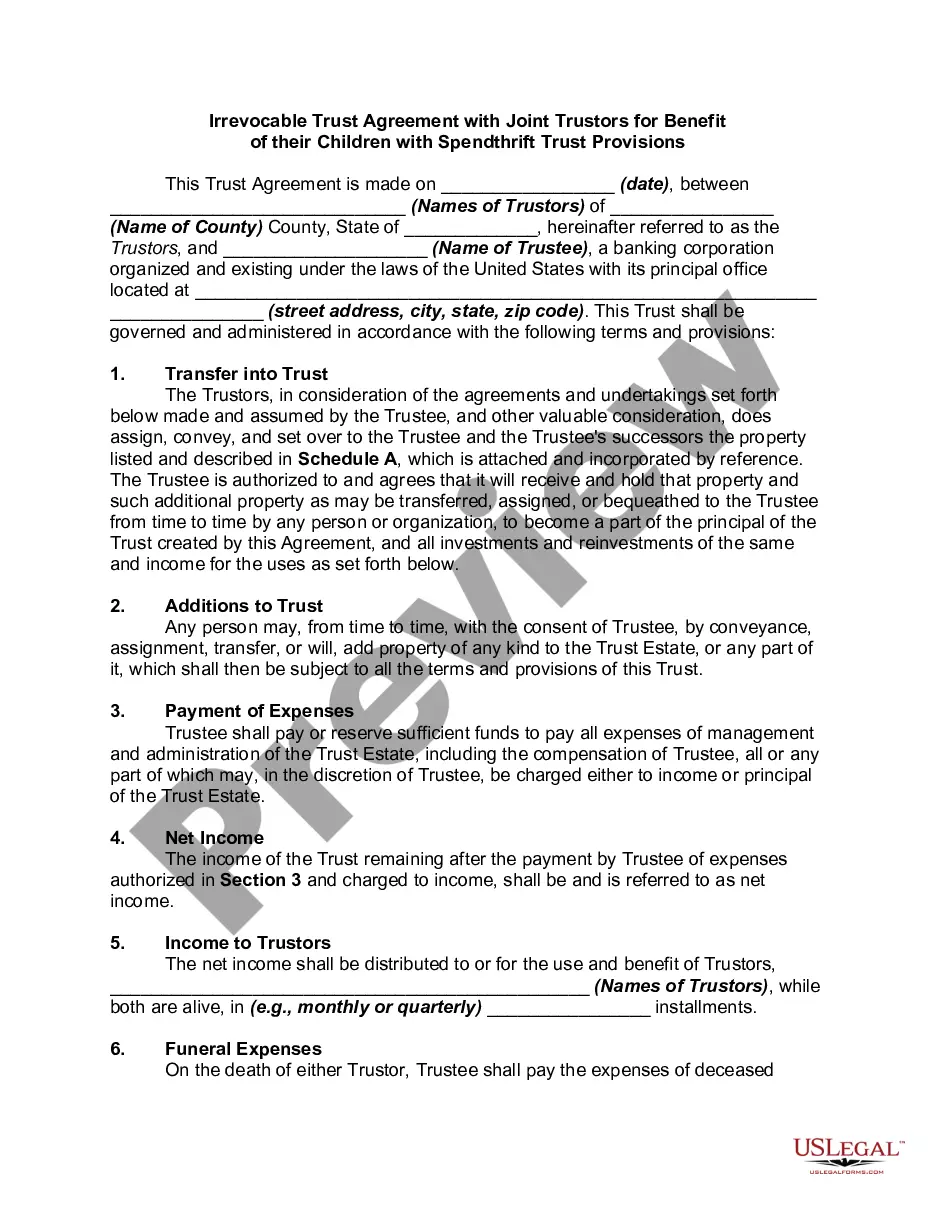

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Delaware Irrevocable Trust Agreement for the Benefit of Spouse, Children and Grandchildren

Instant download

Description

Free preview

How to fill out Irrevocable Trust Agreement For The Benefit Of Spouse, Children And Grandchildren?

If you need to finalize, obtain, or print sanctioned document templates, utilize US Legal Forms, the largest collection of legal forms available online.

Make use of the site’s simple and user-friendly search to locate the documents you need.

Various templates for commercial and individual needs are categorized by type and state, or keywords.

Step 4. Once you have located the form you require, click on the Get Now button. Select the pricing plan you prefer and enter your information to register for the account.

Step 5. Complete the transaction. You can use your credit card or PayPal account to finalize the payment.

- Employ US Legal Forms to find the Delaware Irrevocable Trust Agreement for the Benefit of Spouse, Children, and Grandchildren with just a few clicks.

- If you are already a US Legal Forms user, sign in to your account and click the Download button to obtain the Delaware Irrevocable Trust Agreement for the Benefit of Spouse, Children, and Grandchildren.

- You can also access forms you have previously saved in the My documents section of your account.

- If you are using US Legal Forms for the first time, follow the steps outlined below.

- Step 1. Ensure you have selected the form for the correct city/state.

- Step 2. Use the Preview option to review the content of the form. Be sure to read the description.

- Step 3. If you are not satisfied with the form, use the Search field at the top of the screen to find alternative types of the legal form template.

Form popularity

FAQ

An irrevocable trust is a financial arrangement where assets are transferred into a trust, and the grantor cannot alter or dissolve the trust once established. This arrangement offers benefits such as avoiding probate, minimizing estate taxes, and protecting assets for beneficiaries. When you create a Delaware Irrevocable Trust Agreement for the Benefit of Spouse, Children and Grandchildren, you secure a financial legacy for your loved ones while retaining flexibility within the structure.

For an irrevocable trust, you'll primarily need to file IRS Form 1041. This form is essential for reporting all income, deductions, and distributions associated with the trust. If you establish a Delaware Irrevocable Trust Agreement for the Benefit of Spouse, Children and Grandchildren, utilizing this form will help you accurately track the trust's financial activities.

A Trust (or Marital Trust)The surviving spouse must be the only beneficiary of the trust during his/her lifetime, however, at the time of the second spouse's death, the trust can pass to any other named beneficiaries like children, grandchildren, etc.

One of the most preferred ways to leave assets to grandchildren is by naming them as a beneficiary in your will or trust. As the grantor or trustor, you are able to specify a set amount of money or a percentage of your total accounts and property to each grandchild as you see fit.

Individual trusts for each grandchild. Most grandparents choose to put equal amounts of money into each grandchild's individual trust. The trustee can then decide when and how much money to distribute to each grandchild from their individual trust based on the standards written into the trust.

Income earned by the trust from amounts that you've deposited will not be taxed to you; the trust pays the taxes. Amounts deposited in trust, and the income earned from those funds, will be used for the benefit of your grandchildren. You can provide that the trust terminate at any age you specify.

Beneficiaries of an irrevocable trust have rights to information about the trust and to make sure the trustee is acting properly. The scope of those rights depends on the type of beneficiary. Current beneficiaries are beneficiaries who are currently entitled to income from the trust.

Often there is someone the grantor knows who the grantor suggests to be the trustee. Typical choices are the grantor's spouse, sibling, child, or friend. Any of these may be an acceptable choice from a legal perspective, but may be a poor choice for other reasons.

Irrevocable trusts can also protect assets from being used in determining Medicare eligibility. Once an irrevocable trust is funded, the trust property cannot be taken back by the grantor without the consent of the beneficiary. It is legal to name a beneficiary as trustee, such as a spouse.

An irrevocable trust is a trust that can't be amended or modified. However, like any other trust an irrevocable trust can have multiple beneficiaries. The Internal Revenue Service allows irrevocable trusts to be created as grantor, simple or complex trusts.