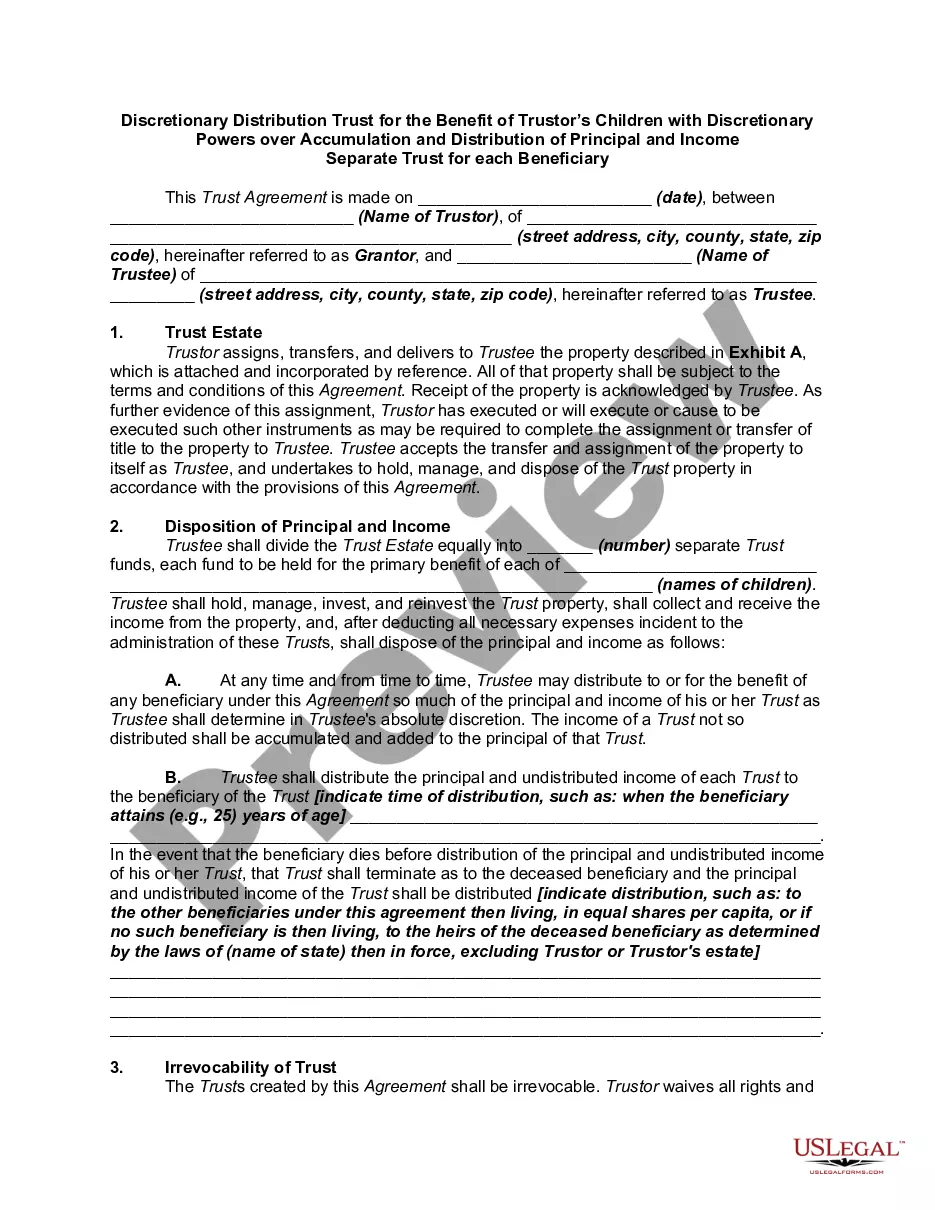

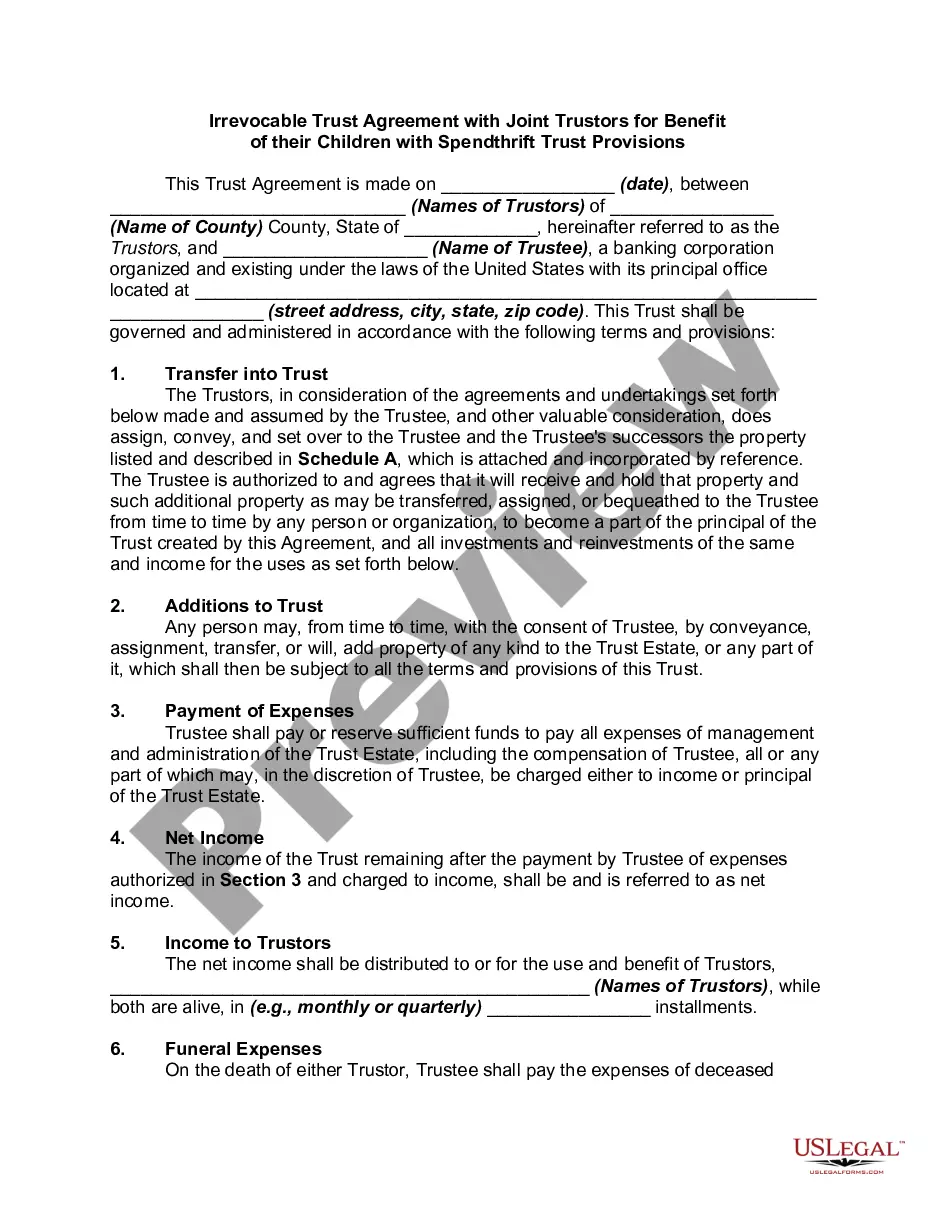

An irrevocable trust is an arrangement in which the grantor departs with ownership and control of property. Usually this involves a gift of the property to the trust. The trust then stands as a separate taxable entity and pays tax on its accumulated income.

A discretionary trust is a trust where the beneficiaries and/or their entitlements to the trust fund are not fixed, but are determined by the criteria set out in the trust instrument by trustor. Discretionary trusts can be discretionary in two respects. First, the trustees usually have the power to determine which beneficiaries (from within the class) will receive payments from the trust. Second, trustees can select the amount of trust property that the beneficiary receives. Although most discretionary trusts allow both types of discretion, either can be allowed on its own. It is permissible in most legal systems for a trust to have a fixed number of beneficiaries and for the trustees to have discretion as to how much each beneficiary receives.