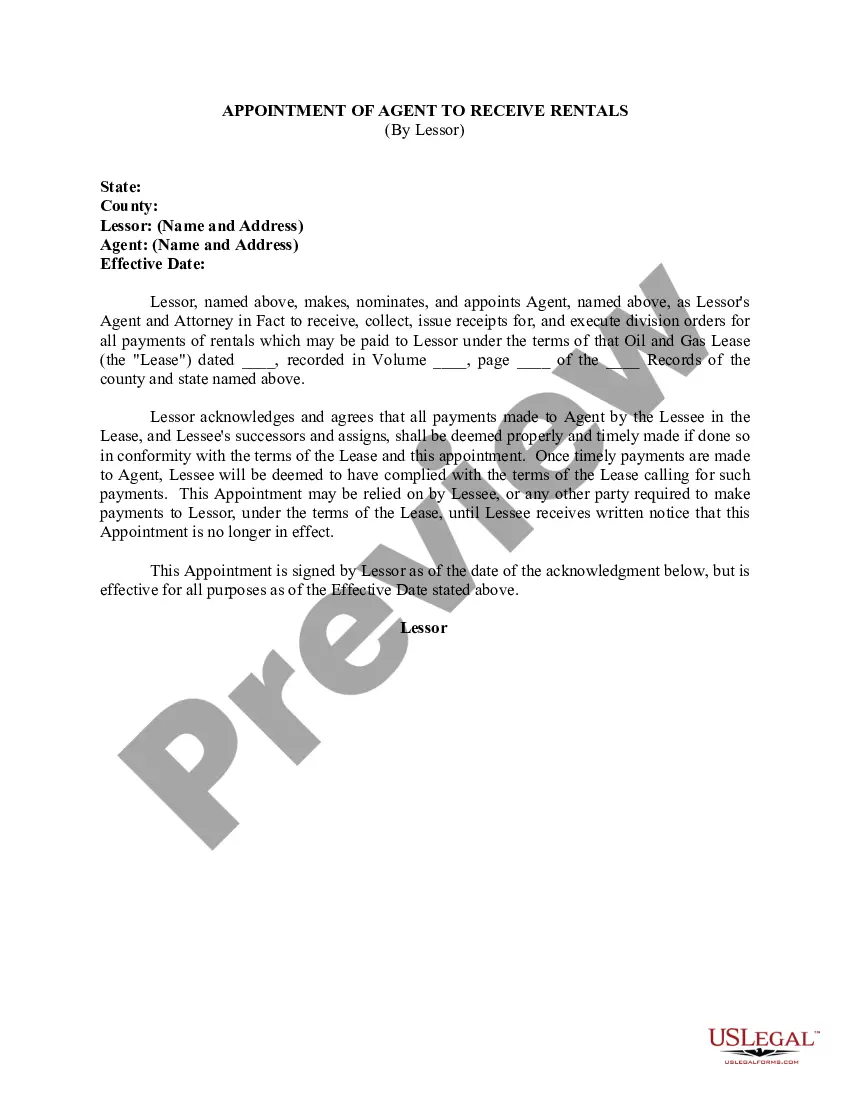

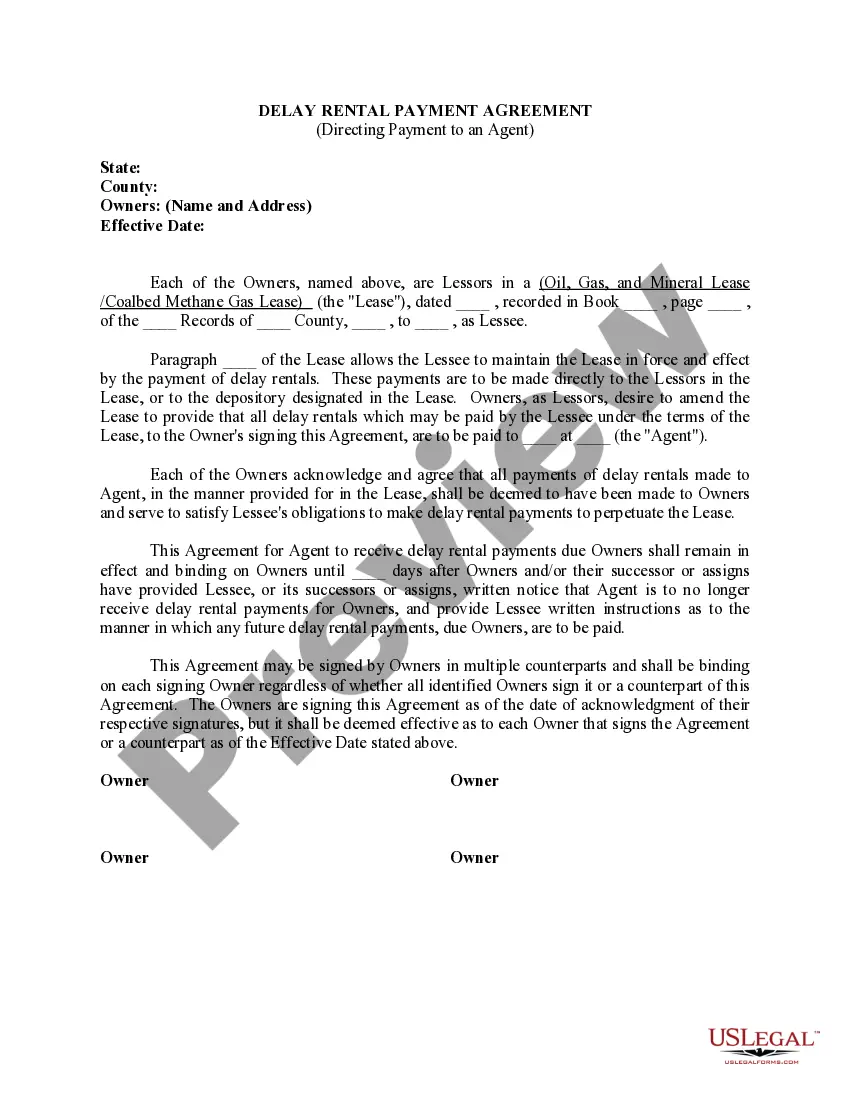

District of Columbia Direction For Payment of Royalty to Trustee by Royalty Owners

Description

How to fill out Direction For Payment Of Royalty To Trustee By Royalty Owners?

US Legal Forms - among the biggest libraries of legal types in America - gives a wide array of legal document web templates it is possible to acquire or print. Making use of the web site, you will get a large number of types for company and individual functions, sorted by types, states, or keywords and phrases.You will find the latest variations of types such as the District of Columbia Direction For Payment of Royalty to Trustee by Royalty Owners within minutes.

If you currently have a subscription, log in and acquire District of Columbia Direction For Payment of Royalty to Trustee by Royalty Owners from the US Legal Forms library. The Download button will appear on every kind you view. You have accessibility to all in the past delivered electronically types within the My Forms tab of the profile.

If you wish to use US Legal Forms the very first time, allow me to share easy instructions to get you began:

- Be sure you have picked the proper kind for the area/county. Select the Review button to examine the form`s information. See the kind outline to ensure that you have chosen the appropriate kind.

- When the kind does not suit your specifications, use the Look for area at the top of the monitor to get the one that does.

- If you are satisfied with the form, affirm your choice by clicking on the Get now button. Then, opt for the costs program you want and supply your credentials to sign up for an profile.

- Process the purchase. Make use of your Visa or Mastercard or PayPal profile to complete the purchase.

- Select the formatting and acquire the form in your gadget.

- Make alterations. Fill up, modify and print and sign the delivered electronically District of Columbia Direction For Payment of Royalty to Trustee by Royalty Owners.

Each format you added to your account lacks an expiry time and is also yours permanently. So, if you would like acquire or print one more duplicate, just go to the My Forms segment and click around the kind you need.

Get access to the District of Columbia Direction For Payment of Royalty to Trustee by Royalty Owners with US Legal Forms, one of the most considerable library of legal document web templates. Use a large number of specialist and status-particular web templates that satisfy your organization or individual demands and specifications.

Form popularity

FAQ

Generally, an unincorporated business, with gross income (Line 11) more than $12,000 from District sources, must file a D-30 (whether or not it has net income). This includes any business carrying on and/or engaging in any trade, business, or commercial activity in DC with income from DC sources.

Corporations with operations or income from DC need to file the District of Columbia Corporate Income Tax Form D-20 with the DC Office of Tax and Revenue. A minimum tax of $250 applies for businesses with DC gross receipts of $1 million or less, and $1,000 for receipts exceeding the $1 million mark.

Generally, every corporation or financial institution must file a Form D-20 (including small businesses, professional corporations, and S corporations) if it is carrying on or engaging in any trade, business, or commercial activity in the District of Columbia (DC) or receiving income from DC sources.

A return must be filed by an unincorporated business if its gross income from engaging in or carrying on any trade or business in DC plus any other gross income received from DC sources amounts to more than $12,000 during the year, regardless of whether it had net income.

Special rules on depreciation and business expenses For federal tax purposes, businesses may deduct bonus depre- ciation and additional IRC §179 expenses. DC does not allow the bonus depreciation deduction nor any additional IRC §179 expenses.

The filing of the D 30 is a requirement for operating or continuing to operate a motor vehicle for hire in the District by a non resident. The minimum tax is $250 if DC gross receipts are $1M or less.

Any non-resident of DC claiming a refund of DC income tax with- held or paid by estimated tax payments must file a D-40B. A non-resident is anyone whose permanent home was outside DC during all of 2022 and who did not maintain a place of abode in DC for a total of 183 days or more during 2022.

A business is exempt if more than 80% of gross income is derived from personal services rendered by the members of the entity and capital is not a material income-producing factor. A trade, business or professional organization that by law, customs or ethics cannot be incorporated is exempt.