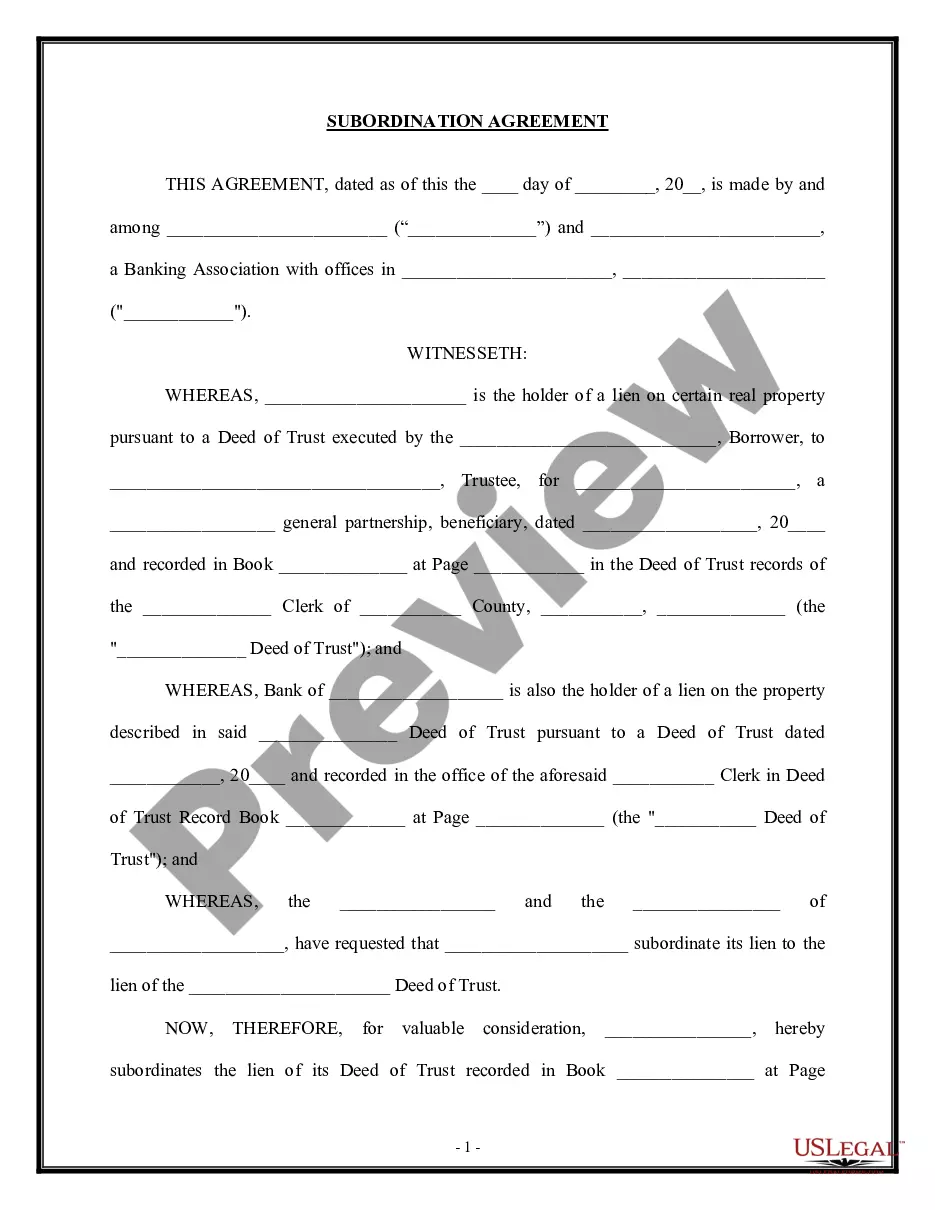

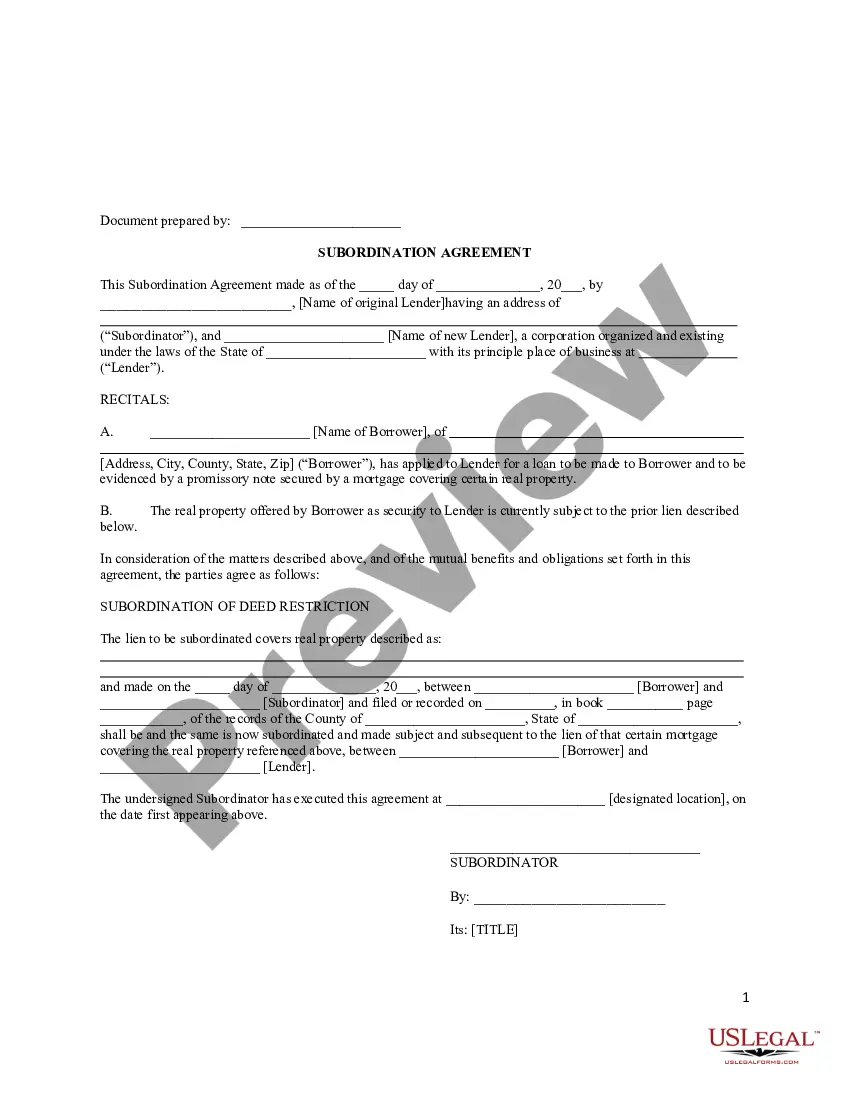

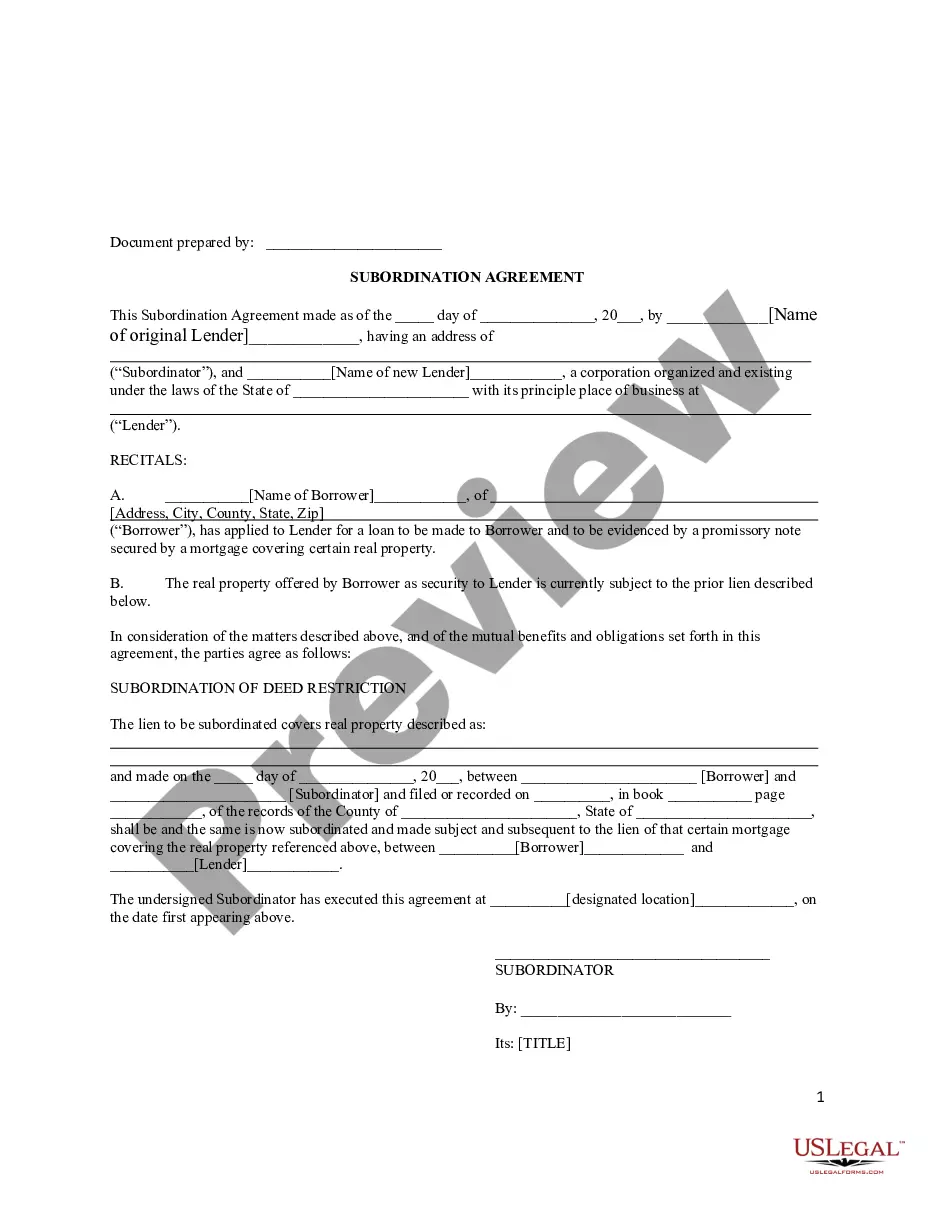

District of Columbia Subordination Agreement Subordinating Existing Mortgage to New Mortgage

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Subordination Agreement Subordinating Existing Mortgage To New Mortgage?

Finding the right authorized document format could be a have a problem. Needless to say, there are a lot of web templates accessible on the Internet, but how can you find the authorized type you need? Utilize the US Legal Forms internet site. The service provides a large number of web templates, including the District of Columbia Subordination Agreement Subordinating Existing Mortgage to New Mortgage, that you can use for business and private needs. All of the forms are examined by experts and meet up with federal and state needs.

If you are already authorized, log in to your account and then click the Download switch to find the District of Columbia Subordination Agreement Subordinating Existing Mortgage to New Mortgage. Make use of account to look through the authorized forms you may have bought in the past. Proceed to the My Forms tab of your own account and obtain yet another backup in the document you need.

If you are a whole new consumer of US Legal Forms, listed here are straightforward guidelines so that you can follow:

- Initial, make certain you have chosen the right type for your city/state. You may look over the form making use of the Preview switch and look at the form explanation to ensure it will be the right one for you.

- When the type will not meet up with your requirements, utilize the Seach discipline to find the correct type.

- Once you are positive that the form is suitable, go through the Purchase now switch to find the type.

- Pick the rates prepare you would like and enter in the necessary information. Build your account and purchase your order with your PayPal account or Visa or Mastercard.

- Select the submit format and down load the authorized document format to your device.

- Complete, revise and print out and indicator the obtained District of Columbia Subordination Agreement Subordinating Existing Mortgage to New Mortgage.

US Legal Forms may be the most significant local library of authorized forms for which you will find a variety of document web templates. Utilize the company to down load expertly-manufactured files that follow express needs.

Form popularity

FAQ

Many people have a subordinate mortgage in the form of a home equity line of credit or home equity loan. A subordinate mortgage is secured by your property but sits in second position, if you have a primary mortgage, for getting paid in the event you default. Subordinate Mortgage: What Is It and Why Does It Matter? - SoFi sofi.com ? learn ? content ? subordinate-mo... sofi.com ? learn ? content ? subordinate-mo...

As one of the final forms you receive before you close on your new loan, the Closing Disclosure allows you to compare your loan terms and costs to the terms listed in the Loan Estimate form you were given at the beginning of the process.

Again, if you're refinancing your first mortgage and the property also has a subordinate mortgage, the refinancing lender will usually handle the process of getting the necessary subordination agreement. But you need to ensure that the required subordination agreement is completed before the new loan's closing date. What Is a Subordination Agreement in Real Estate? - Nolo nolo.com ? legal-encyclopedia ? what-subor... nolo.com ? legal-encyclopedia ? what-subor...

Does a closing disclosure mean your loan is approved? No, a closing disclosure does not always mean your loan is approved. You may find incorrect information or something you want to change. Your lender also has the opportunity to back out if they find something new that makes them change their mind.

Required loan disclosures. (a)(1) A licensee who offers to make or procure a loan secured by a first or subordinate mortgage or deed of trust on a single to 4-family home shall provide the borrower with a financing agreement executed by the lender. § 26?1113. Required loan disclosures. | D.C. Law Library Council of the District of Columbia (.gov) ? council ? code ? sections Council of the District of Columbia (.gov) ? council ? code ? sections

Getting A Second Mortgage A second mortgage will become a subordinate loan. If you repay the primary loan within the term of the second mortgage, the second mortgage can take its place as the primary loan. What To Know About A Subordinate Mortgage rocketmortgage.com ? learn ? mortgage-sub... rocketmortgage.com ? learn ? mortgage-sub...

A Closing Disclosure is a five-page form that provides final details about the mortgage loan you have selected. It includes the loan terms, your projected monthly payments, and how much you will pay in fees and other costs to get your mortgage (closing costs).

If a mortgage loan application is approved and executed without the information in sections 1116.1 and 1116.2, the mortgage loan application shall be voidable by the borrower(s) prior to the loan closing and any fees submitted by the borrower(s) in connection with the application shall be returned to the borrower(s) in ...