The Fair Credit Reporting Act (FCRA) is designed to help ensure that credit bureaus furnish correct and complete information to businesses to use when evaluating your application. Your rights include:

The right to receive a copy of your credit report. The copy of your report must contain all of the information in your file at the time of your request.

The right to know the name of anyone who received your credit report in the last year for most purposes or in the last two years for employment purposes.

Any company that denies your application must supply the name and address of the credit bureau they contacted, provided the denial was based on information given by the credit bureau.

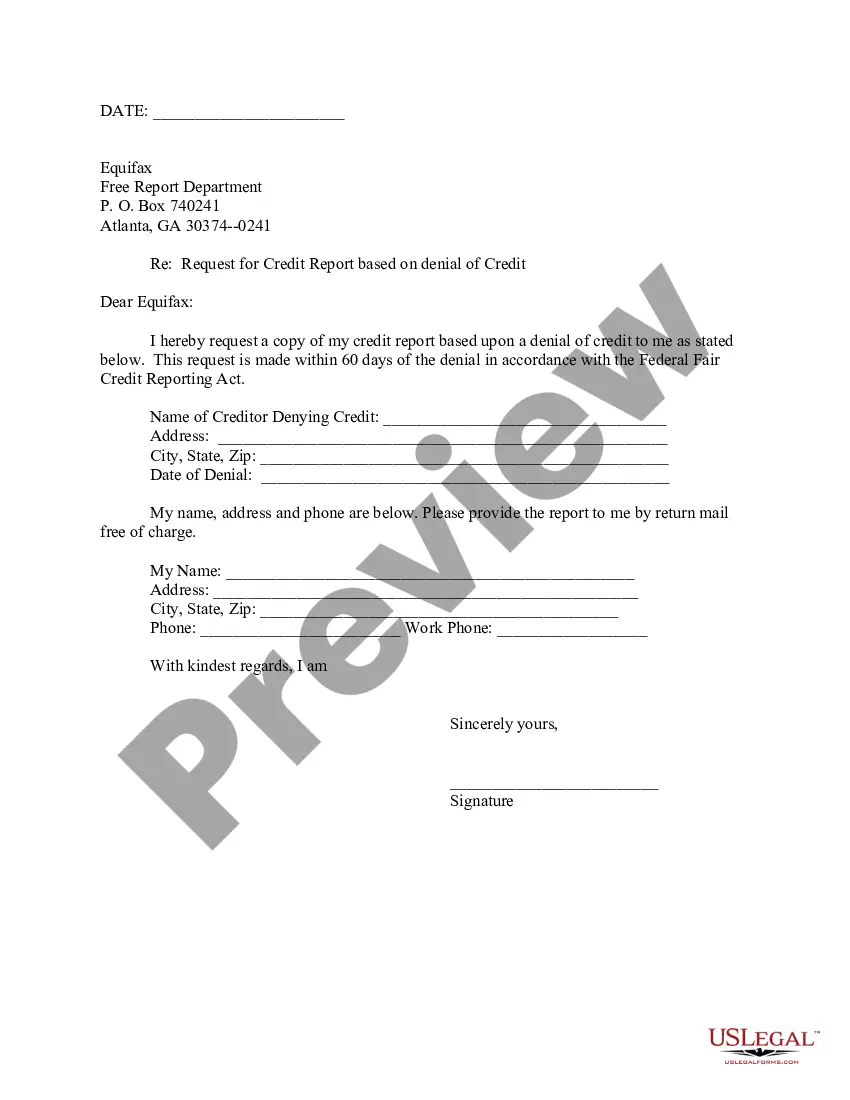

The right to a free copy of your credit report when your application is denied because of information supplied by the credit bureau. Your request must be made within 60 days of receiving your denial notice.

If you contest the completeness or accuracy of information in your report, you should file a dispute with the credit bureau and with the company that furnished the information to the bureau. Both the credit bureau and the furnisher of information are legally obligated to investigate your dispute.

A right to add a summary explanation to your credit report if your dispute is not resolved to your satisfaction.

District of Columbia Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency

Description

How to fill out Request For Disclosure Of Reasons For Denial Of Credit Application Where Action Was Based On Information Not Obtained By Reporting Agency?

Finding the right legitimate document web template can be a battle. Naturally, there are a variety of layouts accessible on the Internet, but how will you obtain the legitimate form you will need? Use the US Legal Forms site. The assistance delivers 1000s of layouts, like the District of Columbia Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency, which you can use for company and personal requirements. Every one of the forms are inspected by pros and fulfill state and federal requirements.

When you are currently signed up, log in in your profile and then click the Acquire switch to have the District of Columbia Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency. Utilize your profile to search with the legitimate forms you may have acquired earlier. Check out the My Forms tab of your respective profile and obtain an additional backup of the document you will need.

When you are a brand new user of US Legal Forms, listed here are straightforward guidelines so that you can stick to:

- Initially, make sure you have chosen the right form for your metropolis/state. It is possible to look through the shape while using Preview switch and browse the shape description to guarantee it will be the best for you.

- When the form fails to fulfill your preferences, use the Seach area to find the correct form.

- When you are certain that the shape is proper, click on the Purchase now switch to have the form.

- Select the costs strategy you want and enter the required details. Design your profile and buy an order using your PayPal profile or bank card.

- Pick the file structure and download the legitimate document web template in your device.

- Complete, edit and produce and sign the received District of Columbia Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency.

US Legal Forms is the largest catalogue of legitimate forms where you can discover numerous document layouts. Use the service to download skillfully-created documents that stick to state requirements.

Form popularity

FAQ

Upon receiving a consumer's proper notice of dispute, the furnisher must conduct a reasonable investigation of the dispute. The furnisher also must review all relevant information provided by the consumer with the dispute notice.

The credit reporting company you sent the dispute letter to must investigate your dispute, forward copies of relevant documents to the company that provided the information about you, and report the results back to you. A credit reporting company is not required to take action about disputes that are frivolous.

Credit bureaus function as databases of information about you. After collecting it, they use that information to create a credit score, which most lenders use as criteria for approving a line of credit. The raw data, before it's used to create a credit score, is known as your credit reports.

If the disputed information is wrong or can't be verified, the company is required by law to delete or change the information. It also has to notify all of the credit reporting companies to which it provided the wrong information, so the credit reporting companies can update their files with the correct information.

The FCRA also requires a creditor to disclose, as applicable, a credit score it used in taking adverse action along with related information, including up to four key factors that adversely affected the consumer's credit score (or up to five factors if the number of inquiries made with respect to that consumer report ...

For the purposes of the Fair Credit Reporting Act (FCRA), a ?credit reporting agency? is any legal entity?such as a company or a person?who reports or collects your credit information. This can include: Credit bureaus, like Equifax, Experian, and TransUnion.

Regulation B A written statement of actual and specific reasons for the adverse action or, if not providing the specific reason within the written notice, a statement that the applicant has a right to receive the specific reason for adverse action if requested within 60 days of the notification.

Investigate the dispute and review all relevant information provided by the CRA about the dispute; report your findings to the CRA; provide corrected information to every CRA that received the information if your investigation shows the information is incomplete or inaccurate; and.