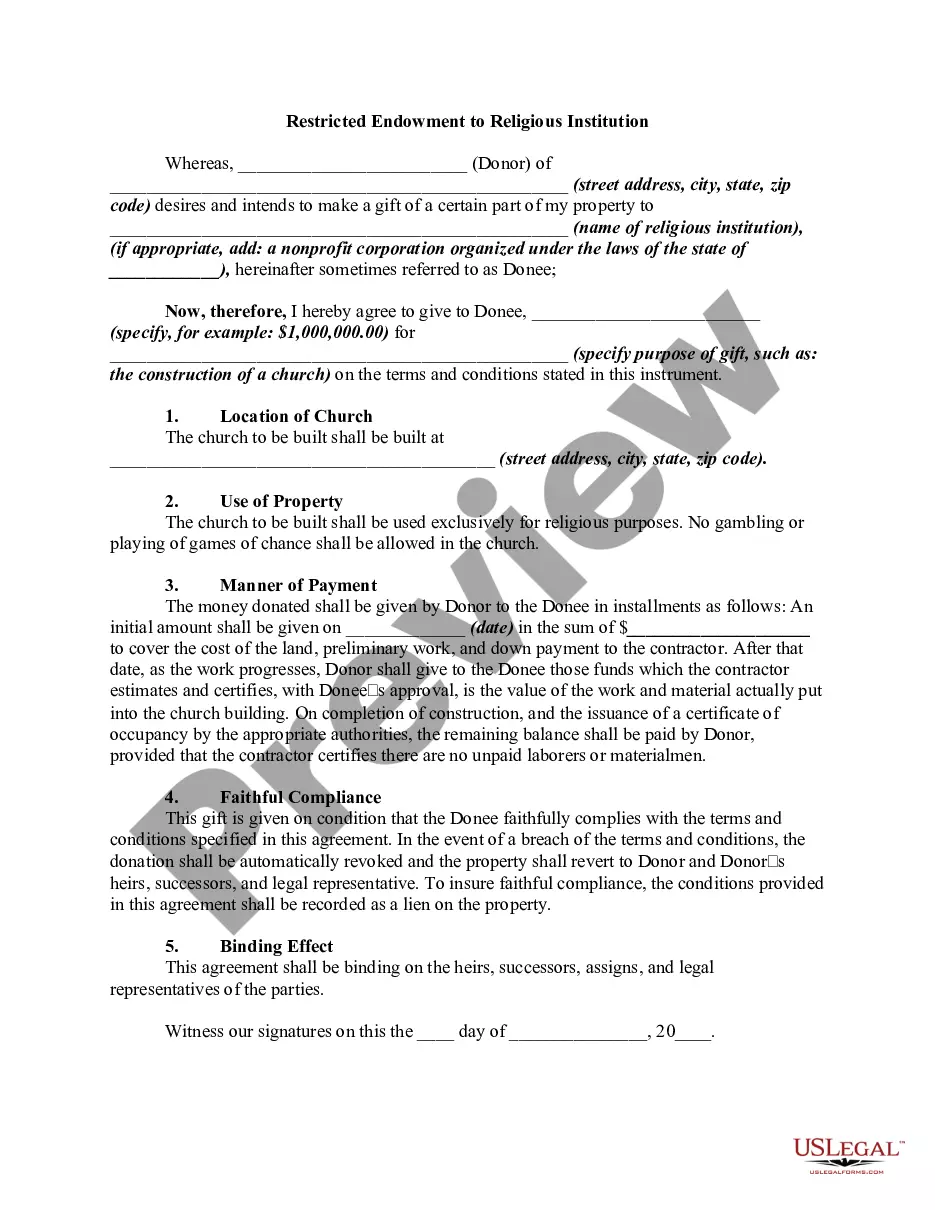

The following form is a gift for a restricted endowment to an educational, religious, or charitable institution.

District of Columbia Restricted Endowment to Educational, Religious, or Charitable Institution

Instant download

Description

How to fill out Restricted Endowment To Educational, Religious, Or Charitable Institution?

Selecting the optimum legal document format can be a challenge.

Of course, there are numerous templates accessible online, but how can you find the specific legal document you require.

Utilize the US Legal Forms website. This service provides a vast selection of templates, such as the District of Columbia Restricted Endowment to Educational, Religious, or Charitable Institution, which you can utilize for business and personal purposes.

If the form does not meet your requirements, use the Search field to locate the appropriate form.

- All forms are reviewed by experts and meet federal and state requirements.

- If you are already registered, Log In to your account and click on the Download button to obtain the District of Columbia Restricted Endowment to Educational, Religious, or Charitable Institution.

- Use your account to search through the legal forms you have purchased before.

- Navigate to the My documents tab of your account and acquire another copy of the document you need.

- If you are a new user of US Legal Forms, here are simple instructions for you to follow.

- First, ensure you have selected the correct form for the area/region. You can review the form using the Review button and examine the form details to confirm it is suitable for you.

Form popularity

FAQ

An endowment under UPMIFA refers to funds that have been set aside by an institution to provide long-term support according to legal guidelines. UPMIFA ensures that the funds are managed prudently and spent in a manner aligned with the institution's mission. For those involved with a District of Columbia Restricted Endowment to Educational, Religious, or Charitable Institution, understanding UPMIFA’s provisions is essential to navigate the responsibilities and benefits that come with managing those funds.

There are four main types of endowments: temporary, term, permanent, and quasi endowments. Each type serves different purposes in funding and supporting institutional goals. For a District of Columbia Restricted Endowment to Educational, Religious, or Charitable Institution, identifying the appropriate type of endowment is crucial to maximizing impact and meeting the institution’s financial needs.

The UPMIFA endowment is designed to govern how institutions manage their endowment funds, ensuring they meet both legal and ethical obligations. This legislation sets guidelines on spending, investment strategies, and the duties of fiduciaries responsible for overseeing these funds. In the context of a District of Columbia Restricted Endowment to Educational, Religious, or Charitable Institution, adherence to UPMIFA helps ensure that funds are utilized effectively for their intended purposes.

UPMIFA, or the Uniform Prudent Management of Institutional Funds Act, outlines several important factors for managing endowment funds. These factors include the purpose of the institution, the investment strategy, and the overall economic conditions. Understanding these factors is essential for any entity dealing with a District of Columbia Restricted Endowment to Educational, Religious, or Charitable Institution to ensure compliance and proper fund management.

An endowment fund is a financial asset that is established for a specific purpose, often to support educational, religious, or charitable institutions. The funds are typically invested, and the income generated is used to support the institution’s mission. In the context of District of Columbia Restricted Endowment to Educational, Religious, or Charitable Institution, these funds ensure long-term financial stability and support for programs that benefit the community.

The UCLA endowment is a significant sum dedicated to supporting various programs and initiatives within the university. However, discussing UCLA’s endowment directly may not connect with the District of Columbia Restricted Endowment to Educational, Religious, or Charitable Institution. This particular type of endowment is designed to provide financial resources to institutions specifically in the District of Columbia. If you would like to learn more about how endowments work or how they can be structured, consider exploring US Legal Forms for guidance and resources.

Yes. Endowments are governed by UPMIFA, which is discussed in a prior blog post. UPMIFA provides that the terms of an endowment can be changed by written agreement between the donor and the charity.

Rather, unrestricted endowment funds are donor-restricted perpetual funds but the earnings (from the spending policy) can be used for general activities of the organization.

In most cases, an endowment is a legal entity, such as a trust or corporation, entirely separate from the non-profit group that receives the benefit. If the benefiting party is a tax-exempt organization, the endowment qualifies for tax-exempt status, in which case any accrued earnings are not taxed.

In addition, UPMIFA does not apply to private foundations held by individual trustees or commercial trustees, such as banks or trust companies, even if the sole beneficiary is a charity. Such trusts are instead governed by the instruments establishing them and applicable state trust law.