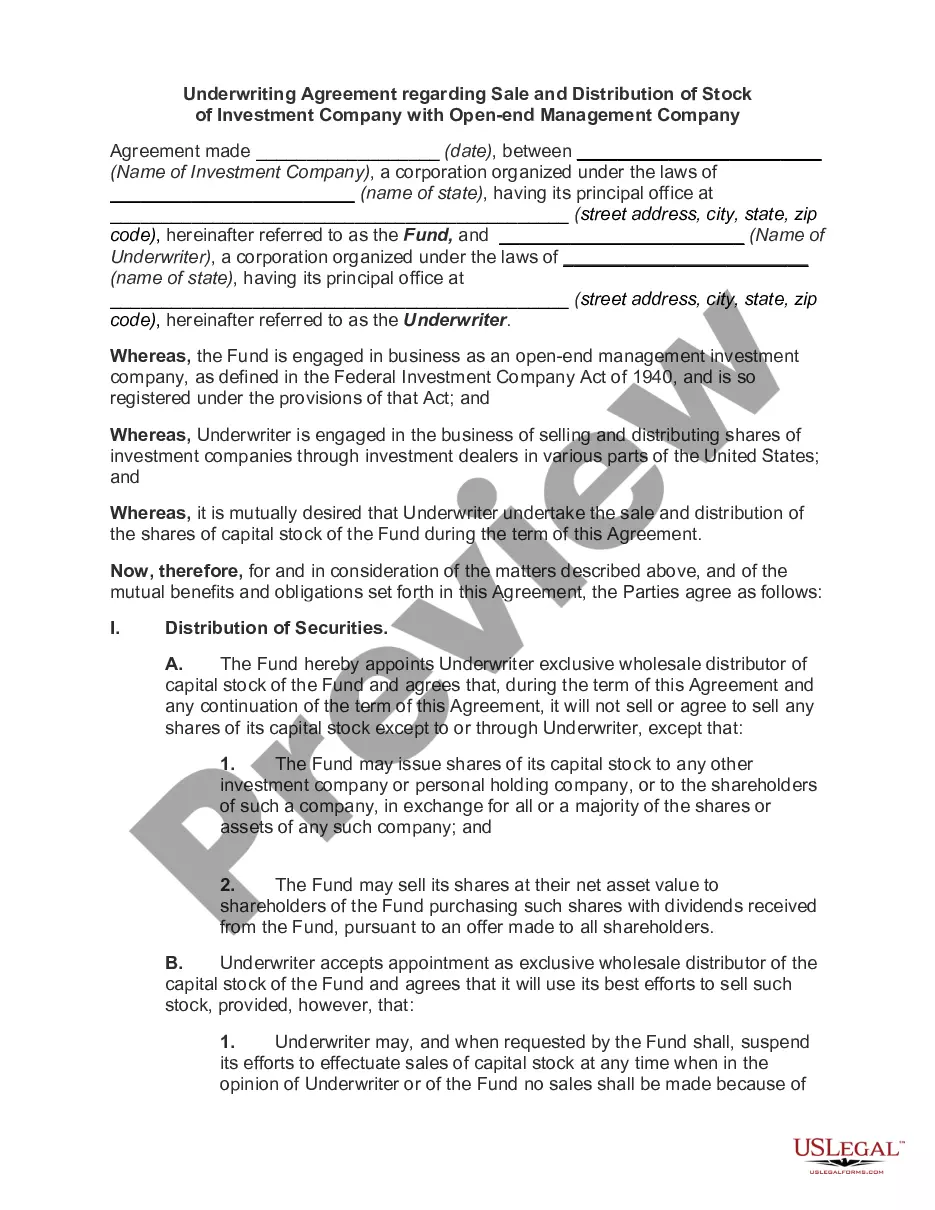

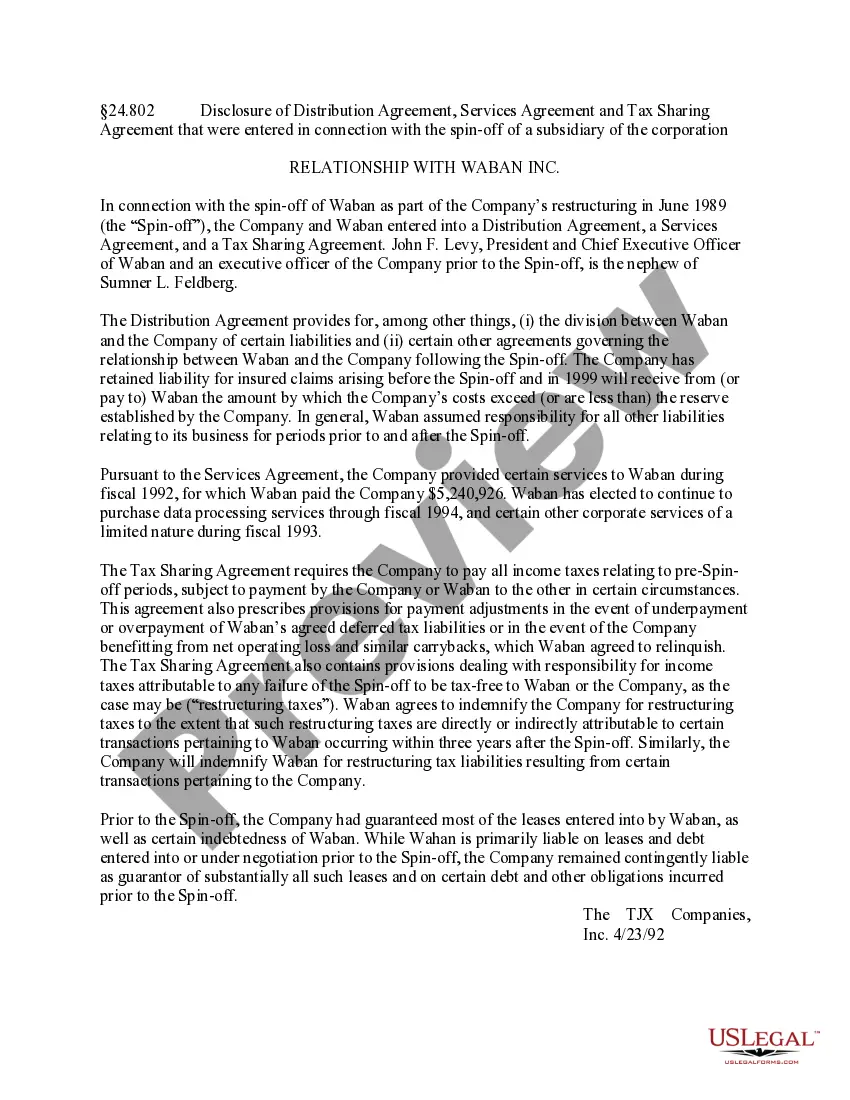

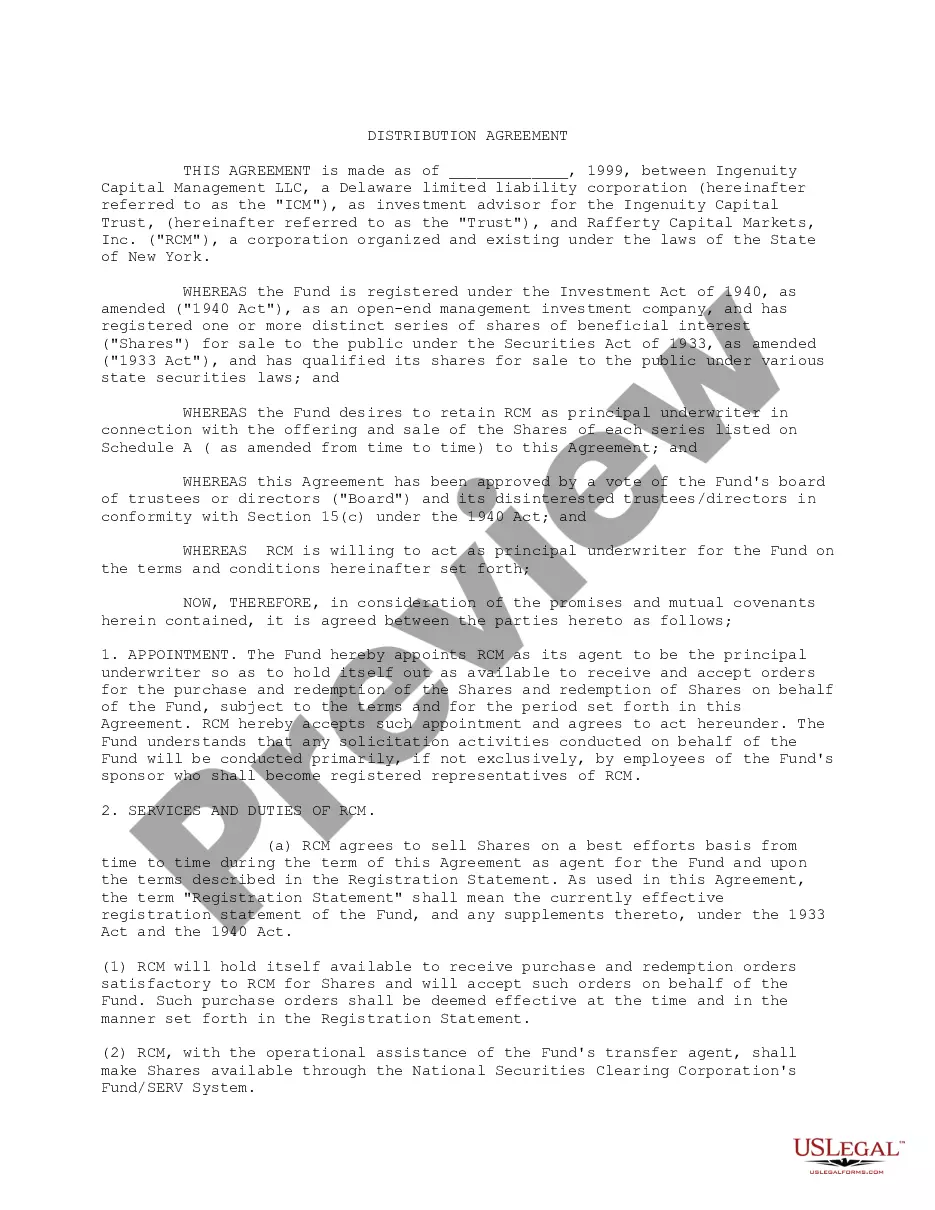

Connecticut Distribution Agreement regarding the continuous offering of the Fund's shares

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Distribution Agreement Regarding The Continuous Offering Of The Fund's Shares?

Discovering the right lawful file template can be quite a struggle. Needless to say, there are plenty of templates available on the net, but how do you find the lawful kind you will need? Take advantage of the US Legal Forms web site. The services delivers a huge number of templates, such as the Connecticut Distribution Agreement regarding the continuous offering of the Fund's shares, which you can use for company and personal needs. All of the kinds are checked out by pros and fulfill state and federal demands.

In case you are presently authorized, log in in your accounts and click the Download option to find the Connecticut Distribution Agreement regarding the continuous offering of the Fund's shares. Make use of your accounts to search with the lawful kinds you may have bought earlier. Check out the My Forms tab of your accounts and acquire one more backup of the file you will need.

In case you are a brand new end user of US Legal Forms, listed here are simple directions so that you can comply with:

- First, make certain you have chosen the right kind for your area/area. You are able to look over the shape while using Review option and look at the shape information to guarantee this is the best for you.

- In the event the kind does not fulfill your preferences, use the Seach industry to get the appropriate kind.

- Once you are positive that the shape is suitable, go through the Buy now option to find the kind.

- Choose the costs prepare you need and enter the required information. Build your accounts and pay for the transaction using your PayPal accounts or bank card.

- Pick the file structure and down load the lawful file template in your device.

- Comprehensive, edit and produce and indicator the attained Connecticut Distribution Agreement regarding the continuous offering of the Fund's shares.

US Legal Forms may be the largest local library of lawful kinds that you can discover numerous file templates. Take advantage of the service to down load professionally-manufactured documents that comply with condition demands.

Form popularity

FAQ

In an equity distribution agreement (also sometimes referred to as a "sales agency agreement" or "placement agency agreement"), a company engages a broker-dealer to conduct ATM offerings of the company's shares under an ATM program (also commonly referred to as an "equity distribution program" or "equity dribble out ...

WHAT IS EQUITY DISTRIBUTION, ROC NATION'S INDIE DISTRIBUTION COMPANY? ?Equity Distribution is a global music distribution platform that allows artists to retain ownership of their masters.

A continuously offered closed-end fund is a type of investment company that periodically offers to buy back a stated portion of its shares from shareholders, generally every three, six, or twelve months, as disclosed in the fund's prospectus.

An equity distribution agreement is a contract typically used by a company that offers another party the ability to distribute shares through what's known as an at-the-market (or ATM) offering program. Companies typically use profits from the distribution of their shares for repayment of loans or refinancing.

Equitable distribution of income means that income is distributed in a way that ensures fairness and allows everyone to have the same opportunities. Equitable distribution of income doesn't mean that income is distributed equally; it just means that income is distributed in a fair way.

Distributionequity is characterized as the increase in options value ofmarketing opportunities that result when a firm effectively utilizesits knowledge relationships with an existing distribution channelpartner to create and market its products.