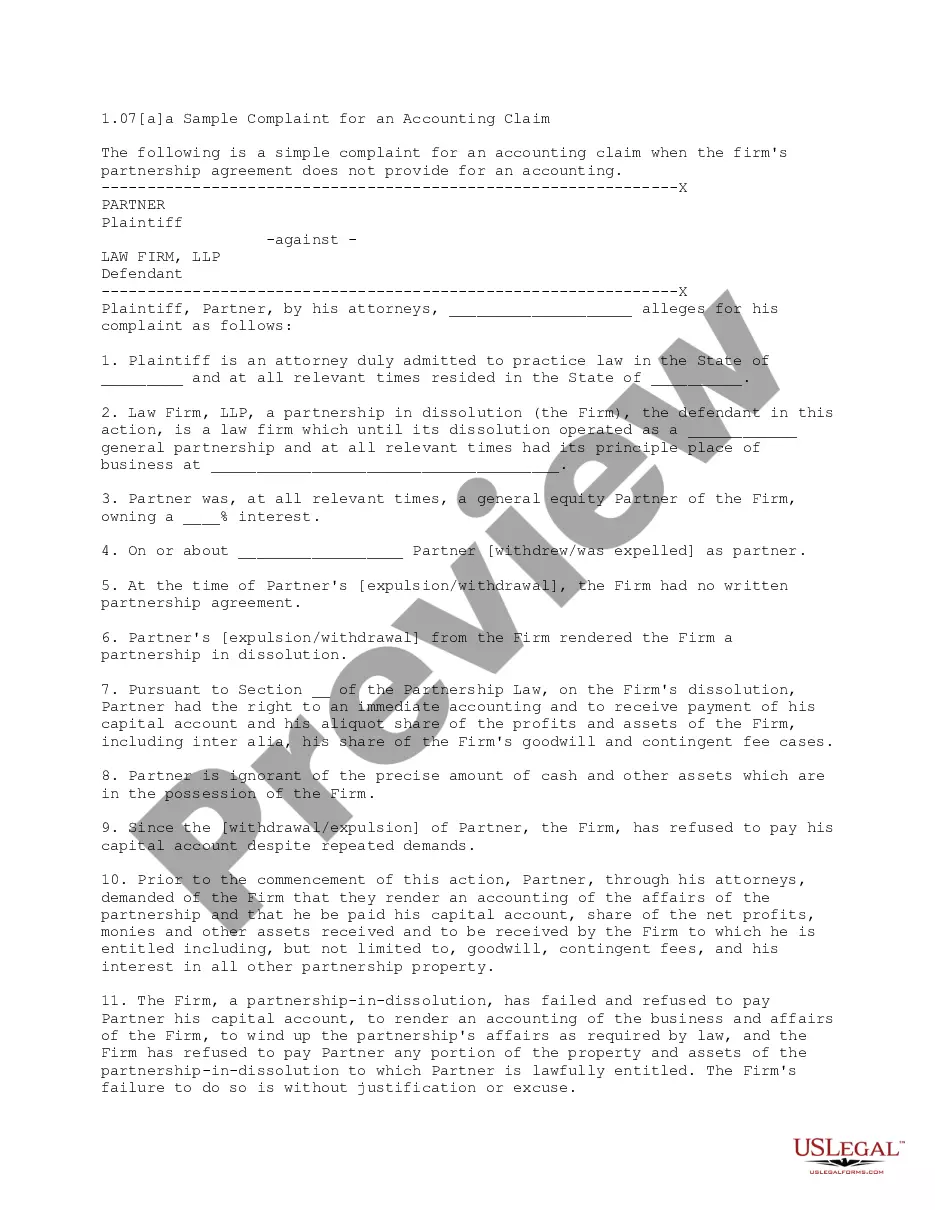

This complaint is for a plaintiff attorney who has been removed from the partnership of his former firm. The complaint requests an accounting of the former firm, stating that the plaintiff has been deprived of economic benefits rightfully due to him under the former partnership agreement, and also alleges egregious acts by his former partners.

Colorado Alternative Complaint for an Accounting which includes Egregious Acts

Category:

State:

Multi-State

Control #:

US-L0107A

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Alternative Complaint For An Accounting Which Includes Egregious Acts?

If you need to comprehensive, download, or print out legal record layouts, use US Legal Forms, the biggest variety of legal varieties, which can be found on the web. Use the site`s simple and easy hassle-free lookup to discover the documents you will need. Various layouts for company and specific purposes are sorted by classes and states, or key phrases. Use US Legal Forms to discover the Colorado Alternative Complaint for an Accounting which includes Egregious Acts in just a handful of click throughs.

In case you are already a US Legal Forms customer, log in to your account and click on the Download option to find the Colorado Alternative Complaint for an Accounting which includes Egregious Acts. You may also accessibility varieties you in the past downloaded inside the My Forms tab of the account.

If you are using US Legal Forms the first time, refer to the instructions under:

- Step 1. Be sure you have selected the shape for the appropriate city/region.

- Step 2. Take advantage of the Review choice to look through the form`s information. Never neglect to read through the information.

- Step 3. In case you are not satisfied together with the develop, make use of the Look for area on top of the screen to locate other versions of the legal develop web template.

- Step 4. When you have identified the shape you will need, select the Get now option. Pick the costs plan you prefer and add your accreditations to register for an account.

- Step 5. Process the deal. You can use your charge card or PayPal account to finish the deal.

- Step 6. Find the format of the legal develop and download it on the system.

- Step 7. Comprehensive, modify and print out or indicator the Colorado Alternative Complaint for an Accounting which includes Egregious Acts.

Each and every legal record web template you purchase is the one you have eternally. You have acces to each and every develop you downloaded within your acccount. Click on the My Forms area and pick a develop to print out or download once again.

Compete and download, and print out the Colorado Alternative Complaint for an Accounting which includes Egregious Acts with US Legal Forms. There are thousands of specialist and condition-specific varieties you can utilize for your company or specific requirements.

Form popularity

FAQ

Colorado Employment Security Act (CESA) The Social Security Act of 1935 directed the establishment of Colorado's unemployment compensation program. Unemployment insurance provides temporary financial assistance to workers who have lost their jobs through no fault of their own.

Hundreds of Coloradans are still waiting to receive the unemployment money they're rightfully owed, because the Colorado Department of Labor and Employment says it's still working to clear fraud holds on their accounts, and to add insult to injury, claimants say they can't get adequate help from the department's ...

?Gross misconduct? means conduct evincing such willful or wanton disregard of an employer's interests or negligence or harm of such a degree or recurrence as to manifest culpability or wrongful intent, or assault or threatened assault upon supervisors, coworkers, or others at the work site.

You may be required to pay unemployment insurance premiums if you meet one or more of the following requirements: Paid wages of $1,500 or more in a calendar quarter during the current or preceding calendar year or, employed at least one person for some portion of a day in each of 20 different weeks during the current ...

If you quit your job, you won't be eligible for unemployment benefits unless you had good cause for quitting. In general, the good cause requirement will be satisfied if you left your job for any of the following reasons: domestic violence (you had to leave the area in order to avoid further violence or harassment)

?Gross misconduct? means conduct evincing such willful or wanton disregard of an employer's interests or negligence or harm of such a degree or recurrence as to manifest culpability or wrongful intent, or assault or threatened assault upon supervisors, coworkers, or others at the work site.