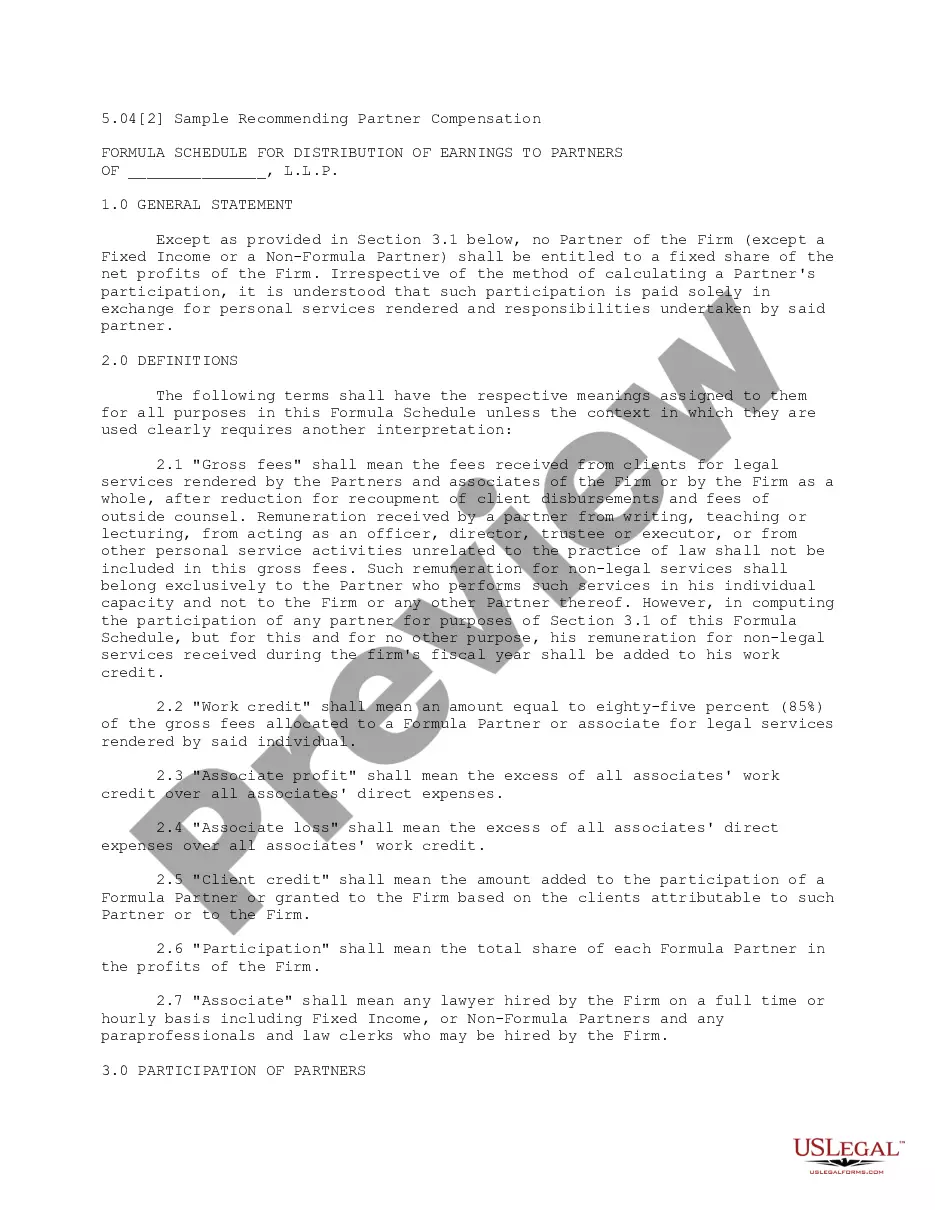

This Formula System for Distribution of Earnings to Partners provides a list of provisions to conside when making partner distribution recommendations. Some of the factors to consider are: Collections on each partner's matters, acquisition and development of new clients, profitablity of matters worked on, training of associates and paralegals, contributions to the firm's marketing practices, and others.

California Formula System for Distribution of Earnings to Partners

Category:

State:

Multi-State

Control #:

US-L05041A

Format:

Word;

PDF;

Rich Text

Instant download

Description

Free preview

How to fill out Formula System For Distribution Of Earnings To Partners?

If you wish to comprehensive, down load, or produce legitimate record layouts, use US Legal Forms, the most important variety of legitimate kinds, which can be found online. Make use of the site`s simple and hassle-free research to obtain the paperwork you will need. Numerous layouts for organization and personal purposes are categorized by groups and suggests, or keywords and phrases. Use US Legal Forms to obtain the California Formula System for Distribution of Earnings to Partners within a few click throughs.

In case you are already a US Legal Forms customer, log in for your accounts and click on the Obtain option to get the California Formula System for Distribution of Earnings to Partners. You can also accessibility kinds you in the past delivered electronically from the My Forms tab of your accounts.

If you use US Legal Forms for the first time, follow the instructions listed below:

- Step 1. Make sure you have chosen the shape for that correct city/nation.

- Step 2. Make use of the Review solution to check out the form`s content. Do not neglect to see the information.

- Step 3. In case you are unsatisfied together with the type, use the Research area towards the top of the display screen to get other types of the legitimate type template.

- Step 4. After you have discovered the shape you will need, click on the Get now option. Select the costs prepare you favor and put your credentials to register to have an accounts.

- Step 5. Method the purchase. You can use your Мisa or Ьastercard or PayPal accounts to complete the purchase.

- Step 6. Select the formatting of the legitimate type and down load it in your product.

- Step 7. Complete, modify and produce or sign the California Formula System for Distribution of Earnings to Partners.

Each legitimate record template you get is yours for a long time. You have acces to every type you delivered electronically inside your acccount. Go through the My Forms segment and select a type to produce or down load once more.

Remain competitive and down load, and produce the California Formula System for Distribution of Earnings to Partners with US Legal Forms. There are many expert and status-specific kinds you can use for your organization or personal needs.

Form popularity

FAQ

Partnerships are considered pass-through entities. That means that any income or losses are passed through the partnership to the individual owners, who are then responsible to account for that income or loss on their income tax returns.

The net income for a partnership is divided between the partners as called for in the partnership agreement. The income summary account is closed to the respective partner capital accounts. The respective drawings accounts are closed to the partner capital accounts.

All trade or businesses, except those that derive more than 50% of their gross receipts from qualified business activities (QBA), must apportion their business income to California using a single-sales factor.

The highest-income Californians pay the largest share of the state's personal income tax. For the 2019 tax year, the top 1 percent of income earners paid almost 45 percent of all personal income taxes.

Answer: Apportioning trades or businesses (including pass-through entities) that use a special formula under CCR sections 25137-1 to -14 must use the single-sales factor to apportion its business income to California except for those that derive more than 50% of their gross business receipts from QBAs.

An $800 annual tax is generally imposed on LPs, LLCs classified as partnerships for tax purposes, LLPs, and REMICs that are partnerships or are classified as partnerships for tax purposes. Distributions to certain nonresident partners are subject to withholding for California tax.

If you are a nonresident with a business, trade, or profession that conducts business both within and outside California, the income generated from business you conduct within California is California source-income and is taxable in the state.

The California Franchise Tax rates depend on your business's tax classification: C corporations: 8.84% S corporations: 1.5% Partnerships (such as LLCs, LPs, LLPs, LLLPs): $800.