Arizona Checklist for Proving Entertainment Expenses

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Checklist For Proving Entertainment Expenses?

If you require extensive, acquire, or print authentic document templates, use US Legal Forms, the largest repository of legal forms available on the web.

Utilize the site’s straightforward and user-friendly search to obtain the documents you need.

Various templates for business and personal purposes are categorized by groups and states or keywords.

Step 4. Once you have found the form you need, click the Buy now option. Choose your pricing plan and enter your details to create an account.

Step 5. Complete the payment process. You may use your Visa, MasterCard, or PayPal account to finalize the transaction.

- Use US Legal Forms to access the Arizona Checklist for Proving Entertainment Expenses in just a few clicks.

- If you are already a US Legal Forms user, sign in to your account and click the Get option to locate the Arizona Checklist for Proving Entertainment Expenses.

- You can also find forms you previously downloaded in the My documents section of your account.

- If this is your first time using US Legal Forms, follow the instructions below.

- Step 1. Ensure you have selected the form for your appropriate city/state.

- Step 2. Use the Preview option to review the form’s content. Make sure to check the description.

- Step 3. If you are not satisfied with the type, use the Search area at the top of the screen to find alternative versions of the legal form template.

Form popularity

FAQ

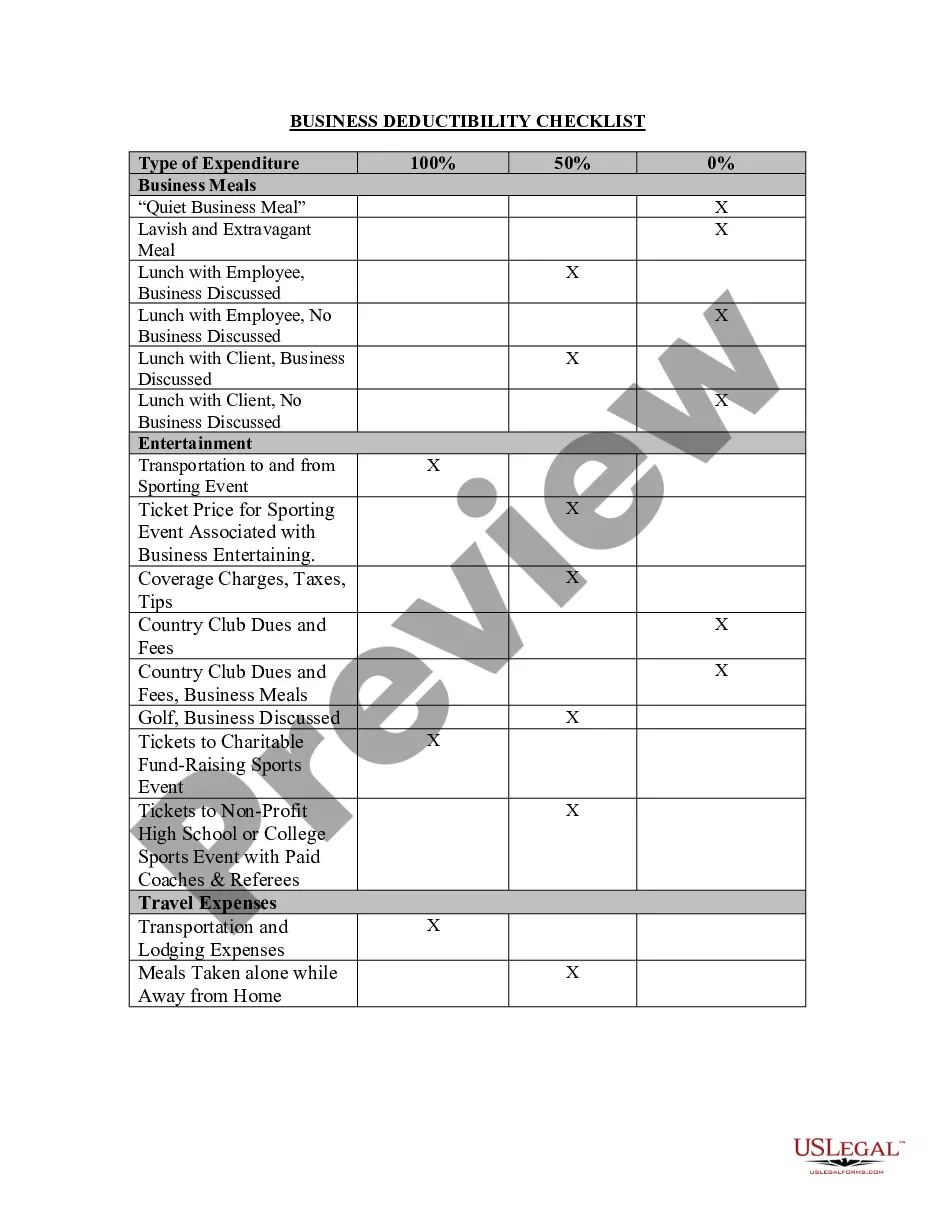

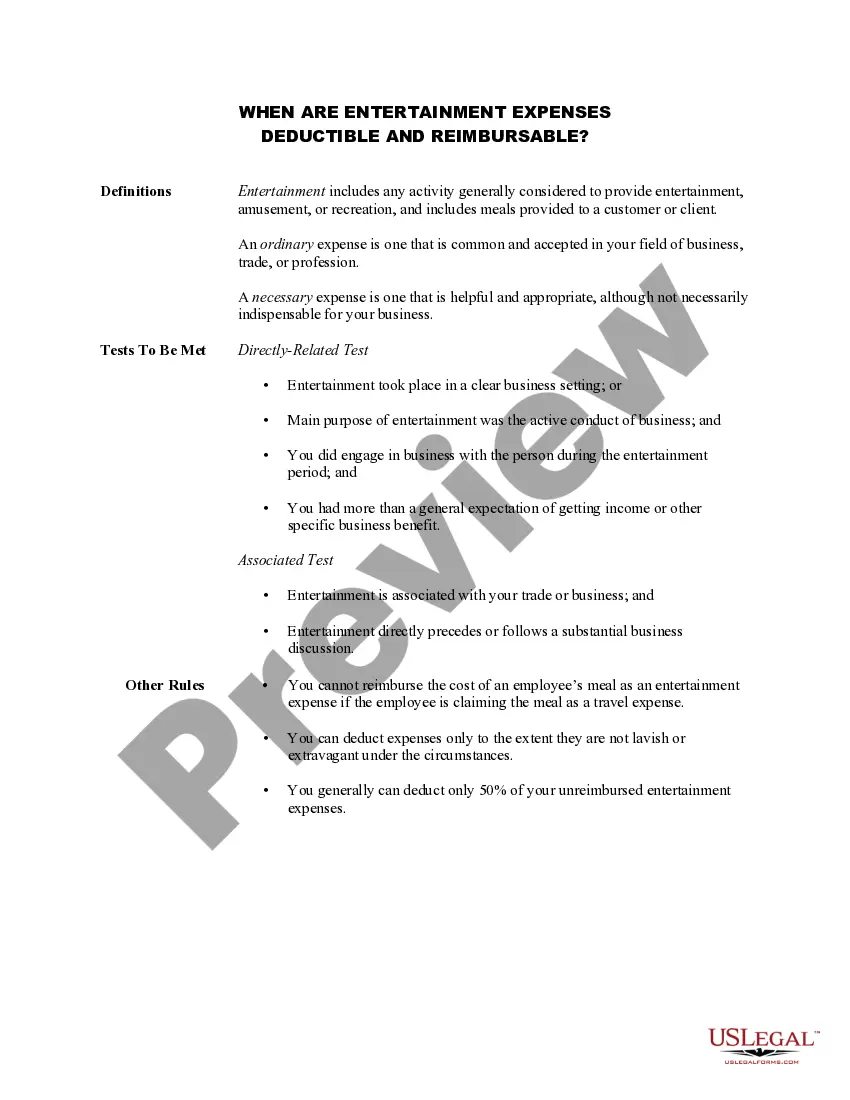

Tax relief for staff entertaining Staff entertaining is generally considered to be an allowable business expense and is therefore tax deductible. Allowable costs in this context include food, drink, entertainment, venue hire, transport and overnight accommodation.

Entertainment expenses include the cost of entertaining customers or employees at social and sports events, restaurant meals and theater tickets, among other things. You may deduct business entertainment expenses subject to certain conditions.

Generally, the IRS doesn't allow business to deduct costs for activities generally considered entertainment, amusement, or recreation, or for a facility used in connection with such activity. Taking a client or customer 200bto an "experience" is no longer deductible.

We have two bookkeeping recommendations for expenses: Travel expenses should be completely separate from entertainment, including meals while traveling. Travel expenses are 100% deductible, except for meals while traveling, which are 50% deductible in 2020 but 100% deductible in 2021/22.

Food and beverages will be 100% deductible if purchased from a restaurant in 2021 and 2022. This temporary 100% deduction was designed to help restaurants, many of which have been hard-hit by the COVID-19 pandemic. Entertainment expenses, like a sporting event or tickets to a show, are still non-deductible.

Anything considered to constitute entertainment, amusement, or recreation is nondeductible, including the cost of facilities used in connection with these activities. This is unchanged from 2018 tax reform.

Generally, the answer is that you can deduct ordinary and necessary expenses to entertain a customer or client if:Your expenses are of a type that qualifies as meals or entertainment.Your expenses bear the necessary relationship to your business activities.You keep adequate records and can substantiate the expenses.

Entertaining clients (concert tickets, golf games, etc.) Wondering how this breaks down? If you're dining out with a client at a restaurant, you can consider that meal 100% tax-deductible. However, if you're entertaining that same client in-office with snacks purchased at a grocery store, the meal is 50% deductible.

Generally, the IRS doesn't allow business to deduct costs for activities generally considered entertainment, amusement, or recreation, or for a facility used in connection with such activity. Taking a client or customer 200bto an "experience" is no longer deductible.