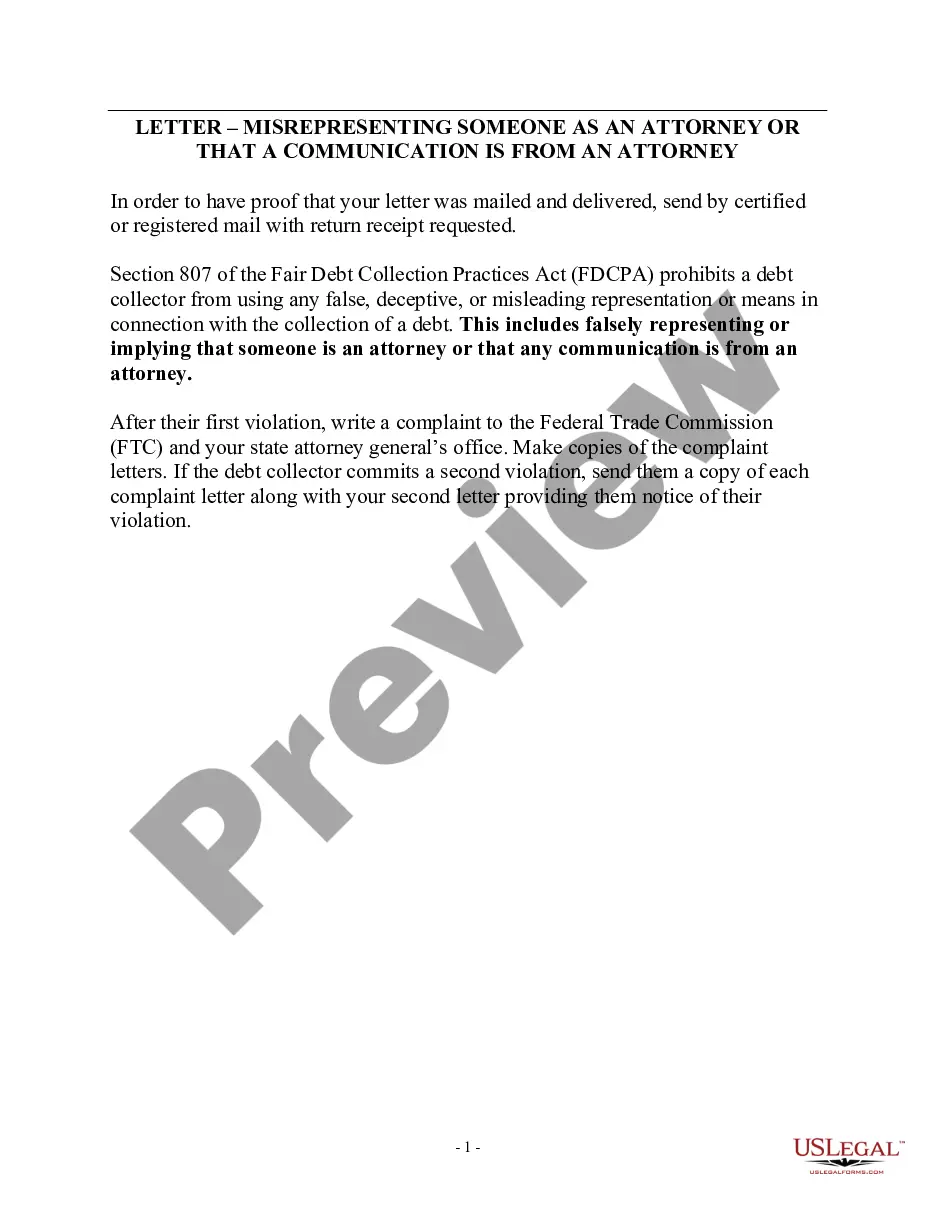

Arkansas Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself

Description

How to fill out Notice Of Violation Of Fair Debt Act - Creditor Misrepresented Himself?

If you require to obtain, acquire, or print legal document templates, utilize US Legal Forms, the largest collection of legal forms that is accessible online.

Employ the website's straightforward and user-friendly search functionality to find the documents you require.

Various templates for business and personal purposes are organized by categories and states, or keywords. Use US Legal Forms to obtain the Arkansas Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself in just a few clicks.

Every legal document template you acquire is yours indefinitely. You have access to every form you downloaded in your account.

Click the My documents section and select a form to print or download again. Compete and retrieve, and print the Arkansas Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself with US Legal Forms. There are millions of professional and state-specific forms available for your business or personal needs.

- If you are currently a US Legal Forms subscriber, Log In to your account and click the Download option to retrieve the Arkansas Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself.

- You can also access forms you have previously downloaded in the My documents tab of your account.

- If you are using US Legal Forms for the first time, follow the instructions below.

- Step 1. Ensure you have chosen the form for the correct city/state.

- Step 2. Use the Preview option to review the form's details. Remember to check the description.

- Step 3. If you are not satisfied with the form, use the Search bar at the top of the screen to find alternative versions of the legal form template.

- Step 4. Once you have found the form you require, click the Get now option. Choose your preferred payment method and enter your details to register for an account.

- Step 5. Complete the transaction. You can use your credit card or PayPal account to finalize the payment.

- Step 6. Select the format of the legal form and download it onto your device.

- Step 7. Fill out, modify, and print or sign the Arkansas Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself.

Form popularity

FAQ

Among the insider tips, Ulzheimer shared with the audience was this: if you are being pursued by debt collectors, you can stop them from calling you ever again by telling them '11-word phrase'. This simple idea was later advertised as an '11-word phrase to stop debt collectors'.

The statute of limitations is a law that limits how long debt collectors can legally sue consumers for unpaid debt. The statute of limitations on debt varies by state and type of debt, ranging from three years to as long as 20 years.

In California, the statute of limitations on most debts is four years. With some limited exceptions, creditors and debt buyers can't sue to collect debt that is more than four years old. When the debt is based on a verbal agreement, that time is reduced to two years.

If a debt collector violates the FDCPA, you may sue that collector in state or federal court. You can even sue in small claims court. You must do this within one year from the date on which the violation occurred.

The FDCPA defines a "creditor" as the person or entity that extended you the credit in the first place (in other words, your original lender). Because the FDCPA is designed to protect debtors against third-party debt collectors, it doesn't apply to your original creditor or its employees.

Your credit card debt, auto loans, medical bills, student loans, mortgage, and other household debts are covered under the FDCPA.

In cases against consumers for unpaid debts, the statute of limitations is three years in Arkansas. To achieve this short statute of limitations period, it must be filed as breach of contract claims, and there cannot be proof in writing, under A.C.A. 16- 56-105.

The statute of limitations for most debts, under Arkansas law, ranges from two to five years. Debt collectors are not allowed to call you at work. Ever. If they call after you have asked them to stop, you may have a claim under the Fair Debt Collection Practices Act.

7 Most Common FDCPA ViolationsContinued attempts to collect debt not owed.Illegal or unethical communication tactics.Disclosure verification of debt.Taking or threatening illegal action.False statements or false representation.Improper contact or sharing of info.Excessive phone calls.

Unless your state law provides otherwise, the FDCPA only requires debt collectors, not original creditors, to verify debts in certain circumstances. This requirement includes law firms that are routinely engaged in collecting debts.