Alabama Fair Credit Act Disclosure Notice

Description

How to fill out Fair Credit Act Disclosure Notice?

You are capable of spending several hours online searching for the authentic document template that meets the federal and state criteria you require.

US Legal Forms offers thousands of valid forms that are reviewed by specialists.

You can effortlessly download or print the Alabama Fair Credit Act Disclosure Notice from my services.

If available, utilize the Review button to browse through the document template simultaneously.

- If you already possess a US Legal Forms account, you may Log In and then click the Download button.

- Afterwards, you may complete, modify, print, or sign the Alabama Fair Credit Act Disclosure Notice.

- Every legal document template you acquire is yours indefinitely.

- To retrieve another version of any purchased form, navigate to the My documents tab and click the relevant button.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure that you have selected the correct document template for the county/city of your choice.

- Review the form outline to confirm you have chosen the right form.

Form popularity

FAQ

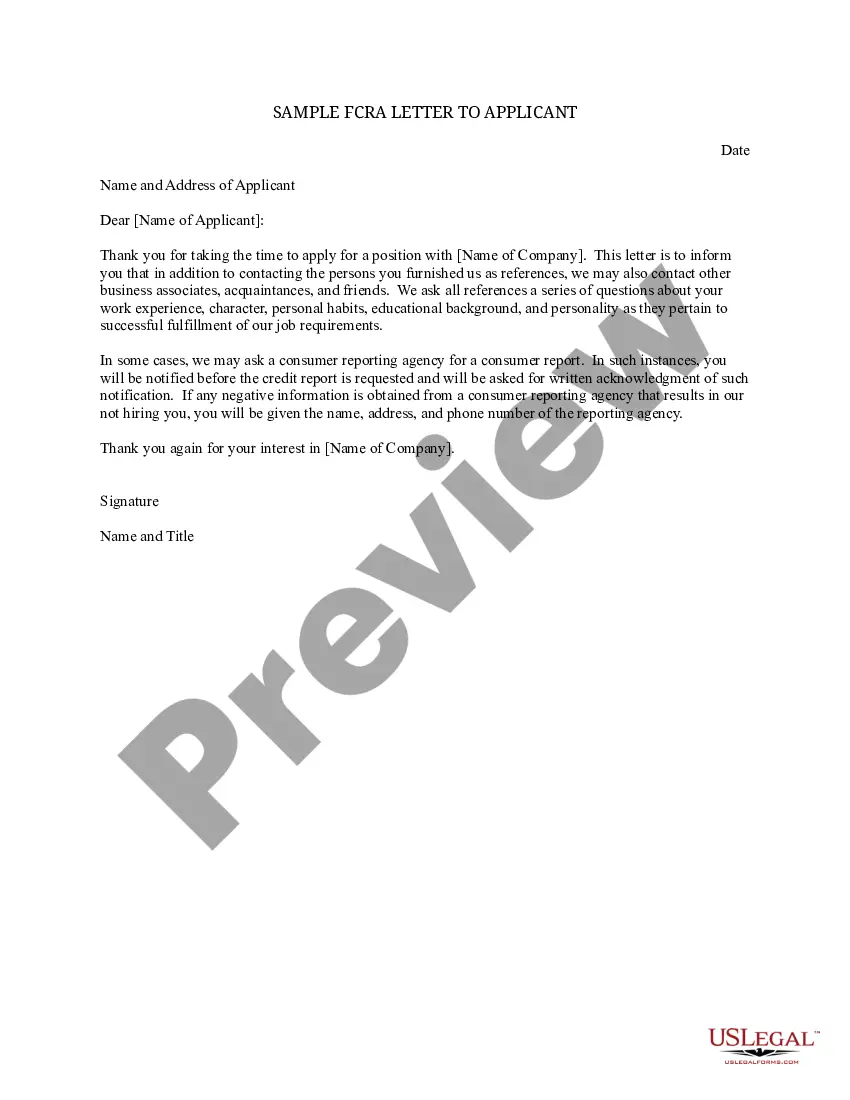

The Fair Credit Reporting Act (FCRA) is a federal law that helps to ensure the accuracy, fairness and privacy of the information in consumer credit bureau files. The law regulates the way credit reporting agencies can collect, access, use and share the data they collect in your consumer reports.

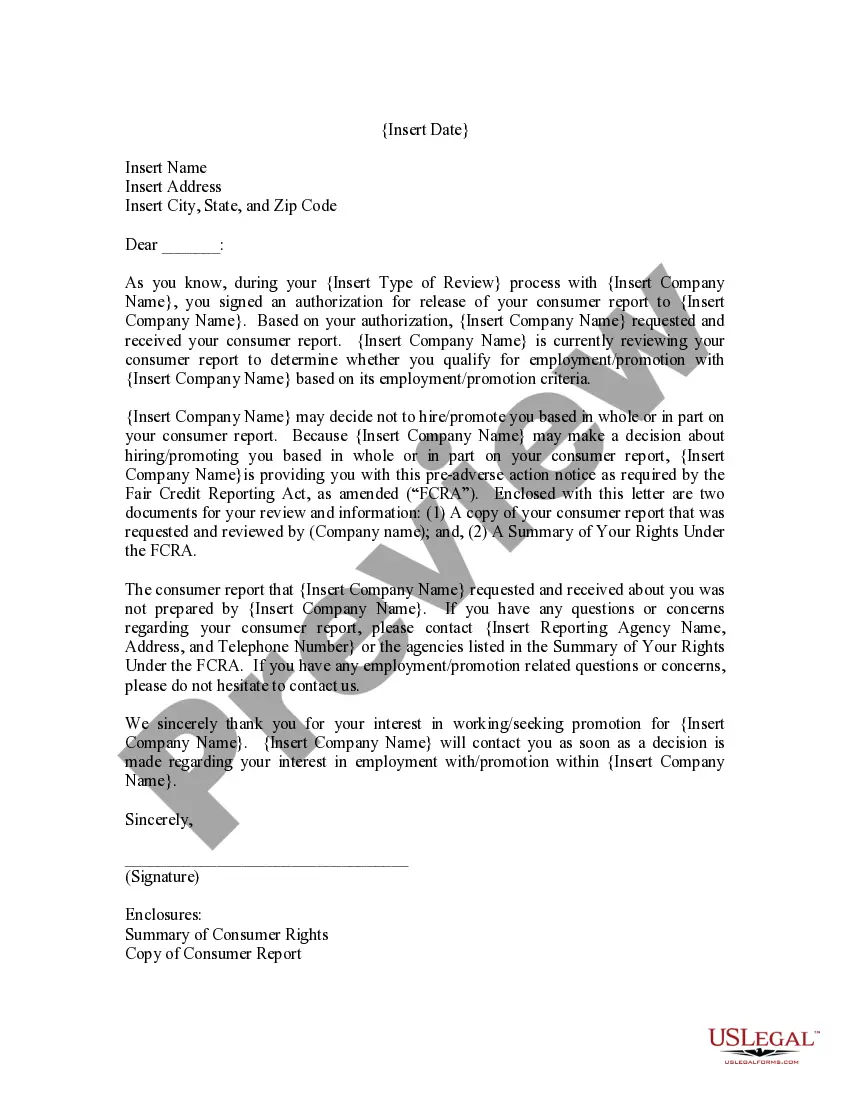

The Fair Credit Reporting Act (FCRA) is a federal law that requires you to make a disclosure to employees or applicants informing them that you will obtain a consumer report about them for employment consideration purposes.

The Fair Credit Reporting Act (FCRA) is a federal law that helps to ensure the accuracy, fairness and privacy of the information in consumer credit bureau files. The law regulates the way credit reporting agencies can collect, access, use and share the data they collect in your consumer reports.

A creditor must disclose a consumer's credit score and information relating to a credit score on a risk-based pricing notice when the score of the consumer to whom the creditor extends credit or whose extension of credit is under review is used in setting the material terms of credit.

The Act (Title VI of the Consumer Credit Protection Act) protects information collected by consumer reporting agencies such as credit bureaus, medical information companies and tenant screening services. Information in a consumer report cannot be provided to anyone who does not have a purpose specified in the Act.

FCRA requirements are related to the Fair Credit Reporting Act (FCRA), which is the primary law regulating how consumer reporting agencies are able to use the personal information of consumers. The FCRA is a federal law first enacted in the 1970s.

A statement indicating that the account "meets FCRA requirements" may be added if a consumer disputes information on their credit report, but the credit bureau determines that the information is accurate. Additionally, it can be concluded that all information is accurate and under federal regulations.

The Fair Credit Reporting Act describes the kind of data that the bureaus are allowed to collect. That includes the person's bill payment history, past loans, and current debts.

Consumer reporting agencies must correct or delete inaccurate, incomplete, or unverifiable information. Inaccurate, incomplete, or unverifiable information must be removed or corrected, usually within 30 days. However, a consumer reporting agency may continue to report information it has verified as accurate.

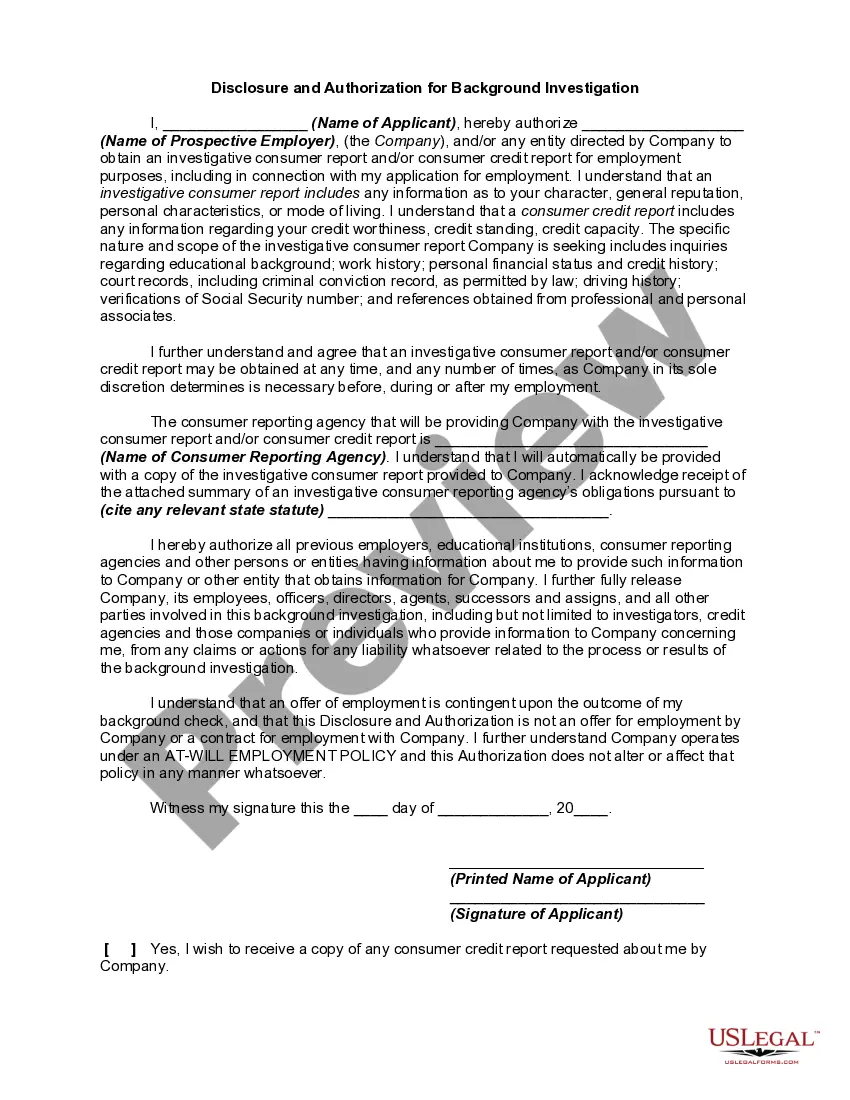

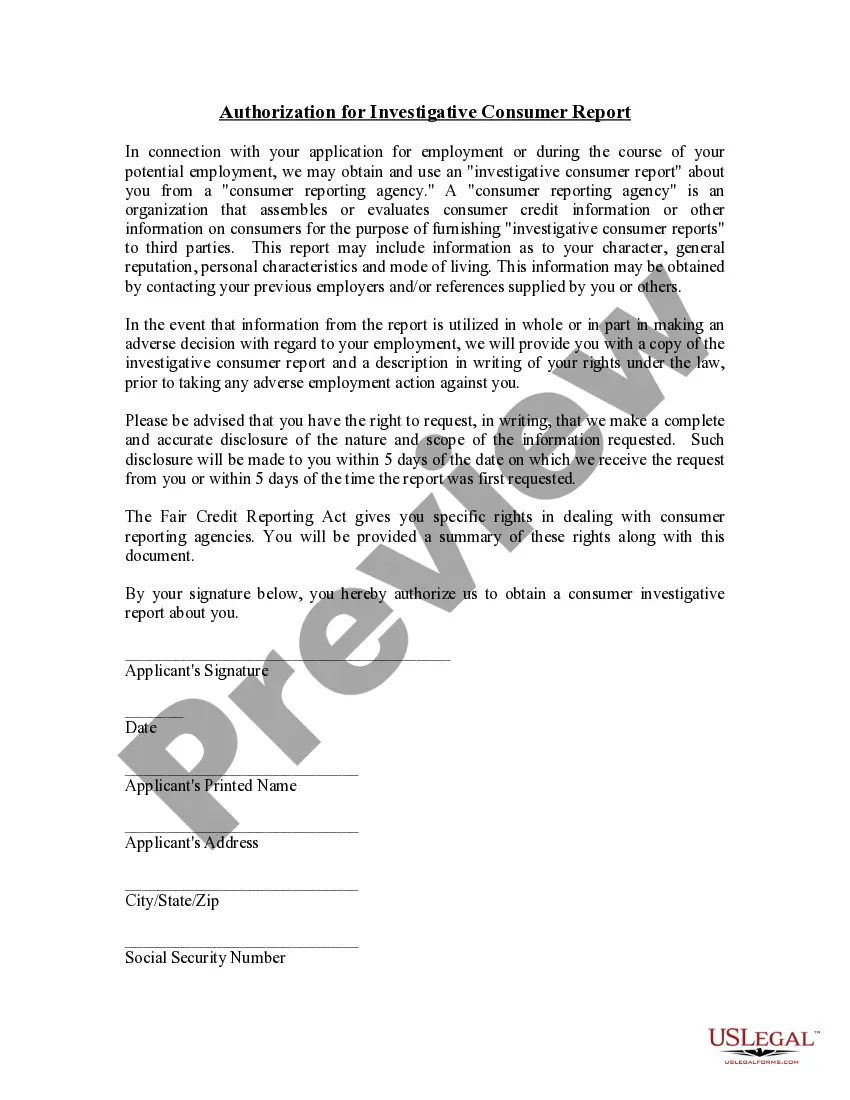

Under the FCRA, an employer may not run a background check on a prospective employee without first providing "a clear and conspicuous disclosure . . . in a document that consists solely of that disclosure, that a consumer report may be obtained for employment purposes." For efficiency, many employers include all