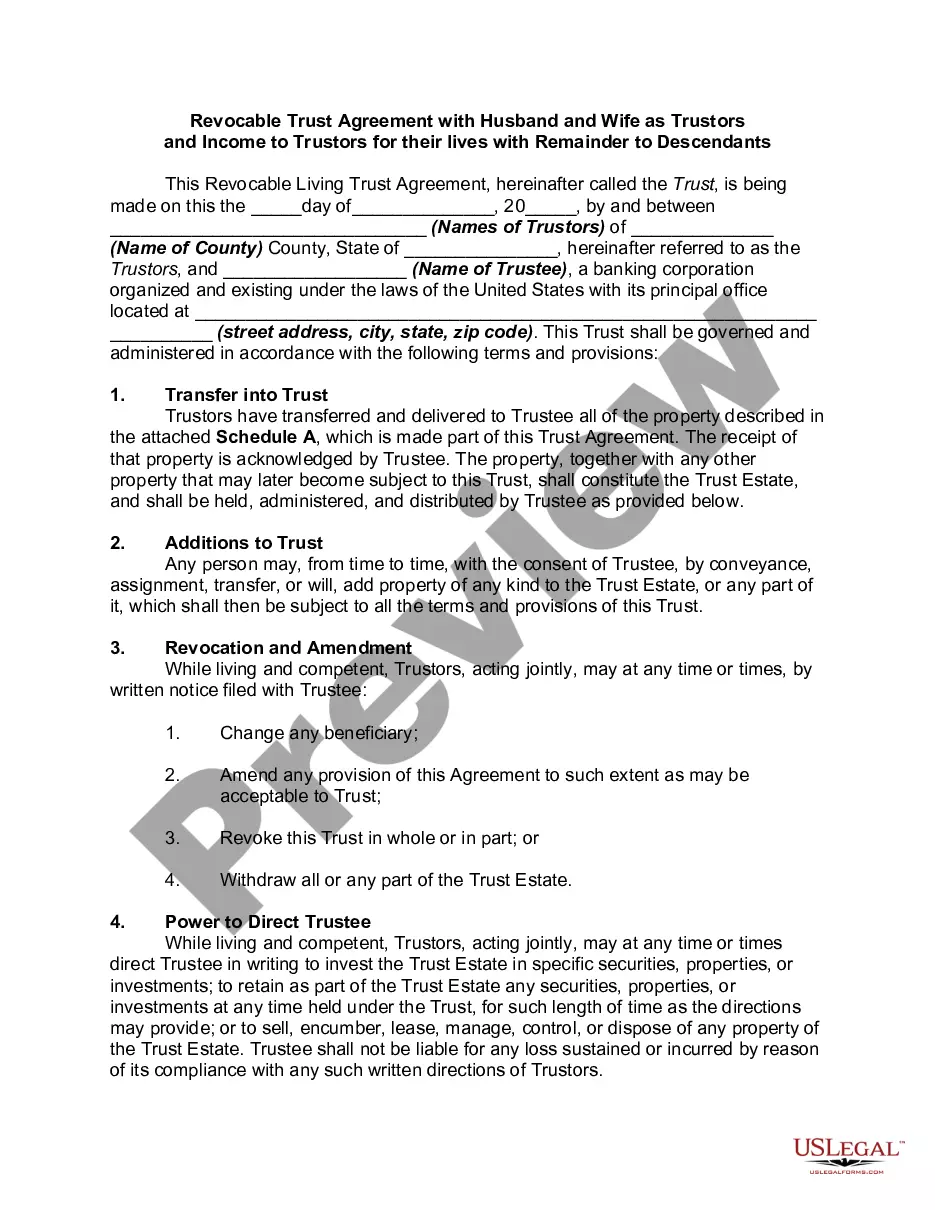

Alabama Joint Trust with Income Payable to Trustors During Joint Lives

Description

How to fill out Joint Trust With Income Payable To Trustors During Joint Lives?

If you need to completely, download, or print legal document templates, utilize US Legal Forms, the premier selection of legal documents, which is accessible online.

Take advantage of the website's straightforward and user-friendly search to locate the documents you require.

Numerous templates for business and personal purposes are categorized by types and states, or keywords.

Step 4. Once you have located the form you need, click the Buy now button. Select the payment plan you prefer and enter your details to register for the account.

Step 5. Complete the purchase. You may use your credit card or PayPal account to finalize the transaction.

- Use US Legal Forms to find the Alabama Joint Trust with Income Payable to Trustors During Joint Lives in a few clicks.

- If you are already a US Legal Forms user, Log In to your account and click the Download button to access the Alabama Joint Trust with Income Payable to Trustors During Joint Lives.

- You can also find forms you have previously downloaded in the My documents section of your account.

- If this is your first time using US Legal Forms, follow these steps.

- Step 1. Ensure you have selected the form for the appropriate region/state.

- Step 2. Use the Review feature to examine the form's details. Remember to read the description.

- Step 3. If you are dissatisfied with the form, utilize the Search field at the top of the page to find other templates from the legal form library.

Form popularity

FAQ

Income earned by the trust can be in the form of interest, dividends, ordinary income, or capital gain. The trust document can allocate which beneficiary is to receive which type of income. Accounting income is used to determine the amount that is required to be distributed to the income beneficiary.

Key TakeawaysTrust beneficiaries must pay taxes on income and other distributions that they receive from the trust. Trust beneficiaries don't have to pay taxes on returned principal from the trust's assets. IRS forms K-1 and 1041 are required for filing tax returns that receive trust disbursements.

After one spouse dies, the surviving spouse is free to amend the terms of the trust document that deal with his or her property, but can't change the parts that determine what happens to the deceased spouse's trust property.

What happens in this type of trust is that the trust is a joint revocable trust when both spouses are alive. When one of the spouses dies, the trust will then split into two trusts automatically. Each trust will have half the assets of the trust along with the separate property of the spouse.

Some of your financial assets need to be owned by your trust and others need to name your trust as the beneficiary. With your day-to-day checking and savings accounts, I always recommend that you own those accounts in the name of your trust.

Joint trusts are also revocable living trusts, set up to hold all of the assets of a married couple and to provide access to the trust assets for both. Typically, at the first death, half of the assets receive a step-up in basis, but all of the assets stay in the trust.

A revocable living trust becomes irrevocable once the sole grantor or dies or becomes mentally incapacitated. If you have a joint trust for you and your spouse, then a portion of the joint trust can become irrevocable when the first spouse dies and will become irrevocable when the last spouse dies.

Assets That Can And Cannot Go Into Revocable TrustsReal estate.Financial accounts.Retirement accounts.Medical savings accounts.Life insurance.Questionable assets.

Under typical circumstances, the surviving spouse would become the sole trustee after the death of one spouse. The surviving spouse would control the shared property, and the personal property of the deceased spouse would be distributed to the beneficiaries.

No Asset Protection A revocable living trust does not protect assets from the reach of creditors. Administrative Work is Needed It takes time and effort to re-title all your assets from individual ownership over to a trust. All assets that are not formally transferred to the trust will have to go through probate.