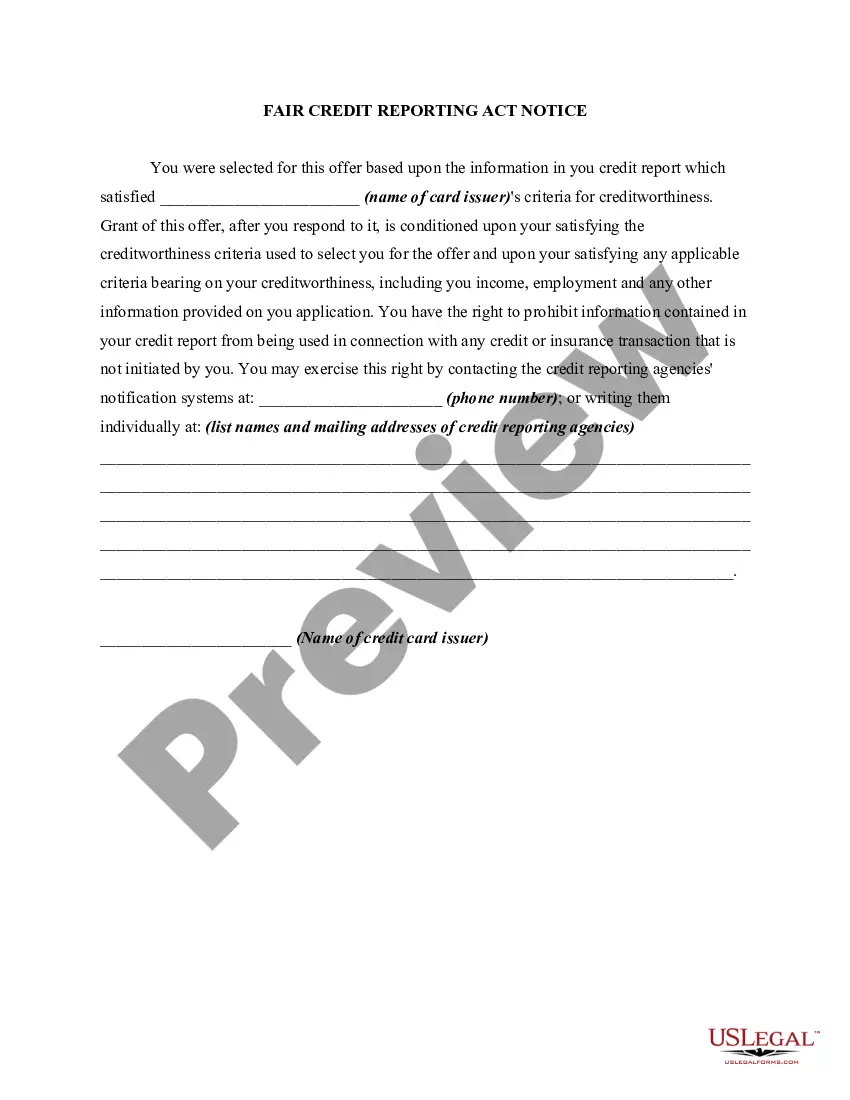

Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information. If such a request is made and is received within 60 days after the consumer learned of the adverse action, the user, within a reasonable period of time, must disclose to the consumer the nature of the information.

Alabama Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency

Description

How to fill out Notice Of Increase In Charge For Credit Based On Information Received From Person Other Than Consumer Reporting Agency?

Are you currently in a place where you need to have files for sometimes enterprise or specific reasons almost every day time? There are plenty of legal record web templates available on the Internet, but discovering types you can trust is not straightforward. US Legal Forms provides a huge number of develop web templates, such as the Alabama Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency, which are published to fulfill state and federal specifications.

Should you be previously knowledgeable about US Legal Forms website and get a merchant account, basically log in. Following that, it is possible to acquire the Alabama Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency design.

If you do not offer an accounts and wish to begin using US Legal Forms, follow these steps:

- Obtain the develop you will need and make sure it is for the appropriate town/area.

- Make use of the Preview button to review the shape.

- Read the description to ensure that you have selected the correct develop.

- In case the develop is not what you are looking for, use the Search field to obtain the develop that suits you and specifications.

- When you find the appropriate develop, click on Get now.

- Pick the rates plan you desire, fill out the required information and facts to create your account, and pay money for an order utilizing your PayPal or bank card.

- Choose a convenient data file structure and acquire your copy.

Find every one of the record web templates you may have bought in the My Forms food selection. You can get a extra copy of Alabama Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency any time, if possible. Just go through the essential develop to acquire or produce the record design.

Use US Legal Forms, by far the most comprehensive variety of legal varieties, to save efforts and steer clear of blunders. The service provides skillfully manufactured legal record web templates that can be used for a variety of reasons. Generate a merchant account on US Legal Forms and begin generating your daily life a little easier.

Form popularity

FAQ

Risk-based pricing occurs when lenders offer different interest rates and loan terms to borrowers, based on individual creditworthiness. The Risk-Based Pricing Rule requires you to notify consumers if they are getting worse terms because of information in their credit report.

Section 623(a) of the FCRA also requires a person who regularly furnishes information to CRAs to promptly notify a CRA if the person determines the previously furnished information is not complete or accurate.

A Credit Score Disclosure alerts a consumer of their FICO scores, defines what a FICO is, informs how FICO scores affect their access to consumer credit and provides contact information for the bureaus.

A creditor must notify the applicant of adverse action within: 30 days after receiving a complete credit application. 30 days after receiving an incomplete credit application. 30 days after taking action on an existing credit account.

A credit score disclosure alerts a consumer about their credit score and other sources of information as required by the Fair Credit Reporting Act (FCRA). The FCRA is a U.S. government legislation that aims to protect consumer information that is collected by consumer reporting agencies or credit bureaus.

The credit file disclosure includes certain information that is not included in a consumer report about you to a third party, such as the inquiries of companies for pre-approved offers of credit or insurance and account reviews, and any medical account information which is suppressed for third party users of consumer ...

RISK-BASED PRICING RULE. Risk-based pricing occurs when lenders offer different interest rates and loan terms to borrowers, based on individual creditworthiness. The Risk-Based Pricing Rule requires you to notify consumers if they are getting worse terms because of information in their credit report.

In the credit score exception notices, creditors are required to disclose the distribution of credit scores among consumers who are scored under the same scoring model that is used to generate the consumer's credit score using the same scale as that of the credit score provided to the consumer.