Alabama Balloon Secured Note Addendum and Rider to Mortgage, Deed of Trust or Security Agreement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Balloon Secured Note Addendum And Rider To Mortgage, Deed Of Trust Or Security Agreement?

US Legal Forms - one of the largest collections of legal documents in the United States - offers a vast selection of legal document templates that you can obtain or create.

By utilizing the website, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords. You can find the latest forms such as the Alabama Balloon Secured Note Addendum and Rider to Mortgage, Deed of Trust or Security Agreement in moments.

If you already have an account, Log In and obtain the Alabama Balloon Secured Note Addendum and Rider to Mortgage, Deed of Trust or Security Agreement from the US Legal Forms library. The Download button will appear on every form you view. You can access all previously downloaded forms in the My documents section of your account.

Complete the transaction. Use your credit card or PayPal account to finalize the transaction. Select the format and download the form to your device.

Make adjustments. Fill out, modify, and print and sign the downloaded Alabama Balloon Secured Note Addendum and Rider to Mortgage, Deed of Trust or Security Agreement. Every template you added to your account has no expiration date and is permanently yours. Therefore, if you wish to obtain or print another copy, simply go to the My documents section and click on the form you need. Access the Alabama Balloon Secured Note Addendum and Rider to Mortgage, Deed of Trust or Security Agreement with US Legal Forms, one of the most extensive collections of legal document templates. Utilize thousands of professional and state-specific templates that meet your business or personal needs and requirements.

- Ensure you have selected the correct form for your city/region.

- Click the Review button to examine the form's content.

- Check the form summary to confirm that you have selected the right form.

- If the form does not meet your needs, use the Search field at the top of the screen to find one that does.

- If you are satisfied with the form, confirm your choice by clicking the Purchase now button.

- Then, select your preferred payment plan and provide your credentials to register for the account.

Form popularity

FAQ

There are also some risks associated with balloon mortgages, including defaulting on the loan if you're unable to make the balloon payment at the end of the loan term. In such cases, your lender will likely take steps to foreclose on your home.

Let's dive into these in detail. Pay in Full: Settle the Balloon Payment. ... Refinancing Options: Managing Balloon Payments. ... Trade-In Route: Alternatives for Balloon Payments. ... Make Extra Payments: Gradually Reduce the Balloon Amount. ... Negotiate with the Lender: Seek Flexible Repayment Terms.

You will end up in foreclosure for inability to pay that last balloon payment. Sometimes, you can refinance your home before the balloon hits, to pay it off, and stay current on your loan. But you may have no idea if, when that time comes, you will have the credit or the equity in the property to do that.

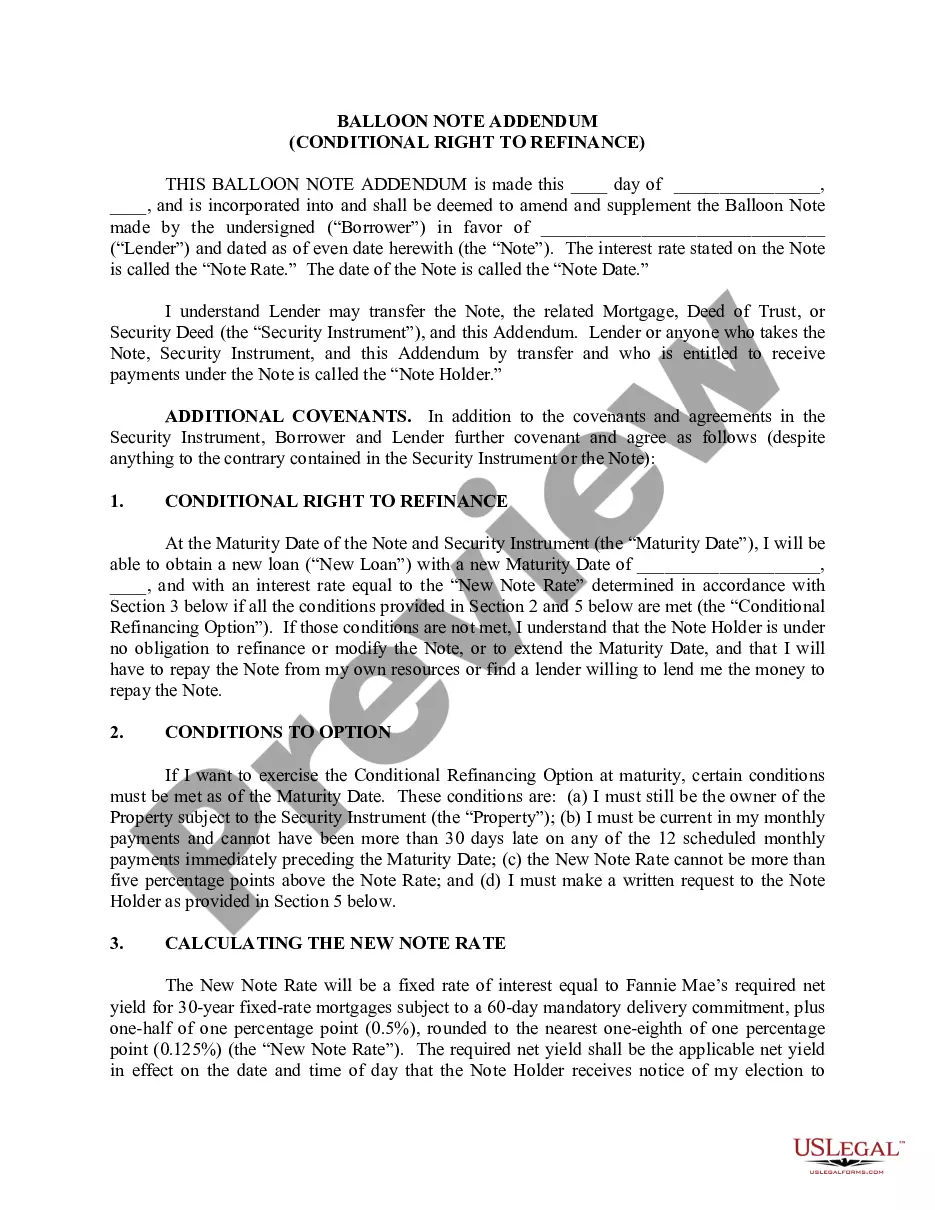

One of the most common ways to handle a balloon payment is to simply refinance the loan. The new loan pays the balloon payment, and you're either left with a fully amortizing loan ? with no balloon involved ? or at least a completely new timeline.

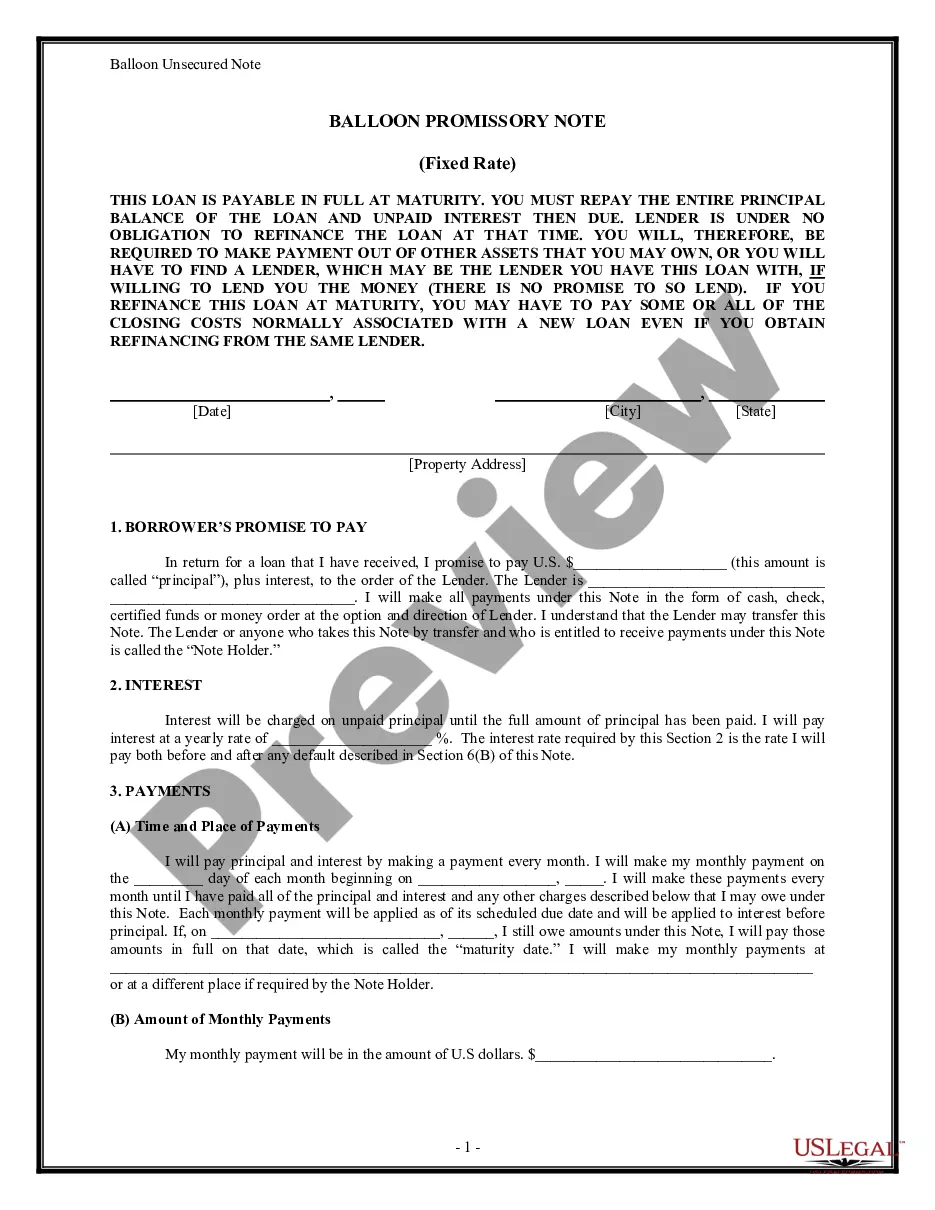

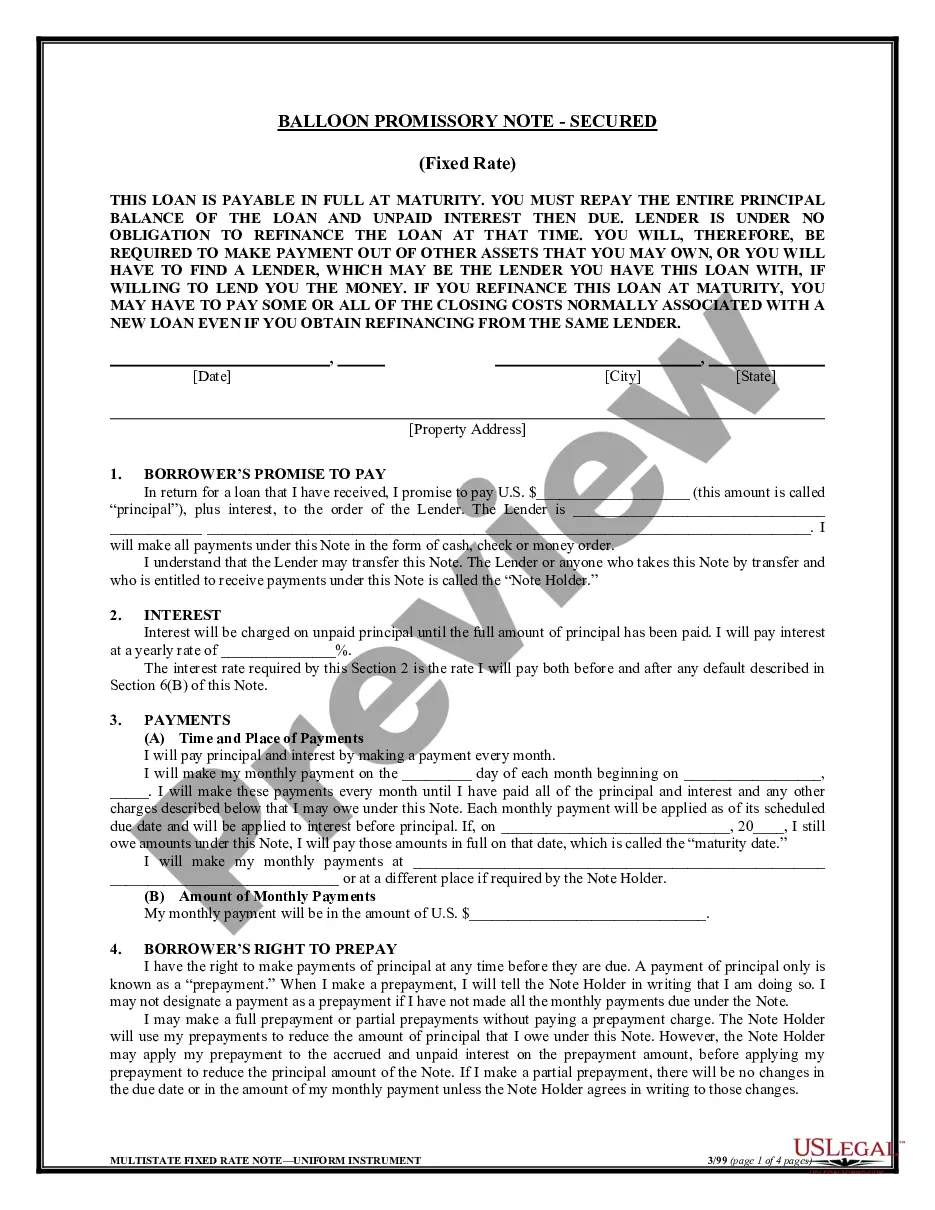

Example of a Balloon Loan Let's say a person takes out a $200,000 mortgage with a seven-year term and a 4.5% interest rate. Their monthly payment for seven years is $1,013. At the end of the seven-year term, they owe a $175,066 balloon payment.

A balloon payment is a larger-than-usual one-time payment at the end of the loan term. If you have a mortgage with a balloon payment, your payments may be lower in the years before the balloon payment comes due, but you could owe a big amount at the end of the loan.

This means making the full balloon payment when the loan matures. Extend the loan. A lender may be able to give you a short-term extension, delaying the date that the loan matures. The extension might be 60 to 180 days.

Borrowers unable to make the balloon payment by the due date can sell the property to avoid defaulting on the loan and potentially facing foreclosure.