Washington Living Trust for Individual Who is Single, Divorced or Widow or Widower with Children

Overview of this form

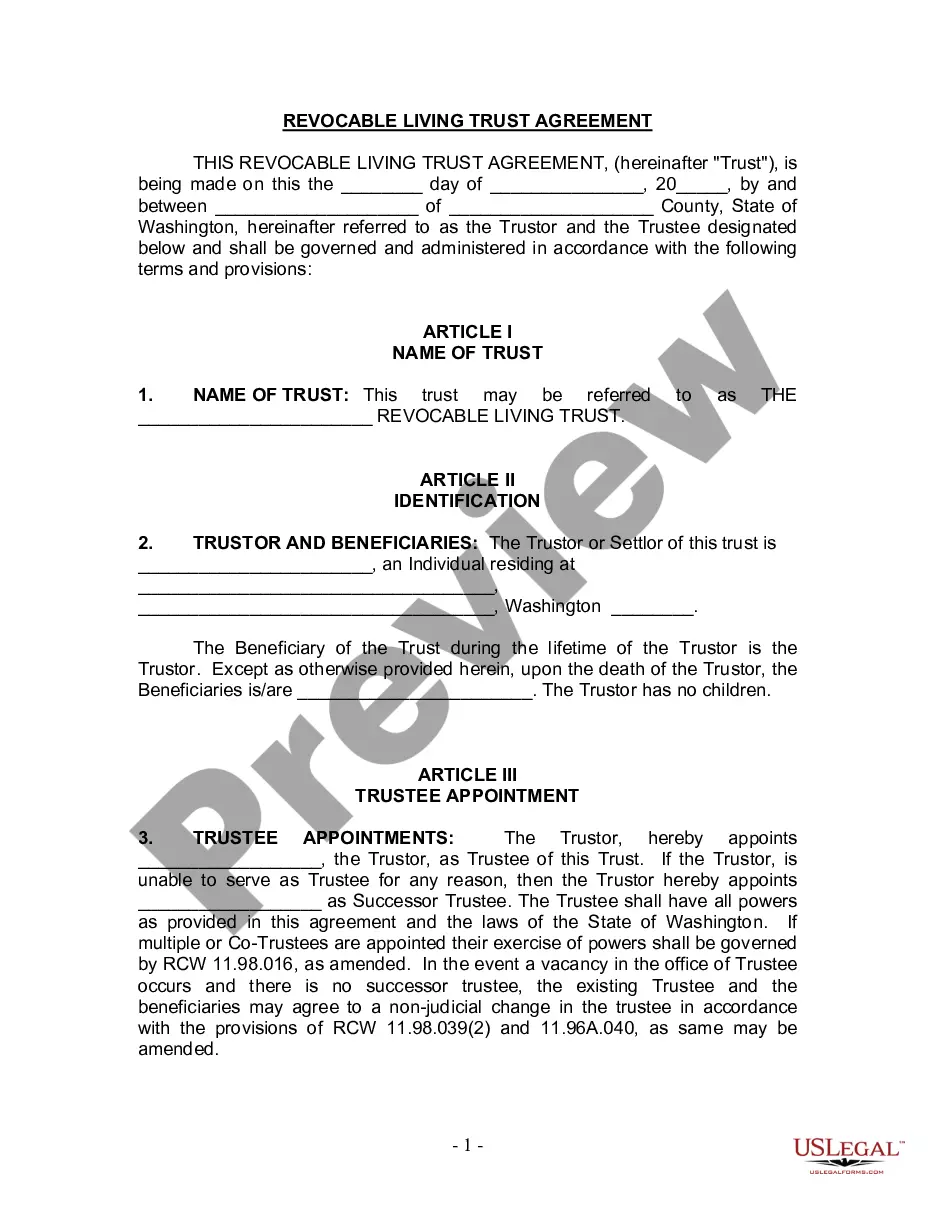

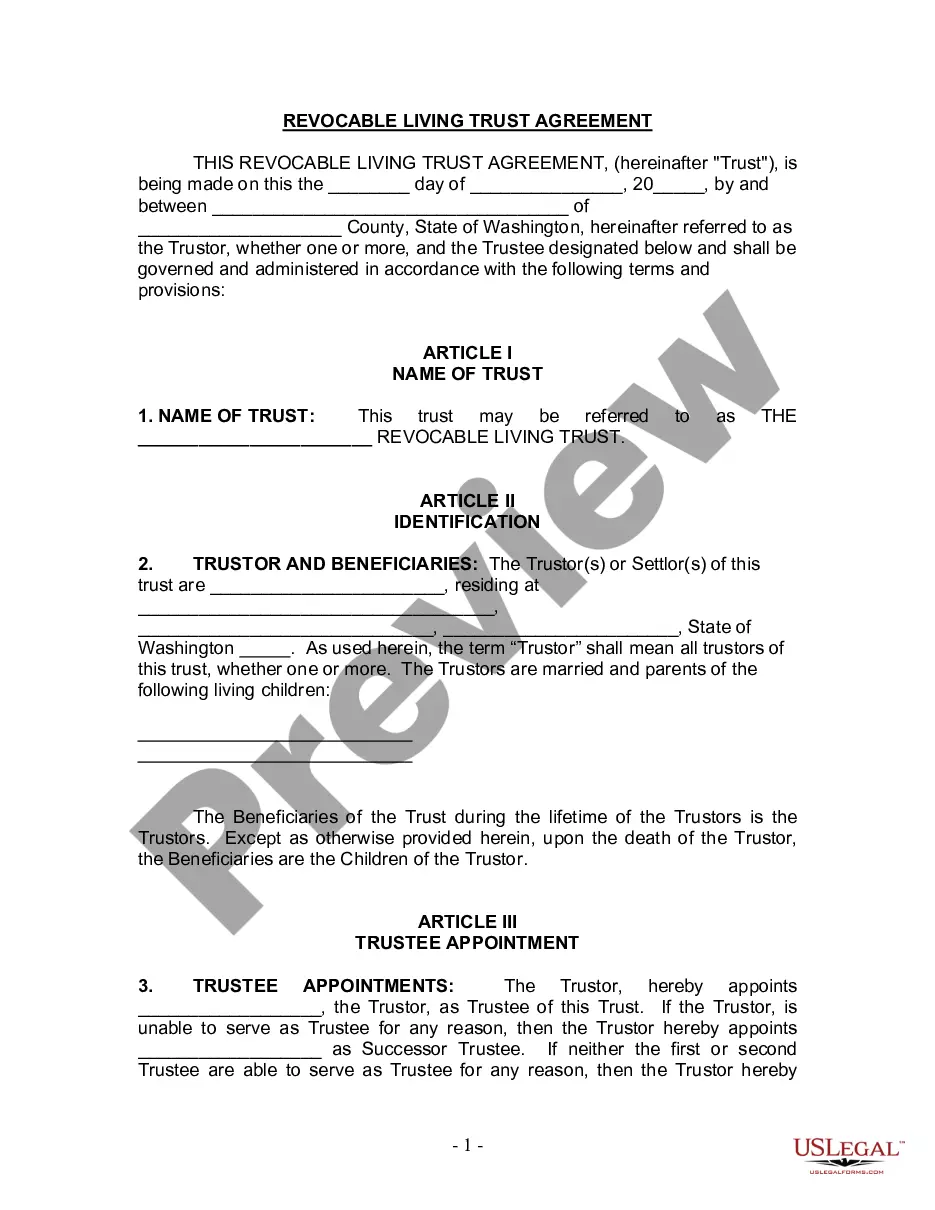

This Living Trust is a legal document designed for individuals who are single, divorced, or widowed and have children. Its primary purpose is to establish a revocable living trust during the individual's lifetime, allowing them to maintain control over their assets while ensuring a smooth transition to their heirs upon death. Unlike wills, this trust avoids probate, simplifying the distribution of assets and managing property through a trustee for the benefit of named beneficiaries.

Key components of this form

- Name of the trust and identifying information about the Trustor.

- Appointment of the Trustee and Successor Trustee provisions.

- Detail of the assets included in the trust and rights associated with them.

- Distribution terms upon the death of the Trustor.

- Powers and responsibilities of the Trustee.

Situations where this form applies

This form is particularly useful when an individual who is single, divorced, or a widow or widower wishes to manage their assets effectively, ensure their children are taken care of, and avoid the complicated probate process after their passing. It is also beneficial when the individual seeks to designate a trusted person to manage and distribute their assets in a manner they specify.

Intended users of this form

- Individuals who are single, divorced, or widowed with children.

- Parents wanting to ensure asset management for their children.

- Individuals seeking to avoid probate and simplify the estate management process.

Instructions for completing this form

- Identify the parties involved by entering the names of the Trustor and Trustee.

- Specify the name of the trust and any additional identifying details.

- List the assets that will be transferred to the trust.

- Designate how the assets will be managed and distributed upon the Trustor's death.

- Have the document signed in front of a notary public if required by state law.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. However, having the trust notarized can enhance its legal standing and ensure its acceptance by third parties.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to list all assets intended for the trust.

- Not updating the trust after major life events, such as marriage, divorce, or the birth of a child.

- Neglecting to appoint a reliable Successor Trustee.

Why use this form online

- Convenient and quick access to legal documents suitable for your needs.

- Editable templates allow for personalized adjustments without the need for a lawyer.

- Reliability of professionally drafted forms to ensure legal compliance.

Legal use & context

- The Living Trust is recognized legally in many jurisdictions and can simplify estate management.

- Setting up a trust can help in asset protection and management, especially for minors.

- Compliance with state laws is essential for the enforceability of this trust.

Main things to remember

- This Living Trust form is ideal for single, divorced, or widowed individuals with children.

- It allows for efficient asset management and avoids the probate process.

- Users should ensure that they comply with their local laws when completing this form.

Looking for another form?

Form popularity

FAQ

A trust is a legal entity that you transfer ownership of your assets to, perhaps in order to decrease the value of your estate or to simplify passing on assets to your intended beneficiaries after you die. An estate planning attorney may charge at least $1,000 to create a trust for you.

How Long to Distribute Trust Assets? Most Trusts take 12 months to 18 months to settle and distribute assets to the beneficiaries and heirs.

There is nothing that says that couple must use a joint revocable trust.When one of the spouses dies, the trust will then split into two trusts automatically. Each trust will have half the assets of the trust along with the separate property of the spouse. The surviving spouse is the trustee over both trusts.

Like a will, a living trust can be altered whenever you wish.After one spouse dies, the surviving spouse is free to amend the terms of the trust document that deal with his or her property, but can't change the parts that determine what happens to the deceased spouse's trust property.

Like a will, a living trust can be altered whenever you wish.After one spouse dies, the surviving spouse is free to amend the terms of the trust document that deal with his or her property, but can't change the parts that determine what happens to the deceased spouse's trust property.

The owner transfers assets into the account during their lifetime. When they pass away, the assets are distributed to beneficiaries, or the individuals they have chosen to receive their assets. A settlor can change or terminate a revocable trust during their lifetime.

Get death certificates. find and file the will with the local probate court. notify the Social Security Administration of the death. notify the state Department of Health. identify the trust beneficiaries. notify the beneficiaries. inventory trust assets. protect trust property.

When they pass away, the assets are distributed to beneficiaries, or the individuals they have chosen to receive their assets. A settlor can change or terminate a revocable trust during their lifetime. Generally, once they die, it becomes irrevocable and is no longer modifiable.

The process of funding your living trust by transferring your assets to the trustee is an important part of what helps your loved ones avoid probate court in the event of your death or incapacity. Qualified retirement accounts such as 401(k)s, 403(b)s, IRAs, and annuities, should not be put in a living trust.