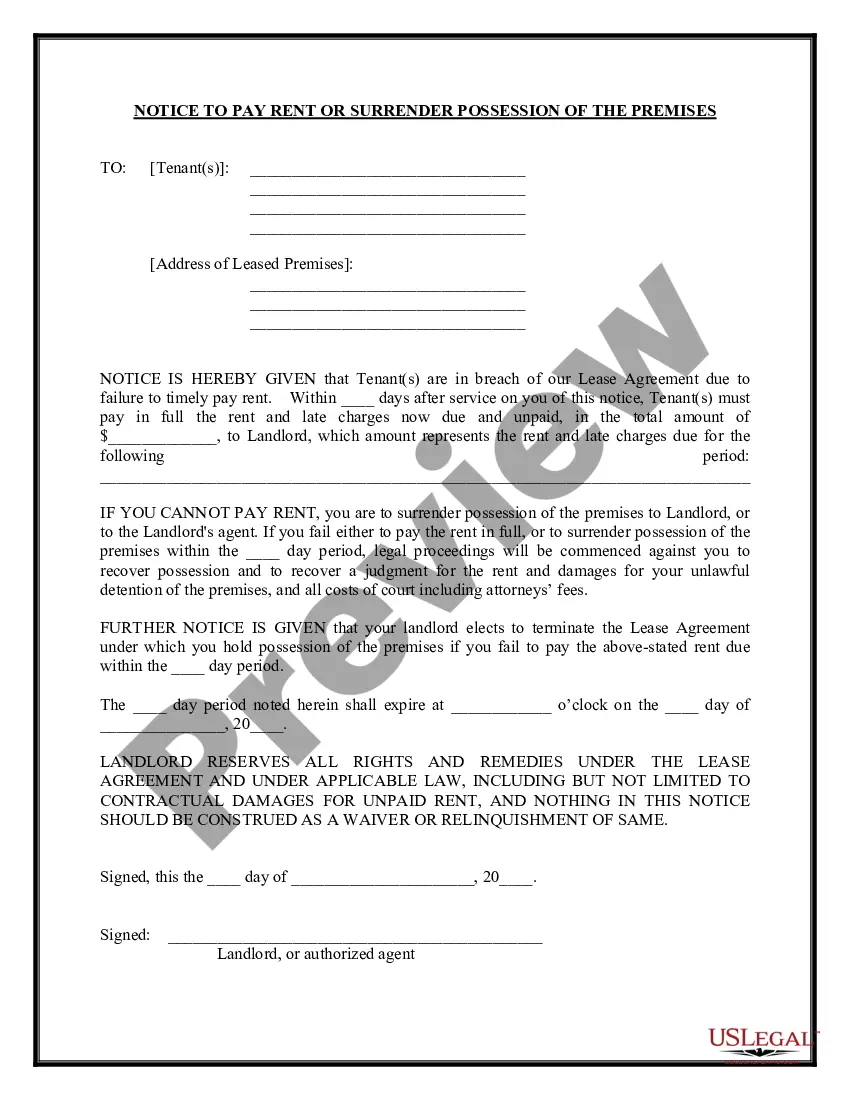

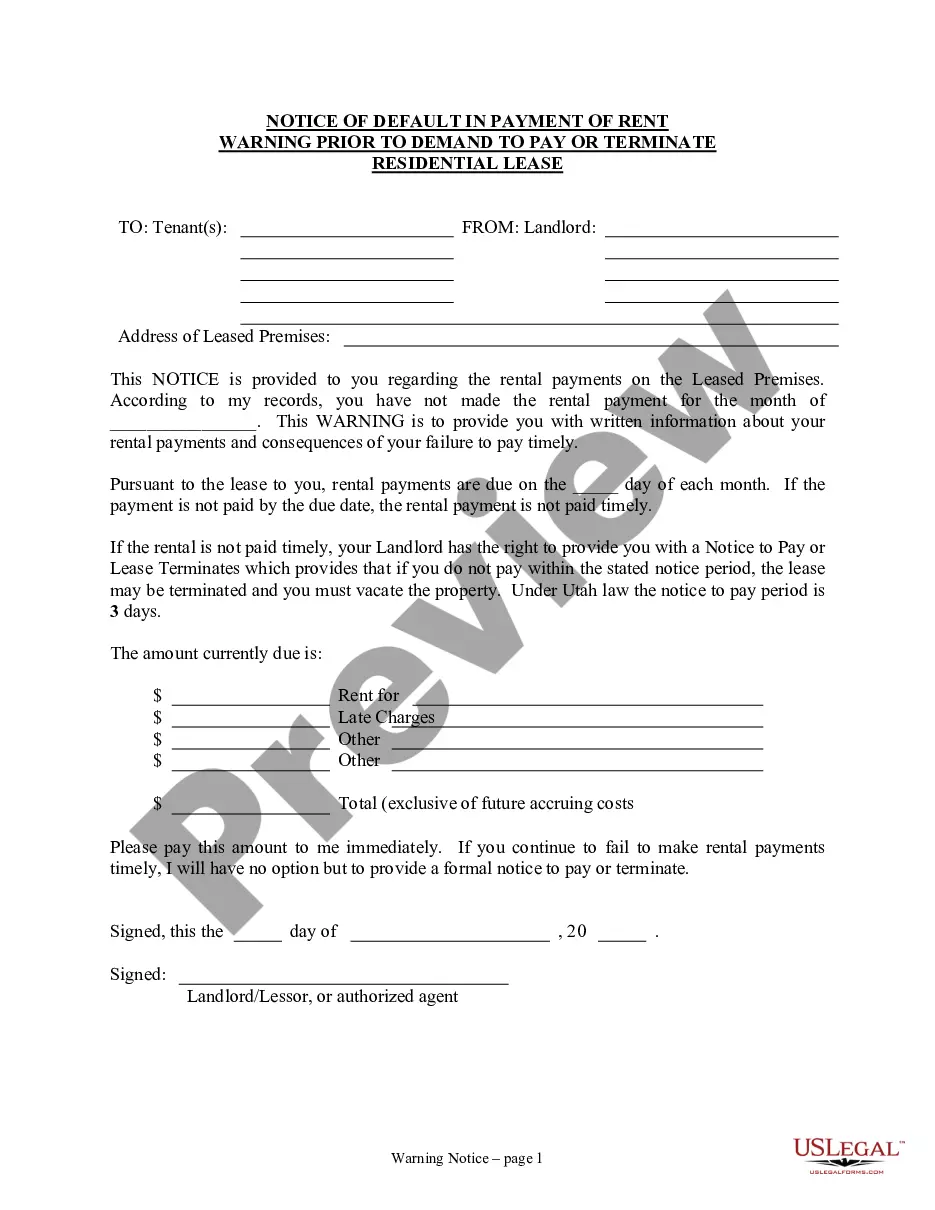

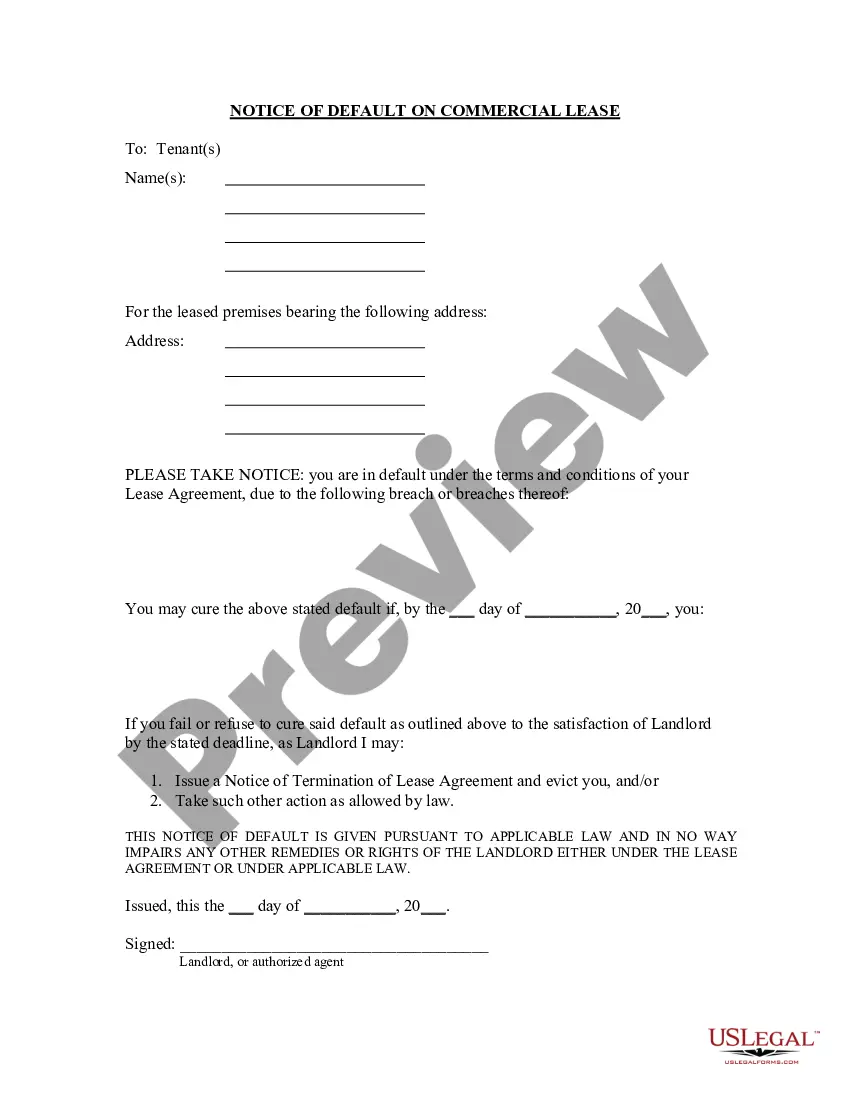

Utah Notice of Default in Payment of Rent as Warning Prior to Demand to Pay or Terminate for Nonresidential or Commercial Property

Understanding this form

This Notice of Default in Payment of Rent as Warning Prior to Demand to Pay or Terminate for Nonresidential or Commercial Property is a crucial document for landlords. It serves as a formal notification to tenants that they have defaulted on their rental payment. This form is specifically designed for non-residential or commercial properties and differs from similar forms used for residential properties. Its primary purpose is to alert the tenant of overdue rent and the consequences that follow, including potential lease termination if payments are not made promptly.

What’s included in this form

- Tenant and landlord information, including names and addresses.

- Details of the due rent amount and payment deadlines.

- Consequences of non-payment, including possible lease termination.

- Proof of delivery options to ensure the notice is officially communicated.

- Signature lines for the landlord or their authorized agent.

When to use this document

This form is essential when a landlord needs to inform a tenant that they are behind on rent payments. It is typically used before issuing a formal demand to pay or terminate the lease. Use this notice when the due rent has not been received by the specified deadline, and you wish to provide the tenant with a warning about the consequences of their late payment.

Who needs this form

- Landlords managing non-residential or commercial properties.

- Property managers acting on behalf of landlords.

- Real estate professionals involved in commercial lease agreements.

Steps to complete this form

- Identify the parties: Fill in the names of the landlord and tenant.

- Specify the property: Provide the address of the leased premises.

- Enter the due date: Indicate the specific month and date of the rent that is overdue.

- Detail the amount due: Clearly state the total rent owed, including any late charges.

- Sign and date the notice: Complete the notice with the landlord's signature and the date of issuance.

Is notarization required?

This form does not typically require notarization unless specified by local law. Always check your state's requirements to ensure legal validity.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to provide accurate tenant information can lead to delivery issues.

- Omitting the specific amount due may cause confusion.

- Not signing the notice can render it invalid.

- Ignoring local laws regarding notice periods specific to your state.

Advantages of online completion

- Convenient access allows for quick preparation and download.

- Editability ensures that you can personalize the notice to fit your situation.

- Reliability from professionally drafted templates ensure compliance with legal standards.

Legal use & context

- This notice acts as a preliminary warning before the eviction process begins.

- It serves as a written record of communication regarding rental arrears.

- Enforcing the terms of the lease agreement helps landlords legally manage tenant behavior.

Summary of main points

- The notice serves as a warning for unpaid rent before legal action.

- Completing the form correctly is crucial for enforcing lease terms.

- Understanding state-specific laws is essential for legal compliance.

Looking for another form?

Form popularity

FAQ

If a borrower falls behind on his mortgage payments, the mortgage lender might file a notice of default, which is an official public notice that the borrower is in arrears. It is one of the initial steps in the foreclosure process.

1Don't ignore the problem.2Contact your lender as soon as you realize that you have a problem.3Open and respond to all mail from your lender.4Know your mortgage rights.5Understand foreclosure prevention options.6Contact a housing counselor.7Prioritize your spending.8Use your assets.Steps to prevent foreclosure - Utah Foreclosure Prevention Taskforce\nwww.utahforeclosureprevention.com > preventforeclosure

The term notice of default refers to a public notice filed with a court that states that the borrower of a mortgage is in default on a loan. The lender may file a notice of default when a mortgagor falls behind on their mortgage payments.

Legally, however, you are not required to vacate your property upon receiving a notice to sell. Depending on the timing of the required notices and previous negotiations with your lender, it can take approximately 120 days to complete a nonjudicial foreclosure.

You can stop the foreclosure process by informing your lender that you will pay off the default amount and extra fees. Your lender would prefer to have the money much more than they would have your home, so unless there are extenuating circumstances, this should work.

After the lender files the Notice of Default, you get 90 days to bring your past-due bill current. After the 90 days pass, the lender files a Notice of Sale with the clerk. The Notice of Sale displays the location, date and time of the sale. It lists the trustee's name and contact information.

The notice of default doesn't affect your credit file, but when the account defaults this will be recorded.If the debt is regulated by the Consumer Credit Act, you must be sent a default notice warning letter and have time to act on it before the default is recorded on your credit file.

Don't ignore the problem. Contact your lender as soon as you realize that you have a problem. Open and respond to all mail from your lender. Know your mortgage rights. Understand foreclosure prevention options. Contact a housing counselor. Prioritize your spending. Use your assets.

A notice of default is the first step to a bank or mortgage lender's foreclosure process.If the mortgage is not paid up to date, the lender will seize the home. A notice of default is also known as a reinstatement period, notice of public auction, or notice of foreclosure.