North Carolina Request that Contracting Body Provide Copy of Payment Bond and Contract Covered by Bond - Individual

About this form

The Request that Contracting Body Provide Copy of Payment Bond and Contract Covered by Bond form is a legal document used by individuals seeking to obtain a copy of a payment bond and the construction contract it covers. This request is typically needed to clarify payment obligations under a contract when legal action may be contemplated. It serves as an official notice to the contracting body to produce these documents within a specified timeframe, and it is distinct from other general contract requests due to its focus on bonding and payment issues specifically.

Main sections of this form

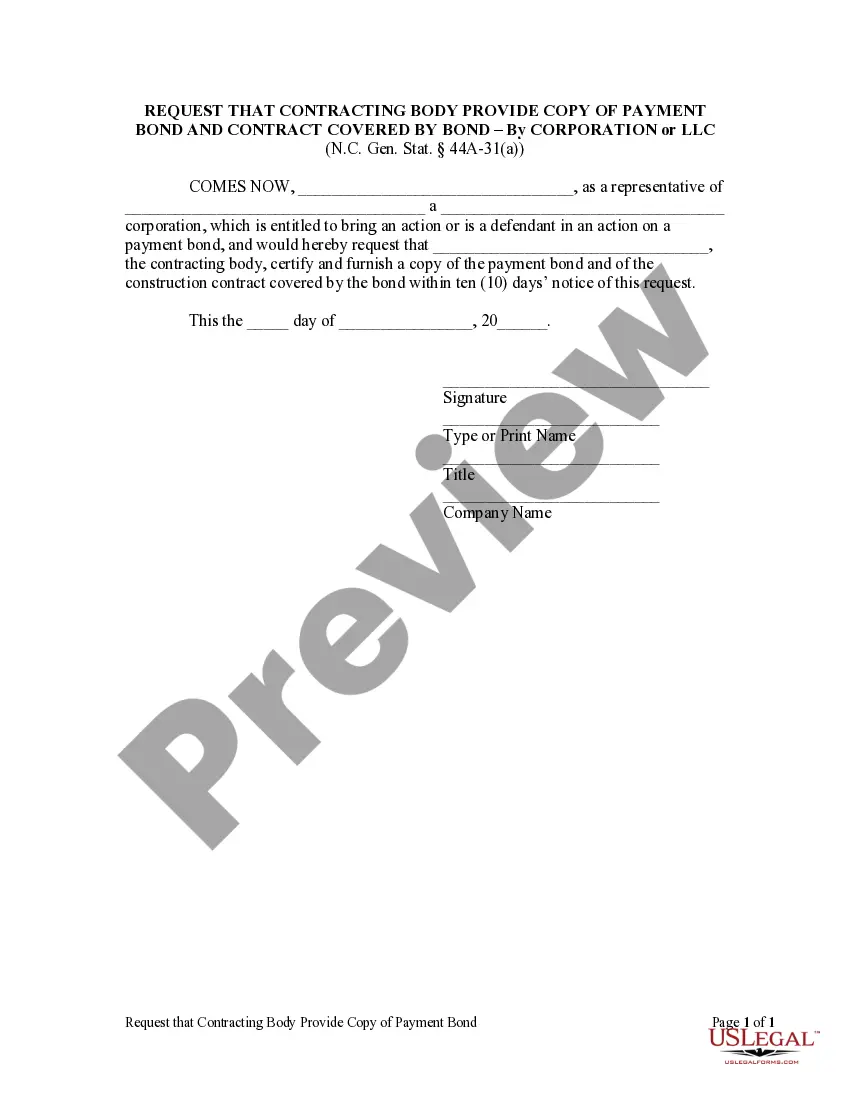

- Requesterâs name and intention to bring or defend an action on a payment bond.

- Name of the contracting body to which the request is directed.

- Specific request for a copy of the payment bond and the construction contract.

- Deadline for the contracting body to respond, set at ten days from the request date.

- Signature line for the requester to validate the request.

- Date section to indicate when the request is made.

When to use this form

This form is essential when an individual is entitled to bring forth a legal action against a contractor or a payment bond issuer. It is particularly relevant in construction disputes where unpaid labor or materials may lead to legal complications. Using this form allows individuals to formally request necessary documentation that supports their claim or defense regarding a payment bond.

Intended users of this form

- Individuals who are entitled to make a claim on a payment bond.

- Defendants in a legal action related to a payment bond.

- Subcontractors or suppliers who need to ensure their payment rights under a construction contract.

- Anyone engaged in a dispute involving construction projects where bonds are involved.

Completing this form step by step

- Enter your name in the space provided as the requester.

- Identify the contracting body you are addressing with your request.

- Clearly specify that you are requesting copies of the payment bond and construction contract.

- Fill in the date when the request is being made.

- Sign the document to validate your request.

- Print your name beneath your signature as required.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. However, it is advisable to check any additional requirements that may apply in your specific jurisdiction to ensure the documentâs effectiveness.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to include all necessary parties' names and contact information.

- Not specifying the correct construction project related to the bond.

- Overlooking the ten-day response deadline in the request.

- Neglecting to sign the document or print your name clearly.

- Not keeping a copy of the request for your records.

Benefits of completing this form online

- Immediate access to download and fill out the form at any time.

- Editable fields allow for easy customization to meet your specific needs.

- Reliable templates drafted by licensed attorneys, ensuring accuracy.

- No need for in-person visits to a lawyer, saving time and resources.

Looking for another form?

Form popularity

FAQ

In the construction industry, the payment bond is usually issued along with the performance bond. The payment bond forms a three-way contract between the Owner, the contractor and the surety, to make sure that all subcontractors, laborers, and material suppliers will be paid leaving the project lien free.

Introduction. A project owner receives a bid bond from a contractor as a part of the supply bidding process. A bid bond provides a guarantee that a winning bidder will take up the contract as per the terms at which they bid. A bid bond ensures compensation to the bond owner if the bidder fails to begin a project.

The contractor who wins the bid is given a contract for the project. A bid bond serves as a guarantee that the contractor who wins the bid will honor the terms of the bid after the contract is signed.A bid bond compensates the owner for the cost difference between the initial contractor's bid and the next-lowest bid.

The surety company will give the Principal (the person who is bonded) a chance to satisfy the claim. If the Principal fails to satisfy the claim, the surety company will step in and satisfy the claim. The surety company will then go to the Principal for repayment of satisfying that claim.

A performance bond is issued to one party of a contract as a guarantee against the failure of the other party to meet obligations specified in the contract.

The Performance Bond secures the contractor's promise to perform the contract in accordance with its terms and conditions, at the agreed upon price, and within the time allowed. The Payment Bond protects certain laborers, material suppliers and subcontractors against nonpayment.

The cost of a performance bond usually is less than 1% of the contract price; however, if the contract is under $1 million, the premium may run between 1% and 2%. Bonds may be more costly, depending upon the credit-worthiness of the contractor. Labor and material payment bonds are companions to the performance bond.

In most cases, a contractor will need to obtain both a payment bond and a performance bond. In these cases, the contractor will often purchase payment and performance bonds together in a so-called P&P bond package. The contractor will apply for a surety bond premium quote through a surety or surety bond broker.