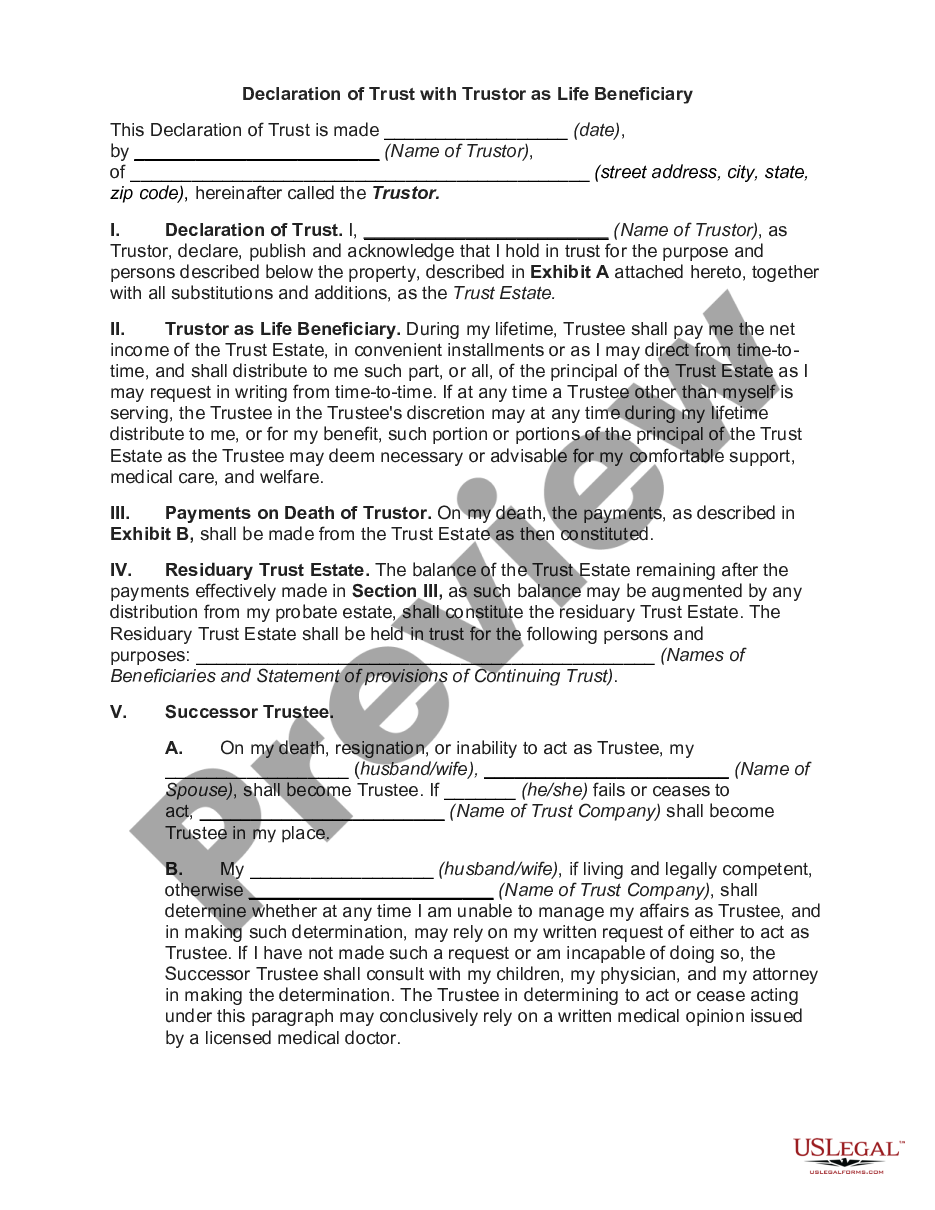

Montana Assignment to Living Trust

About this form

The Assignment to Living Trust form is designed to legally transfer ownership and interest in specific property to a living trust. By using this form, individuals can manage their assets during their lifetime and facilitate estate planning. Unlike wills, this assignment ensures that assets are held within the trust structure, offering benefits such as avoiding probate, providing privacy, and simplifying the transfer of assets upon death.

Form components explained

- Names and addresses of the Assignor and Trustee.

- The name of the living trust and its date of establishment.

- Description of the specific property being assigned to the trust.

- Signatures of the Assignor and the acknowledgment by a notary public.

Situations where this form applies

This form should be used when a property owner wishes to transfer their ownership interest in real estate or other assets to their living trust. It's beneficial when the owner wants to ensure that their assets are managed according to their wishes during their lifetime and are seamlessly transferred to beneficiaries after death. It can also be used when revising estate plans to include new acquisitions or changes in asset distribution wishes.

Who needs this form

This form is intended for:

- Individuals establishing or managing a living trust.

- Property owners who want to simplify their estate planning process.

- Those who are considering transferring specific assets to their trust for better management and distribution.

How to complete this form

- Identify the parties involved: the Assignor(s) and the Trustee.

- Clearly specify the property being transferred to the living trust.

- Enter the date of the assignment and sign the form as the Assignor before a notary public.

- Provide the notary public with the necessary information for acknowledgment, including the date and names.

Does this document require notarization?

Yes, this form must be notarized to be legally valid. This notarization process helps ensure the authenticity of the signatures and the intent of the parties involved. US Legal Forms offers integrated online notarization services, making it easy to complete this requirement securely via video call at your convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to include a complete description of the property being assigned.

- Not signing the form in front of a notary public.

- Omitting the date or any required information about the trust.

Advantages of online completion

- Convenience of downloading the form anytime from anywhere.

- Ability to edit and personalize the form to suit specific needs.

- Reliability of using legally crafted forms designed by licensed attorneys.

Main things to remember

- The Assignment to Living Trust form allows for the transfer of property into a living trust.

- It is essential for effective estate planning to avoid probate.

- Notarization is required for legal validity.

Looking for another form?

Form popularity

FAQ

A revocable living trust isn't subject to the same kind of rules as a will; it should be valid in any state, no matter where you signed it.If you acquire real estate in your new state, you'll probably want to hold it in the trust, so that it doesn't have to go through probate at your death.

Trusts created during your lifetime, known as living trusts, do not go into the public record after you die. With rare exceptions, trusts remain private regardless of whether you have an irrevocable or revocable trust at the time of your death.

Houses and other real estate (even if they're mortgaged) stock, bond, and other security accounts held by brokerages (but think about naming a TOD beneficiary instead) small business interests (stock in a closely held corporation, partnership interests, or limited liability company shares)

No. Trust does not need to be filed in California. Trusts are private documents and usually there are compelling reasons not to file the trust.

Trusts aren't recorded anywhere, so you can't go to the County Recorder's office in the courthouse to ask to see a copy of the trust. However, if real estate is involved, the trust may be recorded in the local office of the county clerk.

Trusts Are Not Public Record. Most states require a last will and testament to be filed with the appropriate state court when the person dies. When this happens, the will becomes a public record for anyone to read. However, trusts aren't recorded.

Pick a type of living trust. If you're married, you'll first need to decide whether you want a single or joint trust. Take stock of your property. Choose a trustee. Draw up the trust document. Sign the trust. Transfer your property to the trust.

To transfer assets such as investments, bank accounts, or stock to your real living trust, you will need to contact the institution and complete a form. You will likely need to provide a certificate of trust as well. You may want to keep your personal checking and savings account out of the trust for ease of use.

Qualified retirement accounts 401ks, IRAs, 403(b)s, qualified annuities. Health saving accounts (HSAs) Medical saving accounts (MSAs) Uniform Transfers to Minors (UTMAs) Uniform Gifts to Minors (UGMAs) Life insurance. Motor vehicles.