Mississippi Living Trust for Husband and Wife with Minor and or Adult Children

Understanding this form

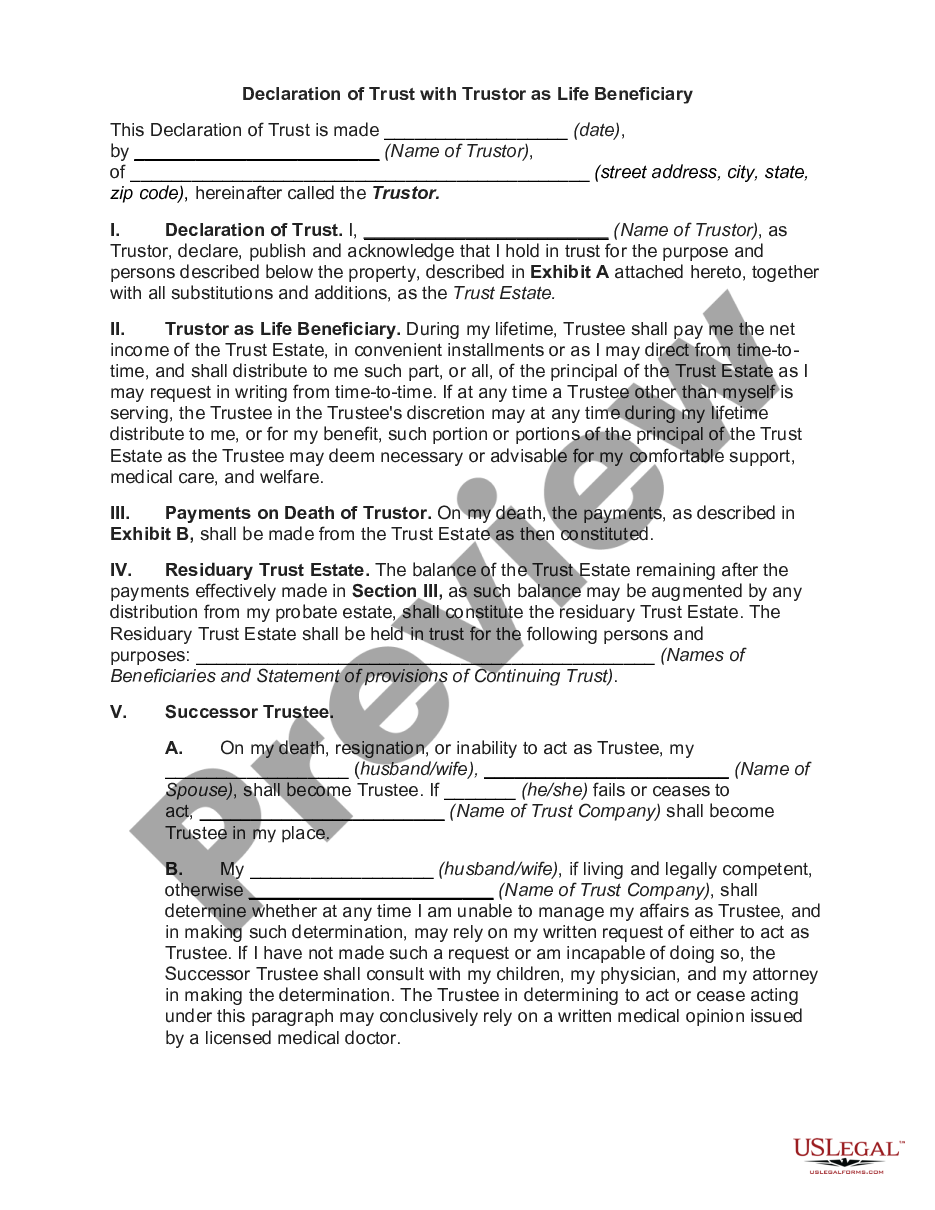

This Living Trust for Husband and Wife with Minor and/or Adult Children is a legal document that creates a revocable living trust during the lifetime of the trustors (typically both spouses). Unlike a will, this trust allows for the management and distribution of assets without going through probate following the trustor's death, providing a smooth transition of property to the designated beneficiaries. It is specifically prepared for use in the state of Mississippi, ensuring compliance with local laws and regulations.

Key parts of this document

- Name of Trust: Identifies the trust by its designated title.

- Trustor and Beneficiaries: Specifies the husband and wife as trustors and outlines the beneficiaries, typically their children.

- Trustee Appointments: Designates the trustee and successor trustees responsible for managing the trust.

- Assets of Trust: Lists the property and assets included in the trust, which can be modified over time.

- Trustee Powers: Outlines the powers granted to the trustee to manage the trust efficiently.

- Distributions: Defines how assets will be distributed upon the death of the trustors.

Situations where this form applies

This form is essential when a married couple wants to ensure their assets are managed and distributed according to their wishes after their death. It is particularly valuable for those with minor children, as it provides a framework for asset allocation and guardianship if needed. Additionally, it helps avoid the lengthy and costly probate process, thereby streamlining estate management.

Who should use this form

- Married couples looking to create an estate plan.

- Individuals who wish to avoid probate for their assets.

- Parents with minor or adult children who want to manage asset distribution.

- Couples who want flexibility to amend their estate plan over time.

Instructions for completing this form

- Identify the parties: Enter the names of the husband and wife acting as trustors.

- Designate the trustee: Specify who will manage the trust assets, including potential successor trustees.

- List the trust assets: Detail the properties and assets that will be held in the trust.

- Outline the distribution plan: Clarify how and when the assets will be distributed upon the trustors' death.

- Sign the document: Both trustors must sign in the presence of a notary public to validate the trust.

Notarization guidance

Yes, this form must be notarized to be legally valid. US Legal Forms offers integrated online notarization services that are available 24/7. This ensures a secure and efficient process without the need for travel.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to update the trust after significant life events, such as the birth of a child or changes in financial status.

- Not listing all significant assets, which can lead to disputes or confusion later on.

- Neglecting to appoint successor trustees, leaving the trust unmanageable if the primary trustee cannot serve.

- Not having the document notarized, which may be required for legitimacy.

Why complete this form online

- Convenience: Complete the form from the comfort of your home at any time.

- Editability: Easily modify the document as circumstances change.

- Reliability: Access a template created by licensed attorneys to ensure legal compliance.

Summary of main points

- A living trust simplifies the transfer of assets upon death and avoids probate.

- It's essential for married couples with minor or adult children to ensure their wishes are followed regarding asset distribution.

- Properly complete and notarize the trust to ensure it is legally enforceable.

Looking for another form?

Form popularity

FAQ

You don't need to include all your accounts in a revocable trust for your heirs to bypass the probate process, notably retirement accounts with designated beneficiaries and investment accounts that have transfer-on-death provisions.

Cash Accounts. Rafe Swan / Getty Images. Non-Retirement Investment and Brokerage Accounts. Non-qualified Annuities. Stocks and Bonds Held in Certificate Form. Tangible Personal Property. Business Interests. Life Insurance. Monies Owed to You.

The process of funding your living trust by transferring your assets to the trustee is an important part of what helps your loved ones avoid probate court in the event of your death or incapacity. Qualified retirement accounts such as 401(k)s, 403(b)s, IRAs, and annuities, should not be put in a living trust.

Yes you can set up a trust independent of your husband. You could fund the trust with your personal property now and/or designate any community property that is yours at the time of your death to pour over into the trust.

Qualified retirement accounts 401ks, IRAs, 403(b)s, qualified annuities. Health saving accounts (HSAs) Medical saving accounts (MSAs) Uniform Transfers to Minors (UTMAs) Uniform Gifts to Minors (UGMAs) Life insurance. Motor vehicles.

Property you put in a living trust doesn't have to go through probate, which means that the assets won't get tied up in court for months and maybe years. However, you don't have to put bank accounts in a living trust, and sometimes it's not a good idea.

One type of trust that will protect your assets from your creditors is called an irrevocable trust. Once you establish an irrevocable trust, you no longer legally own the assets you used to fund it and can no longer control how those assets are distributed.

Houses and other real estate (even if they're mortgaged) stock, bond, and other security accounts held by brokerages (but think about naming a TOD beneficiary instead) small business interests (stock in a closely held corporation, partnership interests, or limited liability company shares)

You can put your real estate into your living trust even if owe money on it. A loan on the property -- like a mortgage or deed of trust -- will follow the property into the trust, and it will also follow the property to the beneficiary.