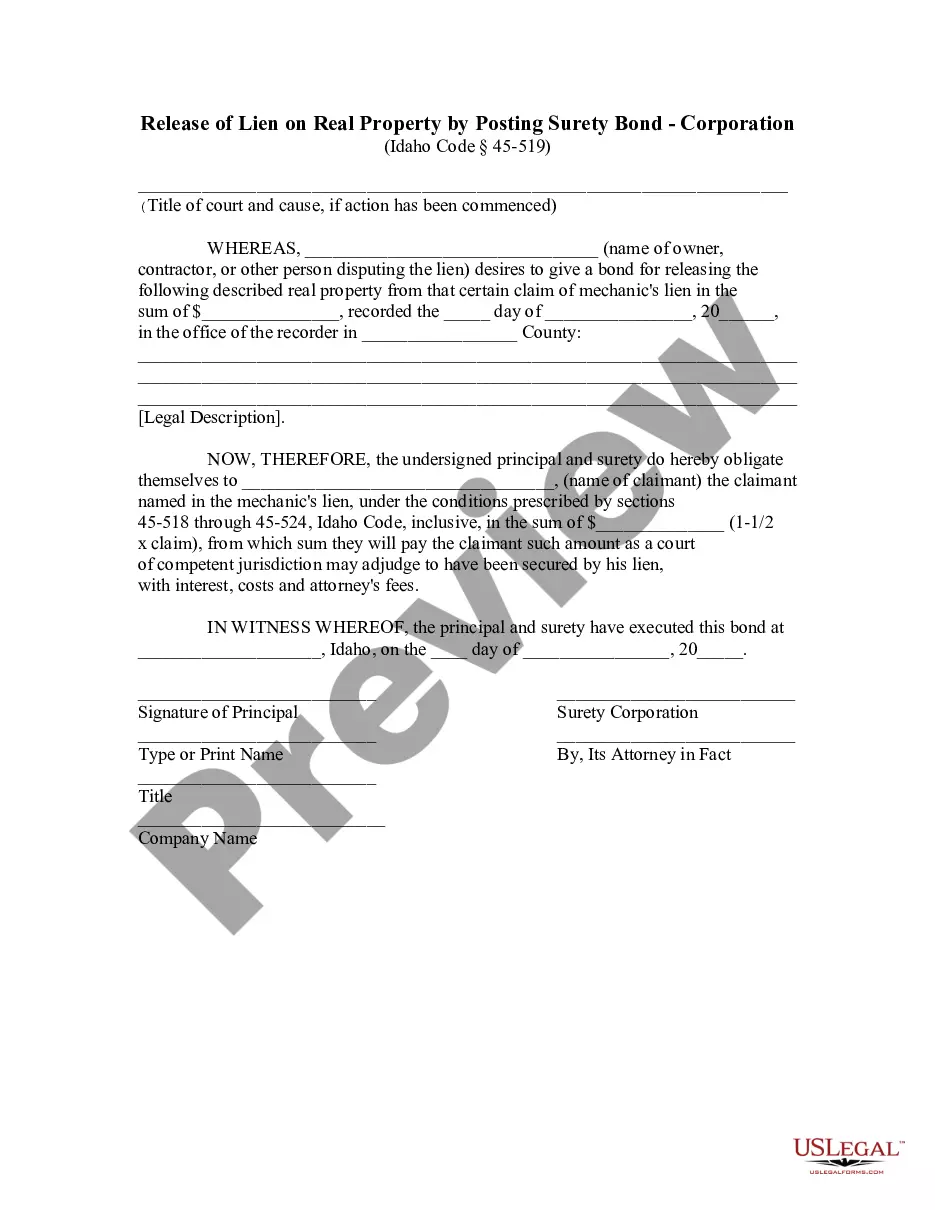

Idaho Release of Lien by Posting of Surety Bond - Individual

Overview of this form

The Release of Lien by Posting of Surety Bond - Individual is a legal document used in Idaho to release a mechanics lien on real property. This form is essential for individuals or entities looking to secure a property while disputing a claim against it. Unlike other lien release methods, this form specifically requires the posting of a surety bond, ensuring the claimant can be compensated if the court rules in their favor. Utilizing this form allows parties to challenge a lien without the burden of inaction on the property in question.

Key parts of this document

- Title of court and cause of action, if applicable

- Name of the party disputing the lien

- Description of the property with a legal description

- Details of the surety bond amount and conditions

- Signatures of the principal and surety corporation

- Notary acknowledgment for validation

When this form is needed

This form should be utilized when a property owner or contractor disputes a mechanics lien and wishes to have the lien released by posting a surety bond. Situations may include construction disputes where a contractor has filed a lien for unpaid work. By completing and filing this form, the disputing party can legally release the lien while ensuring compliance with Idaho law.

Who can use this document

- Property owners seeking to challenge a mechanics lien

- Contractors or individuals involved in construction projects with lien disputes

- Legal representatives handling lien-related issues

Instructions for completing this form

- Identify the court and enter the cause of action if a legal action has been commenced.

- Complete the name of the owner or contractor disputing the lien.

- Provide a detailed legal description of the property and the amount of the mechanics lien.

- State the name of the claimant and the sum of the surety bond.

- Ensure signatures are provided from both the principal and the surety representative.

- Obtain notarization to validate the document.

Does this document require notarization?

Yes, this form must be notarized to be legally valid in Idaho. The notary public serves to verify the identities of the individuals signing the bond, ensuring compliance with legal standards. US Legal Forms offers integrated online notarization services, which are available 24/7 for convenient access and secure processing.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to include a complete legal description of the property.

- Not accurately stating the name of the claimant.

- Omitting necessary signatures or notary acknowledgment.

- Incorrectly calculating the surety bond amount.

Why complete this form online

- Immediate access to the form allows for prompt action in legal disputes.

- Editable templates ensure that the form can be tailored to specific needs.

- Reliability of the document as it is drafted by licensed attorneys.

- Convenience of downloading and printing from the comfort of home.

Key takeaways

- This form is used to release a mechanics lien in Idaho by posting a surety bond.

- Proper completion involves accurate information and signatures from all parties involved.

- Notarization is required for the form to be legally binding.

- Using US Legal Forms provides a secure, convenient, and reliable resource for legal documentation.

Looking for another form?

Form popularity

FAQ

A bond for a $100,000 contract will typically cost $500 to $2,000. Get a free Performance Bond quote.

A surety bond is a promise to be liable for the debt, default, or failure of another. It is a three-party contract by which one party (the surety) guarantees the performance or obligations of a second party (the principal) to a third party (the obligee).

The state of California requires every Notary to purchase a $15,000 Surety Bond in order to protect the public financially from the possibility of a negligent mistake or intentional misconduct.

At its simplest, a surety bond requires the surety to pay a set amount of money to the obligee if a principal fails to perform a contractual obligation. It also helps principals, typically small contractors, compete for contracts by reassuring customers that they will receive the product or service promised.

When it comes to surety bonds, you will not need to pay month-to-month. In fact, when you get a quote for a surety bond, the quote is a one-time payment quote. This means you will only need to pay it one time (not every month).Most bonds are quoted at a 1-year term, but some are quoted at a 2-year or 3-year term.

Nevada law requires all Notaries to purchase and maintain a $10,000 Notary surety bond for the duration of their 4-year commission. The Notary bond protects the general public of Nevada against any financial loss due to improper conduct by a Nevada Notary. The bond is NOT insurance protection for Nevada Notaries.

This is one way a surety bond differs from an insurance policy. While an insurance company does not expect to be paid back for a claim, a surety company does.You are also responsible for paying back the surety company every penny they pay out on a claim, including all costs associated with the claim.

A surety bond is a promise to be liable for the debt, default, or failure of another. It is a three-party contract by which one party (the surety) guarantees the performance or obligations of a second party (the principal) to a third party (the obligee).