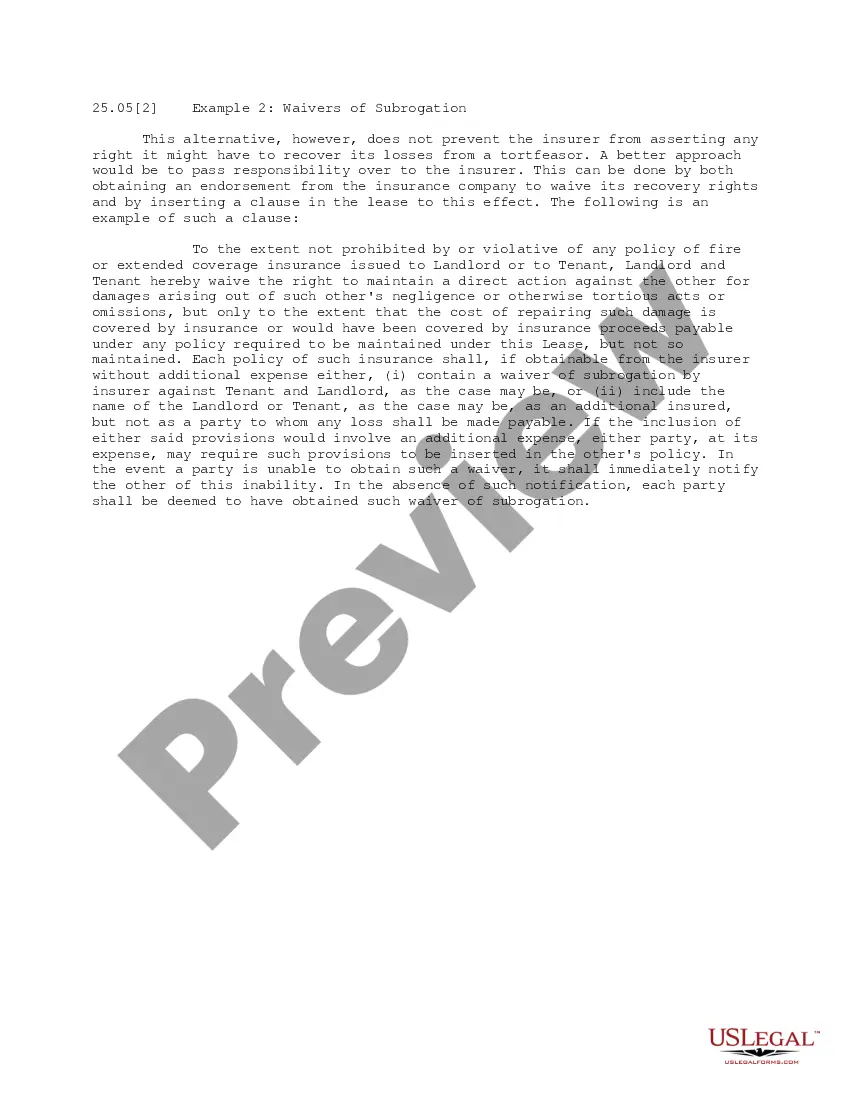

This office lease form does not prevent the insurer from asserting any right it might have to recover its losses from a tortfeasor. A better way to approach this can be done by both obtaining an endorsement from the insurance company to waive its recovery rights and by inserting a clause in the lease to this effect.

Waiver Of Subrogation For Additional Insured

Category:

State:

Multi-State

Control #:

US-OL25052

Format:

Word;

PDF

Instant download

Description

Form popularity

FAQ

When writing a subrogation demand letter, begin by clearly identifying both parties involved, along with relevant policy information. State the facts of the loss in an organized manner, and explicitly reference the waiver of subrogation for additional insured when applicable. Conclude by requesting specific compensation and providing a deadline for response. This structured approach enhances clarity and encourages prompt attention to your demand.

Yes, if you are an additional insured, having a waiver of subrogation is often advisable. This waiver protects you from any claims your primary insured might pursue against you in the event of a loss. By securing this waiver, you can create a safer working environment and minimize potential litigation. It's an essential tool in risk management and fosters better relationships with other parties involved.

Adding a waiver of subrogation for additional insured status involves incorporating the clause into your contracts or insurance policies. Consult with your insurance agent or legal advisor to draft the necessary documentation. This can include specific wording that addresses the waiver creatively. It is crucial to ensure that all parties involved acknowledge and accept this addition.

To obtain a waiver of subrogation for additional insured status, you need to request it from your insurance provider or include it in your insurance policy. Make sure to clearly state your intention to waive subrogation in your contracts and agreements. This approach typically involves negotiating terms with your insurer. Once finalized, your insurance documents will reflect this waiver.

To avoid subrogation, you should use a waiver of subrogation for additional insured status in your contracts. This agreement prevents your insurance company from seeking reimbursement from another party after a claim. By including this waiver, you protect your relationship with other involved parties and streamline the claims process. Proper legal documentation ensures clarity and reduces future disputes.

Filling out a subrogation letter involves providing specific details about the incident and the involved parties. Start by clearly stating the purpose of the letter, which is related to the waiver of subrogation for additional insured. Include all essential information, such as dates, locations, and descriptions of the event. Consider using US Legal Forms to access templates and guidance, ensuring that your letter meets legal standards and conveys your intent effectively.

An additional insured can file a claim against the insured under certain conditions. If the additional insured suffers a loss that falls under the coverage of the insurance policy, they may have a right to claim. However, whether they can pursue a claim depends on the terms of the specific insurance policy and any waivers in place. Consulting a legal resource like US Legal Forms can provide clarity on how a waiver of subrogation for additional insured impacts possible claims.

A waiver of subrogation is typically necessary for parties involved in contracts such as construction, leasing, or service agreements where liability risks exist. It is crucial for any business seeking to protect themselves while working with subcontractors or other parties. Additionally, lenders and property owners often require it to avoid legal entanglements. By utilizing a waiver of subrogation for additional insured, you can further minimize risk exposure.

No, additional insured status and a waiver of subrogation are distinct concepts. An additional insured designation provides protection under the insurance policy to another party, while a waiver of subrogation for additional insured means that the insurer relinquishes the right to seek recovery from third parties. Understanding both terms is crucial for proper risk management in contractual agreements.

A waiver of subrogation can generally be categorized into two versions: a blanket waiver and a specific waiver. A blanket waiver of subrogation for additional insured extends coverage to all parties involved under a specified contract. In contrast, a specific waiver applies only to clearly defined situations or designated parties. Understanding these differences helps you determine which version best fits your insurance needs.