Distribution Agreement Form Withdrawal

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

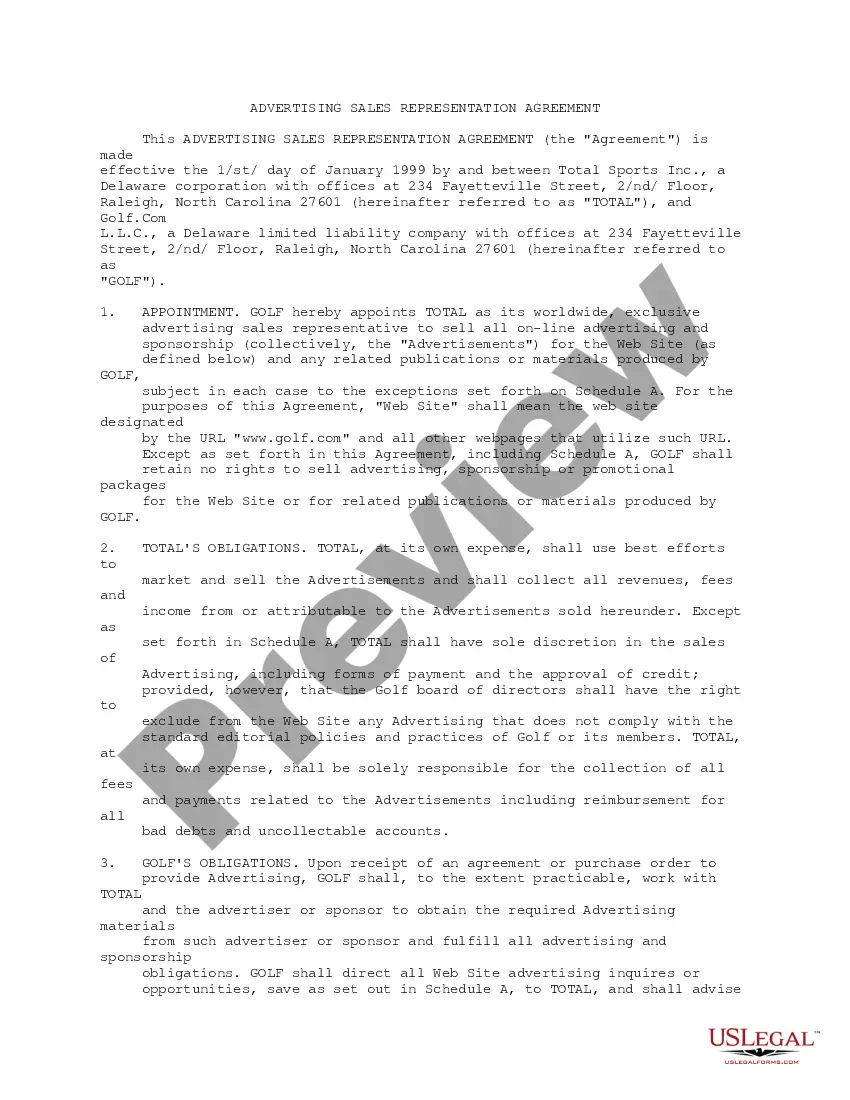

How to fill out Marketing And Distribution Agreement Between Publishers Group West, Inc. And Total Sports, Inc.?

There's no longer a reason to squander time searching for legal documents to meet your local state provisions.

US Legal Forms has gathered all of them in one location and made their access easier.

Our platform provides over 85k templates for various business and personal legal situations categorized by state and usage area.

Utilize the search bar above to discover another template if the earlier one was not satisfactory. Select Buy Now beside the template title when you identify the correct one. Choose the most appropriate pricing plan and create an account or Log In. Complete your subscription payment with a credit card or via PayPal to proceed. Select the file format for your Distribution Agreement Form Withdrawal and download it to your device. Print the form to fill it out manually or upload the template if you prefer to edit it online. Preparing legal documents under federal and state laws and regulations is quick and easy with our collection. Try US Legal Forms now to maintain your documentation in order!

- All forms are suitably crafted and validated for accuracy, so you can trust in receiving an up-to-date Distribution Agreement Form Withdrawal.

- If you are acquainted with our service and already possess an account, ensure your subscription is active before retrieving any templates.

- Log In to your account, select the document, and click Download.

- You can also revisit all obtained documents whenever necessary by selecting the My documents tab in your profile.

- If you have not interacted with our service previously, the procedure will require additional steps to finalize.

- Here's how new users can find the Distribution Agreement Form Withdrawal in our catalog.

- Examine the page content thoroughly to confirm it includes the sample you need.

- To assist, use the form description and preview options if available.

Form popularity

FAQ

You can use your yearly contribution to your traditional IRA to reduce your current taxes since it can be directly subtracted from your income. Then, you can use what you deposited into your Roth IRA as access to have tax-free income in retirement.

You can take your annual RMD in a lump sum or piecemeal, perhaps in monthly or quarterly payments. Delaying the RMD until year-end, however, gives your money more time to grow tax-deferred. Either way, be sure to withdraw the total amount by the deadline.

Regardless of your age, you will need to file a Form 1040 and show the amount of the IRA withdrawal. Since you took the withdrawal before you reached age 59 1/2, unless you met one of the exceptions, you will need to pay an additional 10% tax on early distributions on your Form 1040.

There is no longer an RMD waiver for 2021. As a result, anyone age 72 or older as of December 31, 2021, must take their RMD by year-end to avoid the 50% penalty2015unless this is their first RMD, in which case they have until April 1, 2022.

Key Takeaways Any earnings you withdraw are considered qualified distributions if you're 59½ or older, and the account is at least five years old, making them tax- and penalty-free. Other kinds of withdrawals are considered non-qualified and can result in both taxes and penalties.