Improvement Lease Withdrawal

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

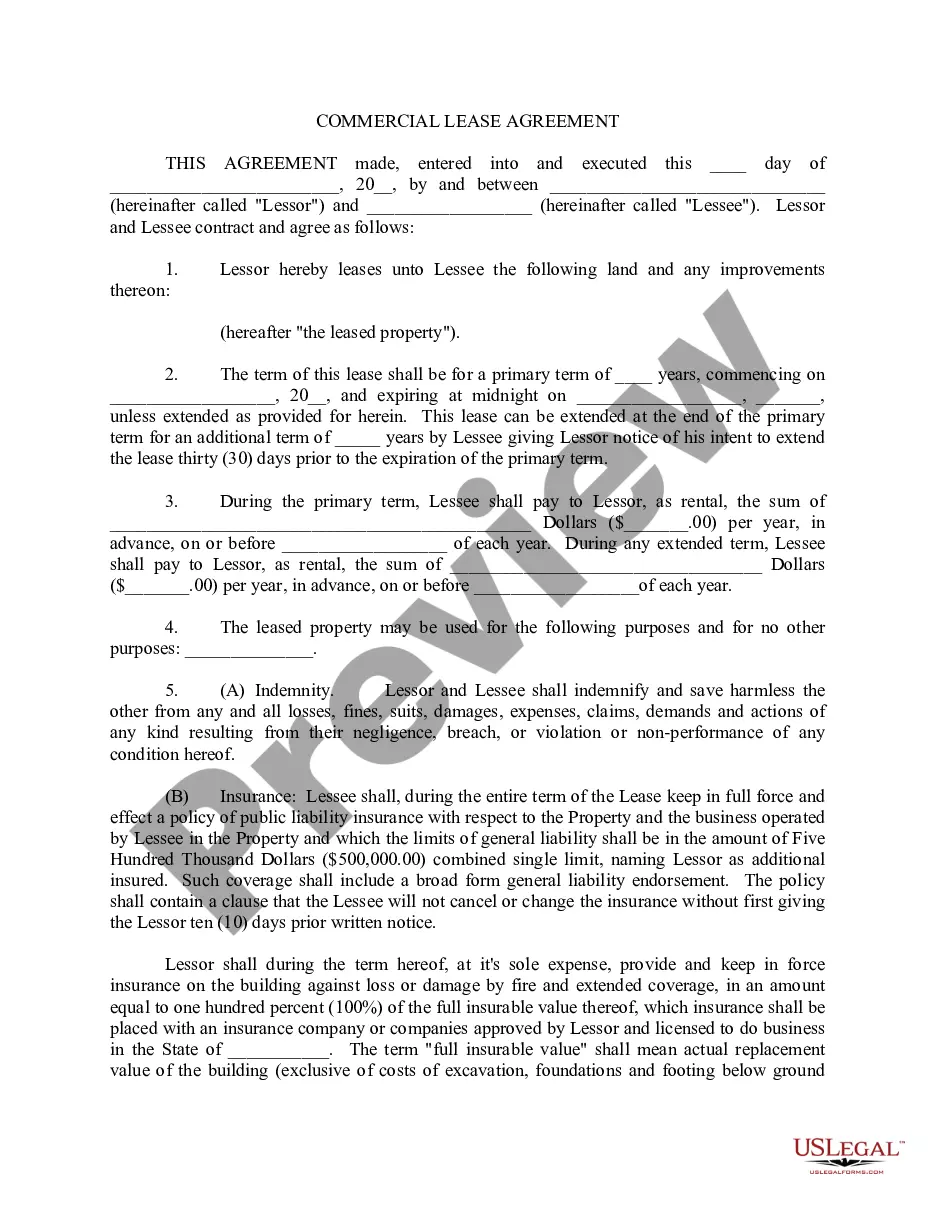

How to fill out Tenant Improvement Lease?

Legal documents management can be perplexing, even for the most seasoned professionals.

When you are looking for a Improvement Lease Withdrawal and lack the time to dedicate to finding the correct and current version, the procedures can be stressful.

US Legal Forms meets all your needs, from personal to business documents, all in one place.

Utilize advanced tools to complete and manage your Improvement Lease Withdrawal.

Here are the steps to follow after obtaining the form you need: Confirm this is the correct form by previewing it and reviewing its description. Ensure that the sample is accepted in your state or county. Click Buy Now when you are ready. Choose a subscription plan. Select the file format you require, and Download, complete, eSign, print, and send your documents. Take advantage of the US Legal Forms online catalog, backed by 25 years of expertise and trustworthiness. Streamline your document management today into a smooth and user-friendly process.

- Access a valuable resource library of articles, guides, and materials pertinent to your situation and requirements.

- Save time and effort searching for the documents you need, and utilize US Legal Forms’ advanced search and Preview feature to find Improvement Lease Withdrawal and obtain it.

- If you have a subscription, Log In to your US Legal Forms account, search for the form, and get it.

- Check your My documents section to review the documents you've previously downloaded and manage your folders as you wish.

- If this is your first experience with US Legal Forms, create a free account and gain unlimited access to all the benefits of the library.

- A comprehensive online form directory could be transformative for anyone seeking to navigate these matters effectively.

- US Legal Forms is a leader in online legal documents, with over 85,000 state-specific legal forms accessible at any time.

- With US Legal Forms, you can access state- or county-specific legal and business forms.

Form popularity

FAQ

A lessor must take the adjusted depreciable basis of an improvement made by the lessor for the lessee into account for purposes of determining gain or loss if the improvement is irrevocably disposed of or abandoned by the lessor at the termination of the lease.

You can't deduct leasehold improvements. But the IRS does allow building owners to account for their depreciation because any improvements made are considered to be part of the building.

When you pay for leasehold improvements, capitalize them if they exceed the corporate capitalization limit. If not, charge them to expense in the period incurred. If you capitalize these expenditures, then amortize them over the shorter of their useful life or the remaining term of the lease.

When you pay for leasehold improvements, capitalize them if they exceed the corporate capitalization limit. If not, charge them to expense in the period incurred. If you capitalize these expenditures, then amortize them over the shorter of their useful life or the remaining term of the lease.

Tax consequences to the landlord: The payment is treated as a lease acquisition cost and amortizes the cost over the lease term. Tax consequence to the tenant: The tenant has immediate income recognition upon cash receipt. The tenant may then depreciate the improvement.