Purchase Acquisition Method

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

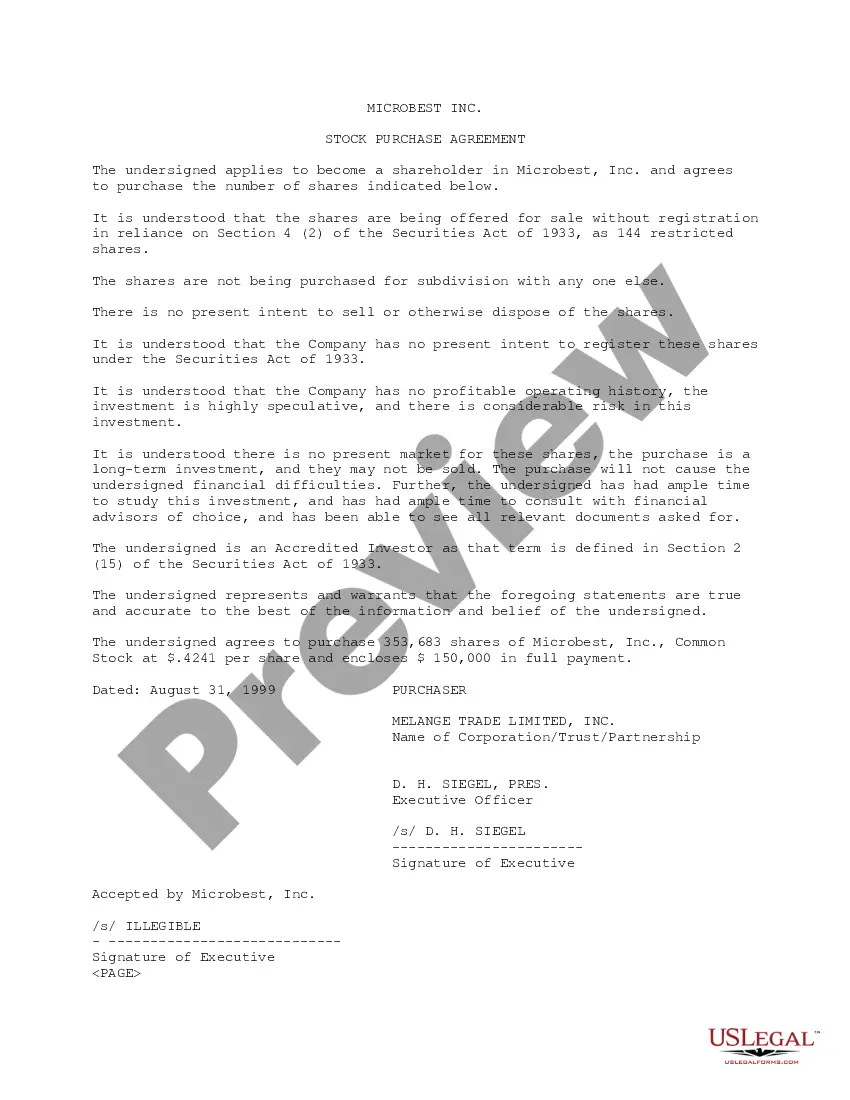

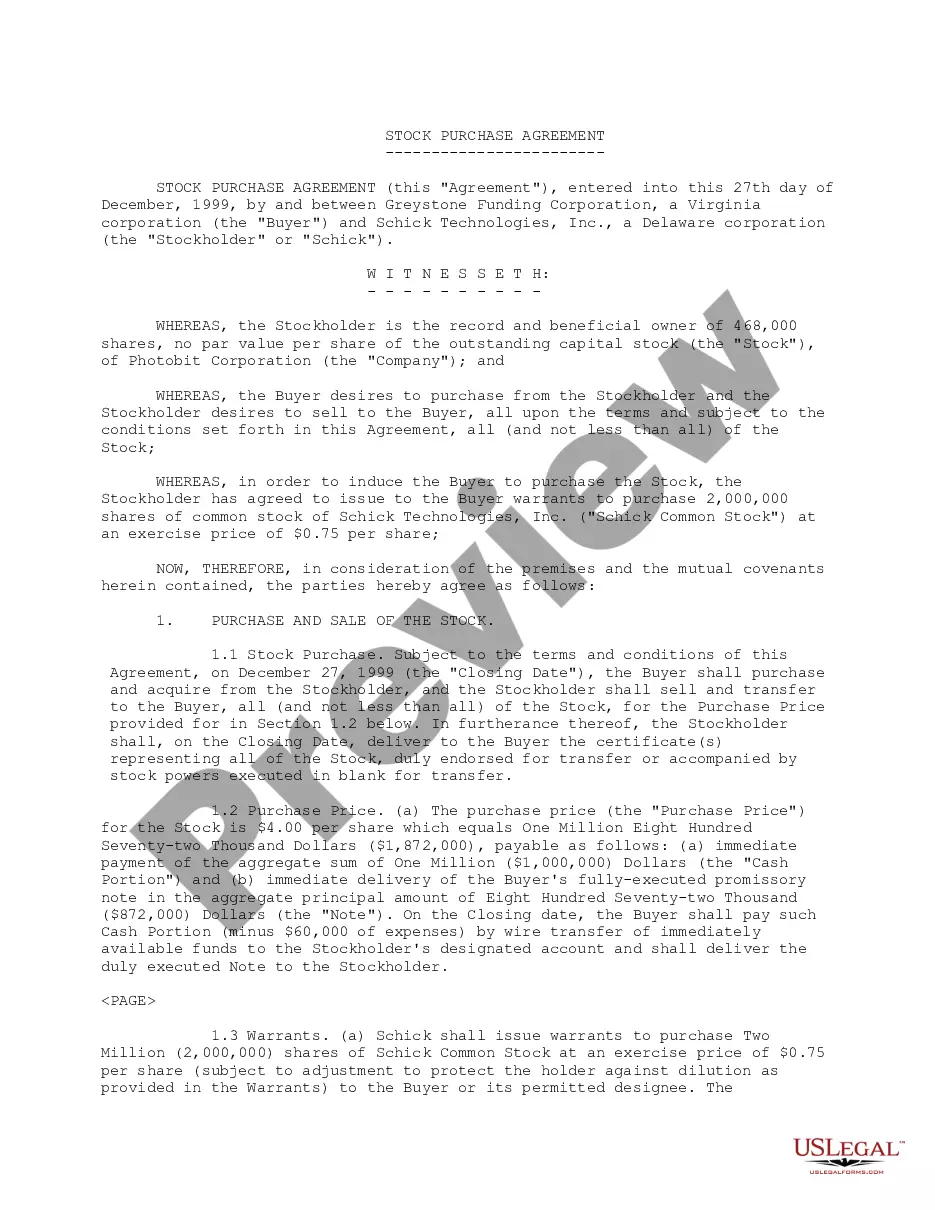

How to fill out Sample Stock Purchase Agreement Regarding Acquisition By Finova Capital Corp. Of All Outstanding Shares Of Fremont Financial Corp.?

Managing legal documents can be perplexing, even for the most skilled professionals.

When you are interested in a Purchase Acquisition Method and do not have the opportunity to spend time searching for the correct and current version, the process can be overwhelming.

US Legal Forms addresses any requirements you may have, ranging from personal to corporate documents, all in one location.

Leverage advanced tools to fill out and manage your Purchase Acquisition Method.

Here are the steps to follow after obtaining the form you need: Verify it is the correct document by previewing and reviewing its details.

- Access a valuable knowledge base of articles, guides, and resources related to your situation and requirements.

- Conserve time and energy searching for the documents you need by utilizing US Legal Forms’ advanced search and Review feature to find Purchase Acquisition Method.

- If you have a monthly subscription, Log Into your US Legal Forms account, search for the form, and retrieve it.

- Check the My documents tab to view the documents you have previously downloaded and manage your folders as you prefer.

- If this is your initial experience with US Legal Forms, create an account and enjoy unlimited access to the library's benefits.

- Utilize a comprehensive online form repository that can transform how you handle these issues efficiently.

- US Legal Forms is a frontrunner in online legal documents, offering over 85,000 state-specific legal forms available at your convenience.

- With US Legal Forms, you can access state or county-specific legal and business forms.

Form popularity

FAQ

The purchase acquisition method typically refers to gaining ownership of an asset, but it does not automatically imply 100% ownership. Many transactions allow for partial ownership or shared interests, depending on the terms negotiated during the acquisition process. When considering the purchase acquisition method, it's crucial to understand your specific goals and the structure of the agreement. At US Legal Forms, we provide resources that can guide you through the nuances of acquisition methods to help you achieve your desired ownership outcome.

An acquisition method refers to the approach a buyer uses to acquire another company or its assets. This process can include various strategies like mergers, stock purchases, or asset transactions. Understanding the purchase acquisition method can help you navigate the complexities of mergers and acquisitions effectively. If you are looking for tools or documents to facilitate this process, consider exploring the resources on the US Legal Forms platform.

Acquisition method Identification of the 'acquirer' Determination of the 'acquisition date' Recognition and measurement of the identifiable assets acquired, the liabilities assumed and any non-controlling interest (NCI, formerly called minority interest) in the acquiree.

Example 1: Acquisition / Purchase of Assets A company purchases the capital assets of another one for $200 million. It will have to record those assets on its balance sheet. This means that the acquiring company will have to record everything that the other company owns.

Under the purchase method, the difference between the acquired company's fair value and its purchase price was recorded as negative goodwill (NGW) on the balance sheet that was to be amortized over time. In contrast, with acquisition accounting, NGW is immediately treated as a gain on the income statement.

The acquisition method is based on the 4-step method in the business combination process below: Identify the Acquirer. Determine the Acquisition date. Recognize and measure identifiable assets acquired, liabilities assumed, and noncontrolling interest in the acquiree.

Purchase acquisition accounting is a method of reporting the purchase of a company on the balance sheet of the company that acquires it. It treats the target firm as an investment.