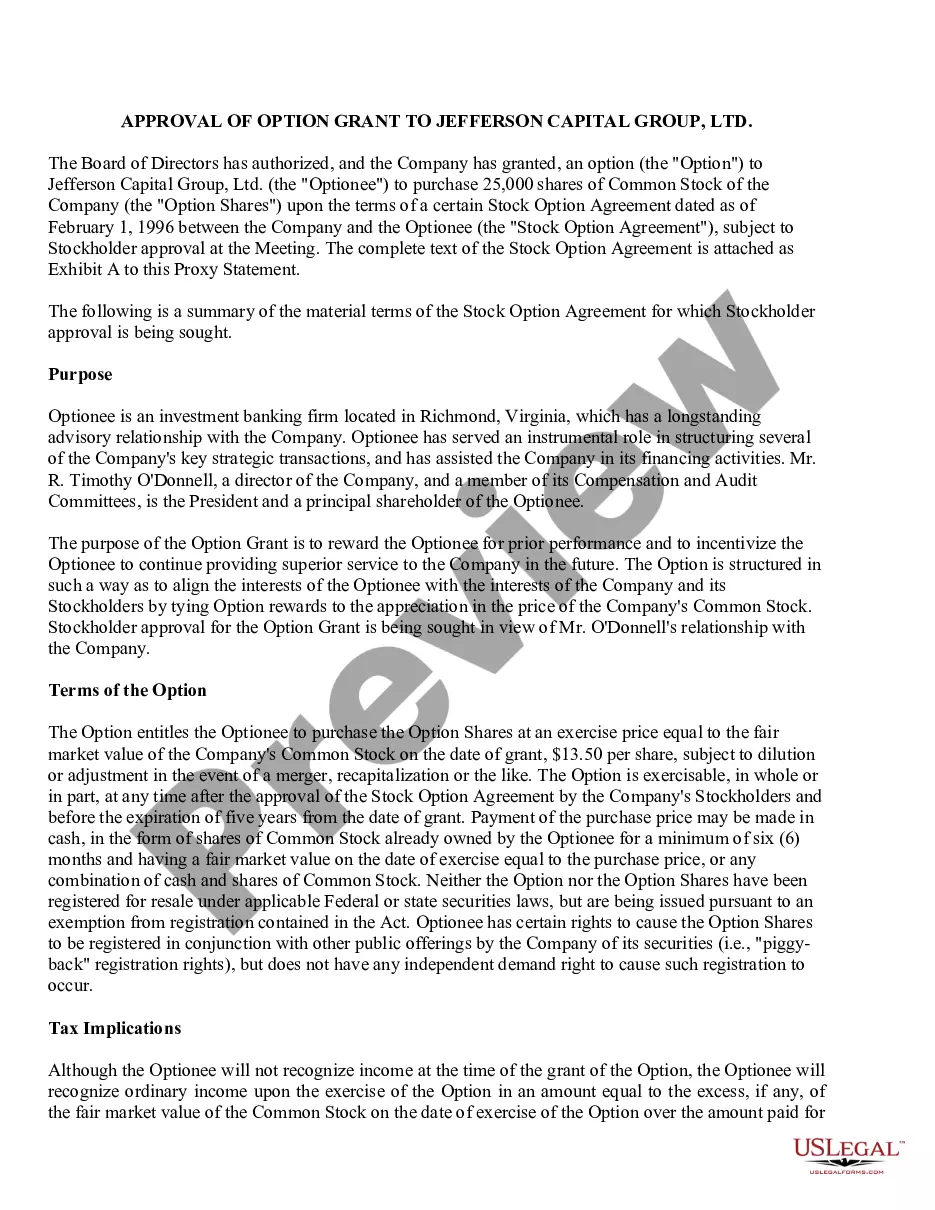

Granting Of Stock Options To Employees

Description

How to fill out Stock Option Grants And Exercises And Fiscal Year-End Values?

Whether for business purposes or for individual affairs, everybody has to deal with legal situations sooner or later in their life. Completing legal documents needs careful attention, starting with picking the right form sample. For instance, if you choose a wrong version of the Granting Of Stock Options To Employees, it will be turned down when you submit it. It is therefore crucial to have a trustworthy source of legal files like US Legal Forms.

If you have to get a Granting Of Stock Options To Employees sample, follow these easy steps:

- Find the sample you need using the search field or catalog navigation.

- Check out the form’s information to make sure it suits your situation, state, and county.

- Click on the form’s preview to examine it.

- If it is the incorrect document, return to the search function to locate the Granting Of Stock Options To Employees sample you need.

- Get the template when it meets your requirements.

- If you already have a US Legal Forms account, simply click Log in to gain access to previously saved templates in My Forms.

- If you don’t have an account yet, you may download the form by clicking Buy now.

- Choose the proper pricing option.

- Finish the account registration form.

- Select your transaction method: you can use a bank card or PayPal account.

- Choose the document format you want and download the Granting Of Stock Options To Employees.

- After it is saved, you are able to complete the form with the help of editing software or print it and finish it manually.

With a large US Legal Forms catalog at hand, you never need to spend time seeking for the right sample across the internet. Take advantage of the library’s simple navigation to find the correct form for any occasion.

Form popularity

FAQ

When the stock options are granted, the total stock option compensation expense is calculated as the fair market value of the stock options x the number of options granted. The company would debit stock option compensation expense and credit ?equity APIC ? stock option?.

Stock Option Granting and Vesting Basics You and the company will need to sign a contract that outlines the terms of the stock options; this might be included in the employment contract. The contract will specify the grant date, which is the day your options begin to vest.

Any compensation income received from your employer in the current year is included on Form W-2 in Box 1. If you sold any stock units to cover taxes, this information is included on Form W-2 as well. Review Boxes 12 and 14 as they list any income on Form W-2 related to your employee stock options.

Since you'll have to exercise your option through your employer, your employer will usually report the amount of your income on line 1 of your Form W-2 as ordinary wages or salary and the income will be included when you file your tax return.

Compensation expense is reported based on the stock's fair value (the market value) on the grant date. The shares are fully vested, and the company allocates the compensation expense over the service period, which is presumed to be the current period, unless other requirements are in place.