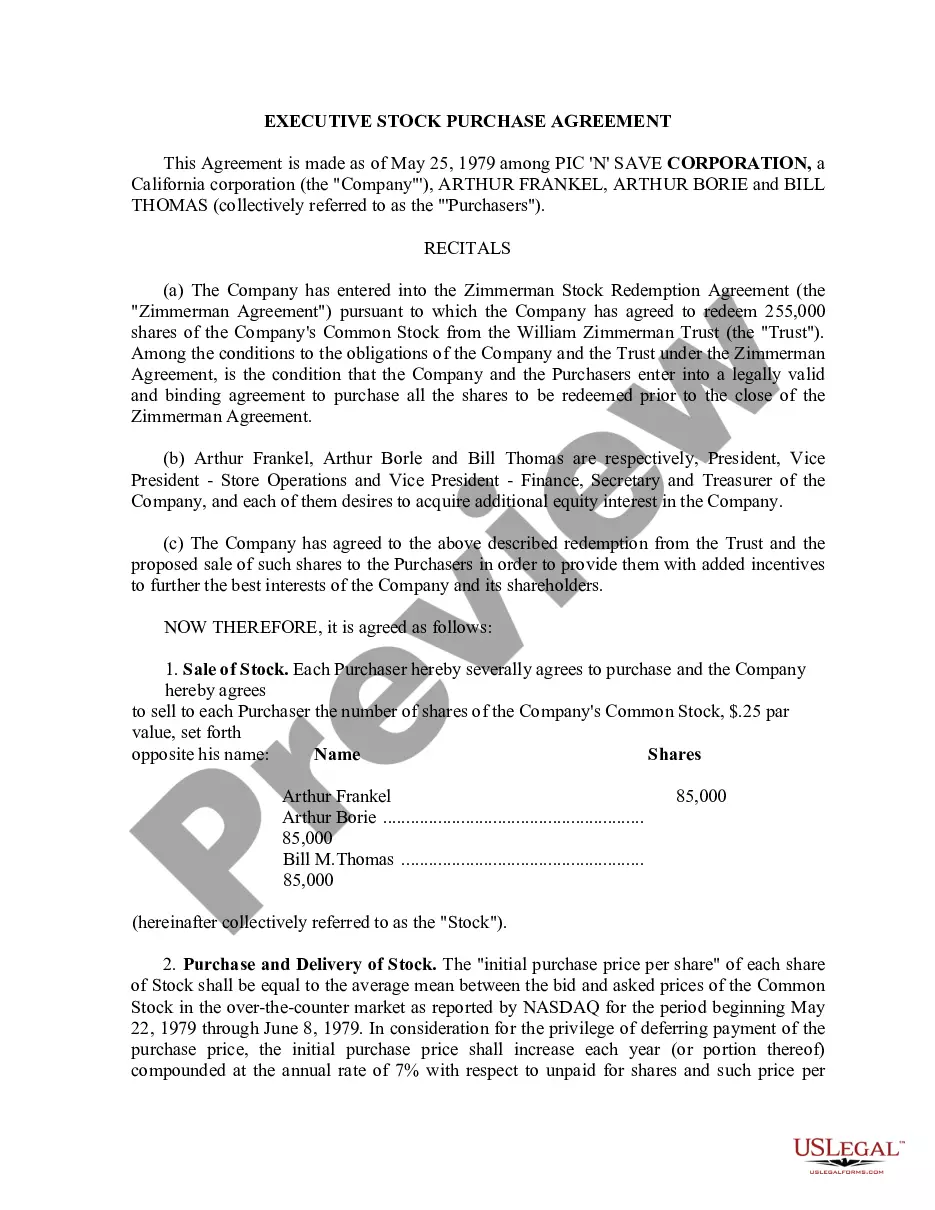

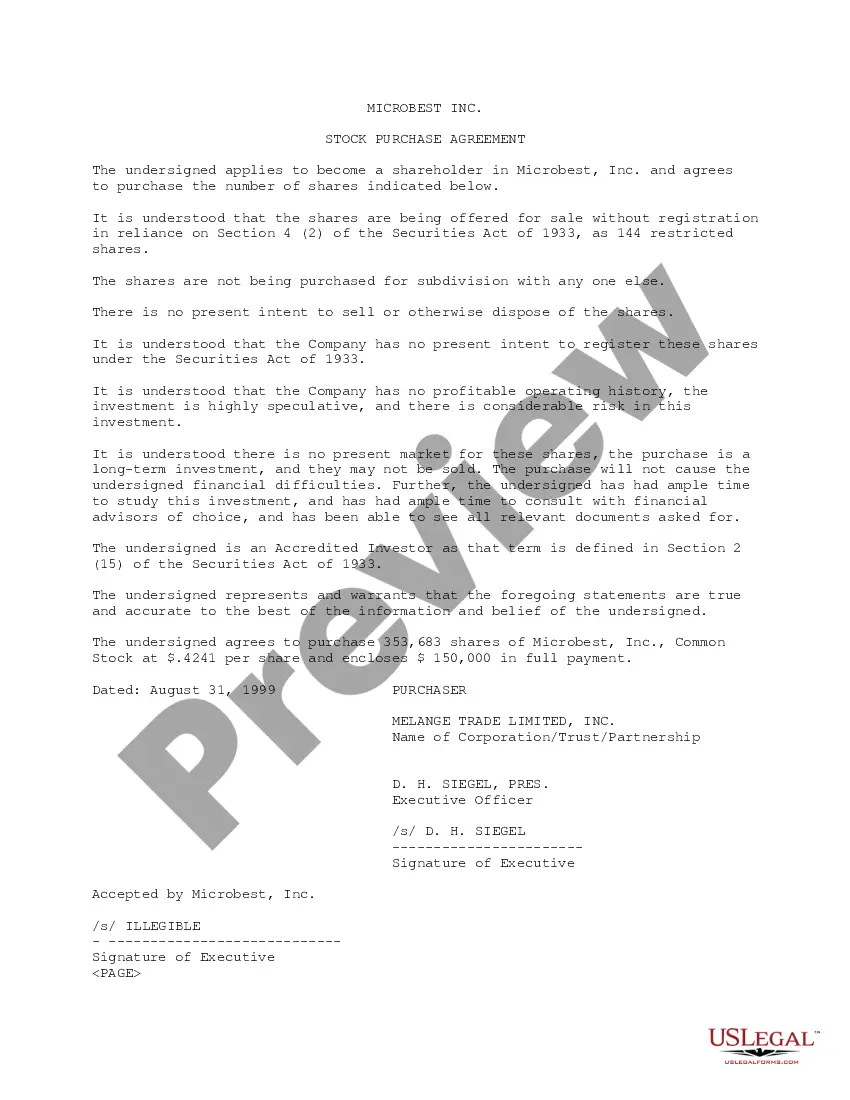

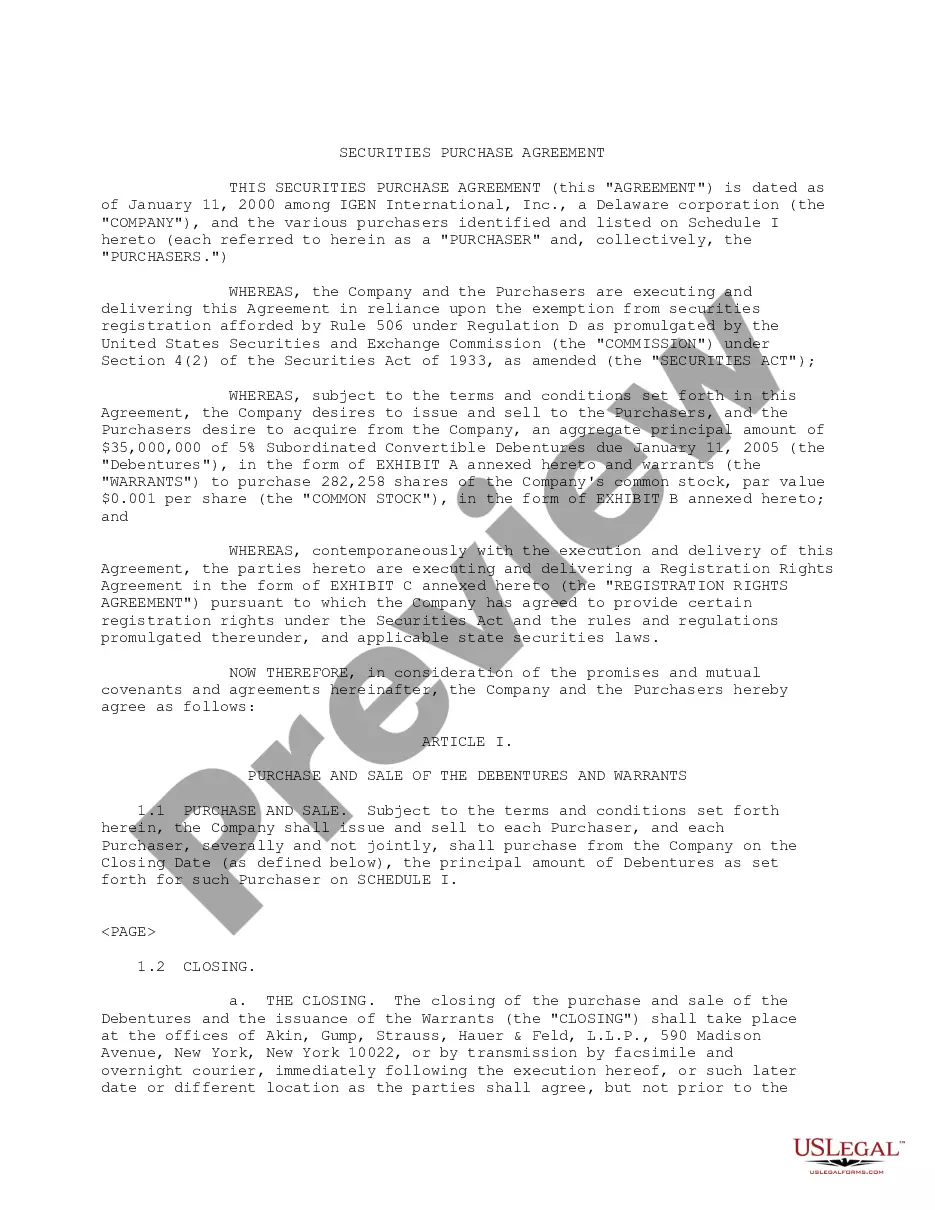

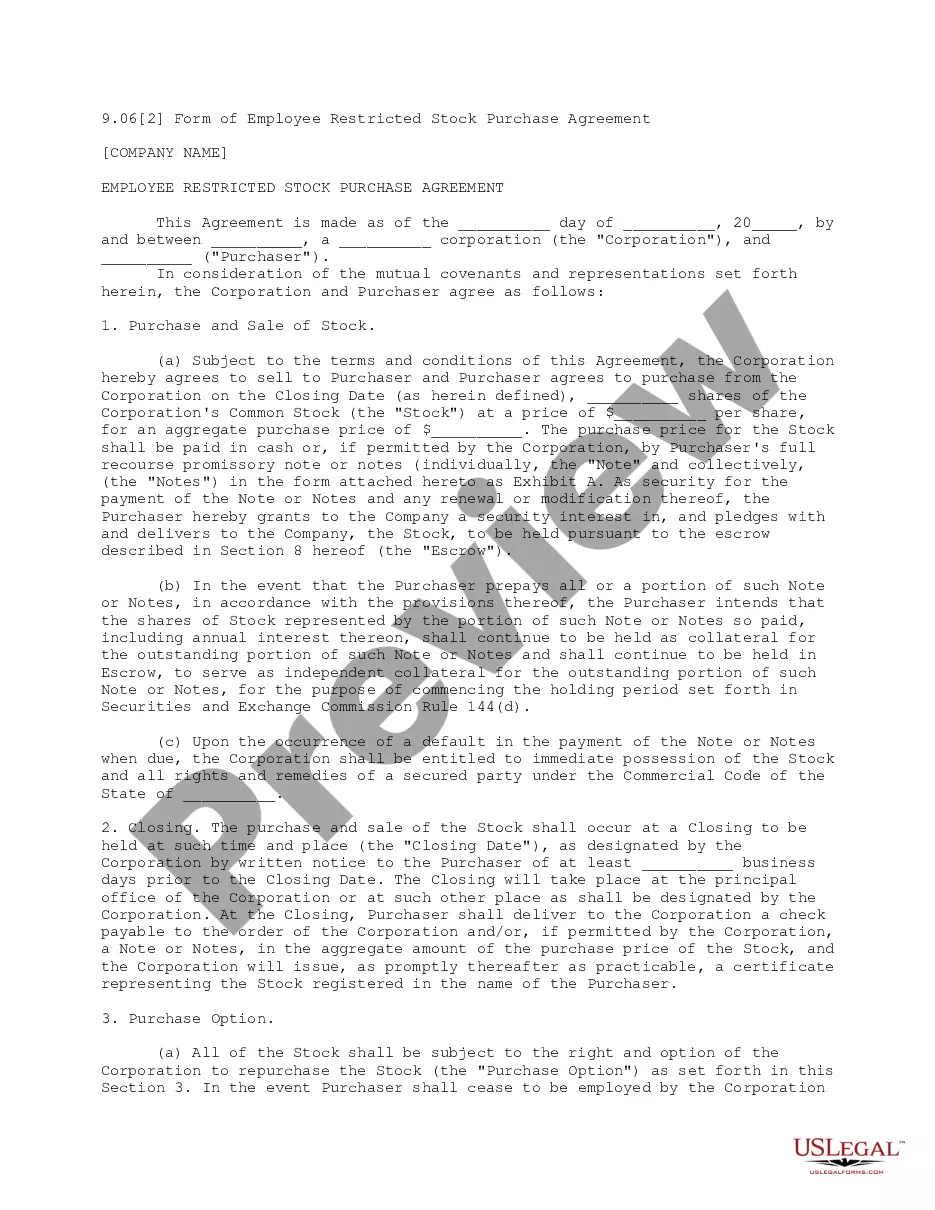

Restricted Stock In S Corporation

Description

Form popularity

FAQ

In general, retirement plans such as 401(k)s cannot be eligible shareholders in an S corporation. However, certain conditions can permit specific plan types to hold shares under IRS guidelines. Understanding these distinctions ensures you navigate ownership structures effectively while maximizing the benefits of your restricted stock in an S corporation. For guidance, consider using US Legal Forms to find relevant forms and compliance tips.

Certain entities, such as corporations, partnerships, and some financial institutions, are prohibited from investing in an S corporation. Additionally, non-resident aliens cannot be shareholders in an S Corp. Understanding who cannot invest helps maintain the tax benefits while maximizing your business's growth potential. Need assistance navigating this? US Legal Forms can be your trusted partner.

Yes, an IRA can hold private company stock, including shares from an S corporation, as long as certain IRS regulations are met. However, it is essential to ensure that the investment complies with rules regarding prohibited transactions. Always conduct thorough research before proceeding to avoid unexpected penalties. For legal clarity, utilize resources from US Legal Forms.

An IRA cannot hold certain types of investments, such as collectibles, life insurance, or investments in S corporations without adhering to specific regulations. Specifically, prohibited items generally include works of art, antiques, and gems. Understanding these restrictions helps you make informed decisions about your investment strategies. US Legal Forms offers guides to help clarify the regulatory landscape around IRAs.

When you hold restricted stock in an S corporation, tax reporting typically occurs at the time of vesting. You must recognize the fair market value of the stock as income on your tax return. Additionally, any gains or losses from the eventual sale of the stock will be subject to capital gains tax. For precise guidance tailored to your situation, consider using US Legal Forms for proper forms and support.

Fringe benefits for 2% shareholders in S corporations can be limited, especially when it comes to restricted stock. While these shareholders are entitled to some benefits, such as health insurance, certain perks may require careful tax considerations. Familiarizing yourself with the implications of restricted stock in an S corporation helps you navigate these benefits effectively and ensures compliance with IRS guidelines.

Obtaining restricted stocks typically involves purchasing shares directly from an S corporation or being awarded them as part of an employee incentive plan. When you acquire restricted stock, it means these shares are subject to certain conditions, such as vesting periods or performance criteria. Understanding the implications of restricted stock in an S corporation can guide you in evaluating such opportunities and maximizing their value.

The 2% owner rule is a crucial guideline when it comes to S corporations and their shareholders holding restricted stock. This rule states that shareholders who own 2% or more of the stock must follow specific regulations regarding fringe benefits and distributions. If you fall under this category, it is vital to understand how your stock can affect your income taxation and benefits under S corporation rules.

To report RSUs on your tax return, you will need to include the fair market value of the shares at the time they vest. This value is included in your Form 1040 as part of your income. Additionally, you should provide details of any stock sales on Schedule D. Using resources from US Legal Forms can simplify the process of reporting RSUs and ensure compliance with tax regulations.

Yes, restricted stock units (RSUs) in S corporations are taxed as ordinary income once they vest. This means that the value of the RSUs becomes part of your taxable income at that point. It's crucial to understand this tax implication as it can affect your overall tax situation. Consider consulting US Legal Forms for guidance on how to manage tax reporting for RSUs.